Top Stories of the Week - 10/13

This week in the newsletter, we share new revelations from the Sam Bankman-Fried trial, examine the launch of sFRAX, and discuss the slashing of 20 validators on Lido, the largest staking pool on Ethereum.

Subscribe here and receive Galaxy's Weekly Top Stories, and more, directly to your inbox.

FTX Insiders Detail Extent of Fraud

Sam Bankman-Fried trial heats up as insiders give testimony. Bankman-Fried faces seven charges, including wire fraud, securities fraud, commodities fraud, and money laundering. So far, witnesses have included Marc-Antoine Julliard, a FTX user who lost $100,000; Gary Wang, FTX’s CTO; Matt Huang, Paradigm co-founder and early investor in FTX; Adam Yedidia, developer at FTX; Caroline Ellison, CEO of Alameda; and Christian Drappi, Alameda research developer.

The witnesses have testified that Bankman-Fried was complicit in defrauding FTX customers by using their funds to back-stop Alameda and invest in venture deals, among other activities. They’ve also given deeper insight into Bankman-Fried and the full scope of alleged fraud at FTX and Alameda. Some of the more astonishing revelations to date include:

The famous balance sheet that CoinDesk published in November 2022, which eventually led to the collapse of FTX and won a Polk award for CoinDesk, understated the severity of the situation. In total, Sam and Caroline prepared eight alternative balance sheets for use with external parties, but went with “alt 7,” which misleadingly listed Alameda debts as “FTX Borrows.”

Sam, Caroline, and other members of FTX leadership allegedly paid $100 - $150 million in bribes to a Chinese account in order to get $1bn in funds released from Huobi and OKX that had been frozen by Chinese authorities. They allegedly first unsuccessfully tried to use accounts of Thai prostitutes to withdraw the money.

Sam appears to have purposefully cultivated a personal image of a young tech genius uninterested in wealth. This included his messily kept hair, inability to tie shoelaces, and driving a Toyota Corolla (he originally drove a “luxury vehicle” that he later swapped).

Alameda had allegedly had a negative net asset value of $2.7 billion as early as 2021, comprised of funds siphoned from unknowing FTX customers. Later, in November 2022, Alameda allegedly sold FTX customer funds (including Bitcoin and Ethereum) to prop up the price of the exchange’s native token (FTT), which comprised a significant portion of their collateral with lenders. Despite the negative NAV, Alameda made many large investments in long-term venture deals using customer funds.

Alameda was given the ability to have a negative balance on the FTX exchange, and therefore use customer funds for its own purposes, as early as July 2019, only two months after FTX launched. Alameda was eventually given a $65 billion line of credit by FTX.

According to Caroline Ellison, Sam wanted to become President and believed he had a 5% chance of realizing that goal.

The trial will finish its second week on Friday. It is expected to last six weeks in total.

OUR TAKE:

Sam Bankman-Fried appears to have hoodwinked everyone from customers to investors to the media. He tricked investors and customers into trusting him with their money. He manipulated colleagues into going along with wildly illegal acts in order to prop up FTX’s empty coffers. And he tricked the crypto industry – as well as many outsiders – into believing he was a boy-genius destined for greatness, or in his mind the Presidency. Bankman-Fried appears to have treated FTX as his personal bank account.

The trial is a reminder why “not your keys, not your coins” and "don’t trust, verify” are core pillars of the crypto ethos. Centralized exchanges play an important role in onboarding new users and facilitating liquidity, but they also introduce systemic risks, particularly given a historically murky U.S. regulatory picture that has, at times, pushed activity into offshore “black boxes” with little to no transparency. Proof of Reserves (PoR), particularly real-time PoR, is one industry standard that, if widely adopted, could help deter and mitigate these risks. In the case of FTX, had a proper real-time PoR existed, the market