Top Stories of the Week - 3/29

This week in the newsletter, we write about SBF's 25-year prison sentence, developments in SEC v. Coinbase, and blobscription distruptions in Ethereum.

Subscribe here and receive Galaxy's Weekly Top Stories, and more, directly to your inbox.

SBF Sentenced to 25 Years

A year and a half after the collapse of FTX, Sam Bankman-Fried (SBF) was sentenced to 25 years in prison for defrauding customers, lenders, and investors. Presiding over the case, Judge Kaplan said SBF lost investors $1.7 billion, lenders $1.3 billion, and customers $8 billion, amounting to $11 billion in losses. SBF was also found guilty of witness tampering and 3 counts of perjury, including lying about not knowing that he was spending customer funds ahead of Fall 2022.

The sentencing featured remarks from various parties. Victims traveled to share grievances, highlighting concerns over the handling of the liquidation and refunding of client funds. SBF himself also spoke, taking responsibility for FTX’s collapse, but falling short of taking blame for causing it to happen. SBF’s lawyers argued his errors were a result of failed management instead of “malice in intent,” calling him a “beautiful puzzle.” Prosecutors used their final statements to hammer home that SBF committed egregious crimes and is likely to commit them again unless he receives the full sentence. In the closing statements, Judge Kaplan pointed toward Sam’s purposeful intent in committing the crimes and deceiving people afterward: “When not lying, he was evasive, hair splitting, trying to get the prosecutors to rephrase questions for him. I've been doing this job for close for 30 years. I've never seen a performance like that.”

SBF was originally found guilty on 7 counts of fraud by a New York jury in November 2023 (See our November coverage here). He has 14 days to submit an appeal, something his legal team has already indicated they will do.

Our Take:

FTX's failure triggered a domino effect across the crypto sector, leading to the write-down of investments worth billions and creating a ripple effect that collapsed entire portions of the market. Beyond investor losses, the fallout resulted in significant damage to crypto market confidence, legal and regulatory scrutiny across the globe, a major contraction in crypto market liquidity and credit, and significant reputational damage. SBF and FTX quickly transitioned from being the poster-child for crypto’s future to the standard example of why crypto is destined to fail.

Some have argued that the very same conditions that enabled SBF’s rise remain today. That is patently false. New exchanges have emerged that enable users to self-custody their funds. These platforms are designed to address the lack of custody and transparency that contributed to the FTX collapse by ensuring users maintain direct control over their digital assets. Exchanges that don’t offer self-custody have started implementing proof of reserve audits to provide verifiable evidence that the exchange possesses the funds it claims to hold on behalf of its user. A critical step forward, U.S. users finally have access to a regulated Bitcoin ETF that affords them the same investor protections they’d get buying equities and further reduces their incentive to move to unregulated offshore exchanges.

Beyond technological and operational changes, there's also a been a push for better regulatory frameworks and self-regulatory practices within the crypto industry. No longer are U.S. government officials getting their crypto talking points and regulatory direction from the very same individual defrauding his customers of billions of dollars. Honest stakeholders are engaging in discussions to establish clearer rules that protect consumers while fostering innovation. These conversations are crucial for creating a stable environment where the potential for fraud and mismanagement is minimized. Progress in this space, unfortunately, continues to be hampered by unclear guidance from regulatory agencies (see SEC Commissioner Hester Pierce’s recent dissent).

Despite these steps forward, crypto remains fraught with challenges. As SBF received his sentence, an anonymous individual amassed over $30 million in deposits through a mere tweet about launching a memecoin. This illustrates the persistent vulnerabilities within the crypto space. The journey ahead is still steep, and a priority must be placed on addressing and rectifying the harmful practices that have marred the industry's reputation in the past. With the SBF debacle coming to a close, onward. - Lucas Tcheyan

SEC v. Coinbase Case to Move Forward

Coinbase will have to face SEC's lawsuit, per court ruling. On March 27, a federal judge ruled that the SEC's lawsuit against Coinbase, originally filed on 6/6/23 alleging Coinbase engaged in unregistered securities offerings over its handling of 12 specified tokens, will move forward. Specifically, the SEC's complaint alleged that Coinbase operates an unregistered securities exchange, broker, and clearing agency, and also that its staking program itself is an unregistered security. Coinbase had filed a motion to dismiss the charges in August 2023, claiming the identified tokens specified in the complaint are not "investment contracts" and that the subject matter of the suit "falls outside of the agency's delegated authority."

According to the latest ruling, “the Court finds that the SEC adequately alleges that Coinbase, through its staking program, engaged in the unregistered offer and sale of securities.” However, the judge did side with Coinbase in dismissing the claim that Coinbase acted as an unregistered broker through Coinbase Wallet. Coinbase's Chief Legal Officer, Paul Grewal, tweeted that the court's decision was expected and that Coinbase remains confident in their legal arguments and is "eager for the opportunity to take discovery from the SEC for the first time."

Both parties have until April 19 to propose a case management plan. No date has been set yet for when the SEC v Coinbase court proceedings will commence into the discovery phase.

Our Take:

Judge Polk Failla partially rejects Coinbase's motion, allowing for the SEC's lawsuit to move forward to the discovery phase in what should be an exciting heavyweight battle that has meaningful implications for the broader crypto industry. Overall, the court's ruling did not read as particularly sympathetic for Coinbase's arguments, though Judge Failla did make some positive assertions in favor of the exchange. It's important to note that in evaluating motions for judgment on the pleadings, the court must assume that all the facts alleged by the SEC are true for the purposes of deciding whether to move forward with the case (but it does not imply that the alleged facts are actually deemed to be true). The judge here is merely ruling on which matters are alleged sufficiently to proceed to trial on those matters.

On application of the Howey Test, Judge Failla asserted Coinbase's offerings for some crypto assets on its platform could plausibly be classified as "investment contract" transactions. Judge Failla affirmed that the tokens in and of themselves are not "securities", though certain transactions relating to those tokens can be "securities" transactions depending on the circumstances. The ruling also assumes that some customers purchased tokens on Coinbase's secondary market exchange to make an investment with a reasonable expectation of profits from managerial efforts of the token issuers. In addition, Judge Failla ruled that the SEC has made a plausible claim that Coinbase's staking program was structured in a manner that a reasonable investor would expect to earn profits from Coinbase's managerial efforts in operating the program.

However, Coinbase notched a meaningful win as the SEC's claim relating to Coinbase Wallet was dismissed. Judge Failla held that even if Coinbase Wallet is used to initiate transactions in tokens that qualify as "investment contract" securities transactions under Howey (which is a big "if"), the SEC cannot prove that Coinbase acts as a broker by making Coinbase Wallet available to its users. Judge Failla's determination relating to Coinbase Wallet considered Coinbase's control over the product and other characteristics. For example, Coinbase does not control customer crypto assets held in Coinbase Wallet - users custody their own funds and are the sole decision makers for making transactions through Wallet. Coinbase Wallet also does not make investment recommendations or process trade documentation. These control considerations, if extended to other non-custodial wallets and DeFi protocols that similarly do not exercise independent control over a user's crypto holdings, could potentially provide more regulatory assurances for operators in the space.

Moving forward, the big questions will be determined at trial which is not likely to occur, nor the case conclude, for several years. - Charles Yu

Blobscriptions Cause Missed Block Rate on Ethereum to Soar

Blob fees skyrocketed for the first time on Wednesday, March 27. Blobs are a new transaction type on Ethereum introduced through the Dencun upgrade that offers more cheaply priced block space for large volumes of data. Ethereum protocol developers envisioned the primary purchasers of blob space to be Layer-2 rollups that rely on Ethereum for data availability. However, on March 27, the launch of a website called “blobscriptions.io” caused an influx of blob transaction activity.The website enables users to easily store any type of data through blobs including digital images and text. Instead of batched transaction data from rollups, the majority of blob activity on the 27 was motivated by users inscribing other types of data to blobs. A view of what type of data is being inscribed through the blobscriptions site can be viewed in real-time here. Evidently, the type of inscriptions activity on Ethereum is similar in nature to the inscriptions activity seen on Bitcoin, comprising of users minting non-fungible and fungible tokens on-chain. From March 26 to 27, the total amount of fees paid hourly to Ethereum for blobs increased from below $5,000 to over $15,000.

Additionally, heightened blob activity caused the percentage of missing blocks on Ethereum to soar. On average, every half hour, roughly 2% to 4% of blocks are missed or fail to get included in the canonical chain of Ethereum blocks. However, this average soared to over 15% on Wednesday, causing widespread concerns among Ethereum protocol developers. Upon further investigation, Prysm client developer Terence Tsao said the root cause appears to be related to the Bloxroute MEV relay. On ACDE #184, Tsao explained that 99% of missing blocks were initially sent by the Bloxroute relay and that once the Bloxroute team shut down their relay, the missing block rate went back to normal levels. Shortly after the ACDE call, CEO of Bloxroute Labs Uri Klarman tweeted that he is “absolutely sure [Bloxroute] relays broadcast blocks and blobs correctly.” He said the team is still investigating the reason for the issues but that in his view the cause may be in Ethereum’s networking layer, not Bloxroute relay software. Though Tsao had indicated the issues causing missing blocks were not related to client software, the Lighthouse client team released a hot-fix on Wednesday to address “blob-related issues” impacting node stability and performance. Other client teams that have released new versions of client software to address various issues in nodes since the Dencun upgrade include Prysm and Teku.

Our Take:

The first meaningful bouts of blob activity on Ethereum have highlighted issues negatively impacting network health in client software and potentially MEV-Boost relay software. While the investigation into what is causing the uptick in missing blocks is still ongoing, it is clear that higher volumes of blob data on Ethereum is contributing to blocks taking longer to process on Ethereum than normal. The root cause may be due to certain client implementations and/or MEV relay implementations. Until the root cause is known and addressed, blob activity is likely to continue to contribute to poorer network health conditions causing slightly longer delays to blocks than before the Dencun upgrade.

The first meaningful bouts of blob activity on Ethereum have also highlighted interesting parallels about the use of Ethereum blob space versus Bitcoin witness data space. Despite the data in both types of additional block space being ephemeral, meaning neither Ethereum or Bitcoin nodes are required to retain data in these spaces indefinitely, there is a high demand from users to fill these cheaply priced block spaces with data anyways. On Bitcoin, users wanting to mint fungible and non-fungible tokens through the witness block space must rely on out-of-protocol standards and third-party data archival solutions to keep track of these tokens and their associated data. Even so, for users on Bitcoin, there are no other widely accepted ways to issue tokens on the network.

However, on Ethereum, users wanting to mint fungible and non-fungible tokens do not have to use blob space. In fact, not using blob space means that users can mint tokens directly to regular Ethereum block space which is retained indefinitely by full nodes, no third-party data archival solutions needed. The benefit of using blob space to mint tokens is that sometimes it can be cheaper to mint tokens through blobs than regular transactions. Before Wednesday, blobs were virtually costless as rollups were not utilizing the full capacity of blob space. With the launch of the blobscriptions.io site, inscriptions soon made up a large share of the underutilized blob space. As of Thursday, March 28, blob fees on Ethereum are trending at roughly $12 per blob and $3 per block transaction. Due to increasing blob fees, it appears that inscriptions as a share of blob space is decreasing as demand for inscriptions is not able to support increasing prices for blob space. Looking ahead, rollups are likely to outprice the large majority of inscriptions minting activity that the network has seen in the early weeks after Dencun activation. As adoption and value for rollups increases, they are likely to be the primary actors driving blob fees. For more data-driven insights on blob fees and activity, check out the Galaxy Research EIP 4844 Blob Dune Dashboard. – Christine Kim

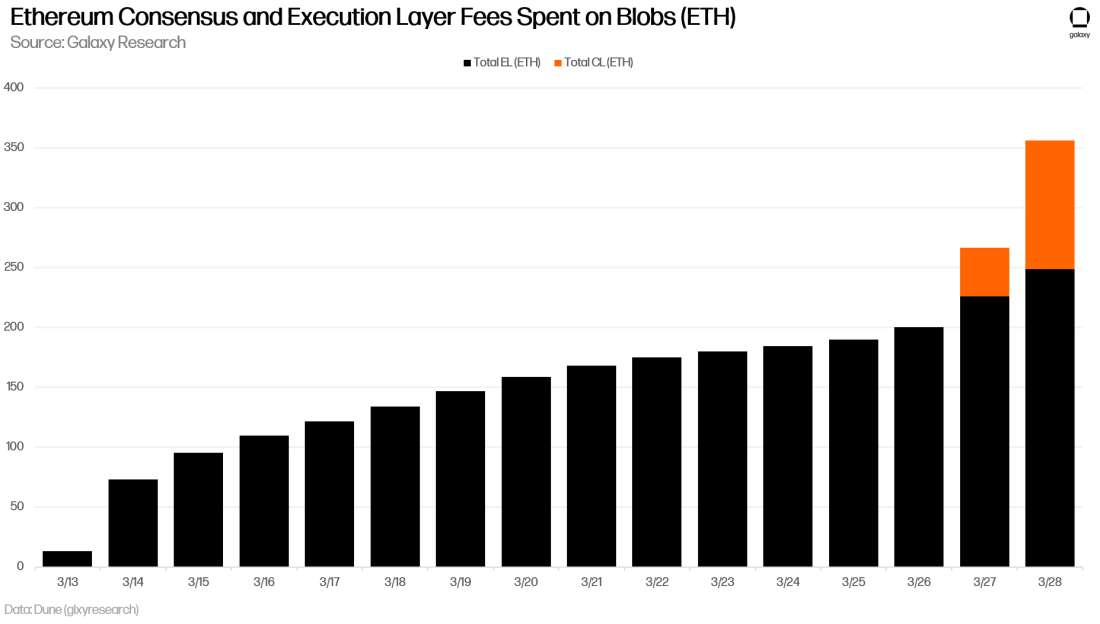

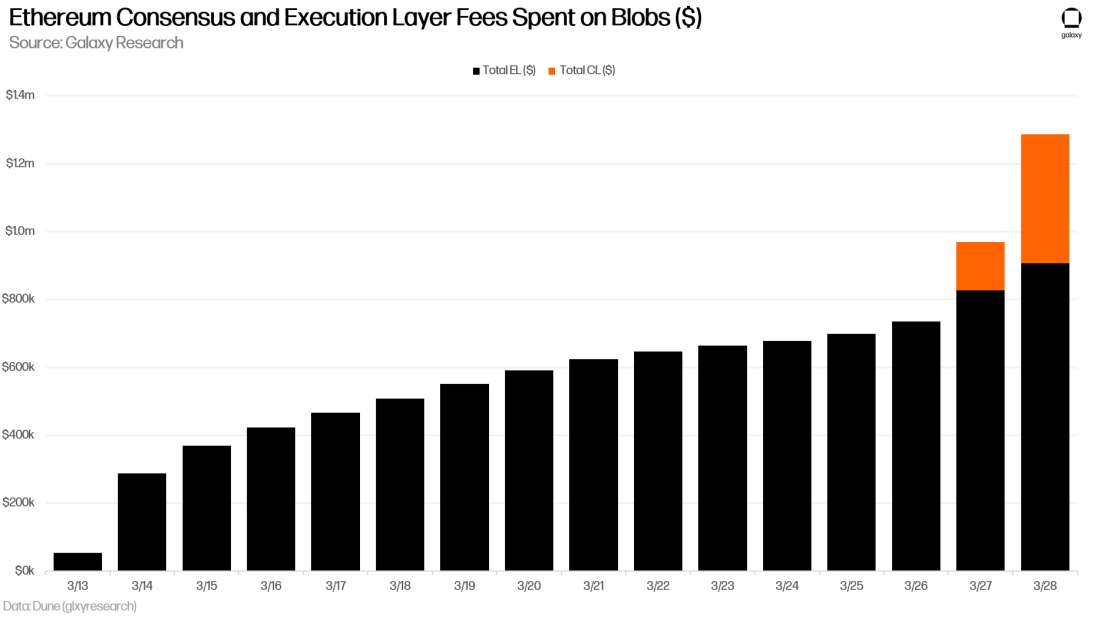

Charts of the Week

Blobscriptions, which let users inscribe data into Ethereum Consensus Layer (CL) blob objects, has led to significant inflation in the Consensus Layer costs of blobs. Before March 27, 2024 CL blob fees were virtually costless, with the median fee fluctuating around $0.000000001 (eight zeros) per blob. As of March 28, 2024 the median fee is $11.89. Growing demand for a finite amount of blob space per slot is driving costs higher.

In total up to March 28, 2024 107.5 ETH has been spent on CL blob fees and 248.6 ETH (base fees plus priority fees) has been spent on EL blob transaction fees. This amounts to a combined total of 356.1 ETH.

Together, this has amounted to almost $1.3 million in fees. A total of $380.1k has been spent on CL blob fees and $907k on EL blob transaction fees.

See Galaxy Research’s EIP-4844 Dune Analytics dashboard for more detail on the economic evolution of Ethereum L2s and EIP-4844.

Other News

Blast application Munchables exploited for $62.5 million worth of ETH.

Liquid staking protocol Prisma Finance exploited for $9 million worth of mkUSD and stETH.

Vitalik publishes blog on where Ethereum is heading after the rollout of blobs.

Bitcoin DeFi layer Alex raises $10 million strategic funding round.

Ethereum reaches 1 million validator milestone and 26% of supply staked.

Hong Kong-based asset manager VSFG and Value Partners apply for spot Bitcoin ETF.

Portugal orders Worldcoin to halt collection of biometric data.

Polygon zkEVM experiences 10-hour outage.

Circle launches its Cross Chain Transfer Protocol (CCTP) on Solana.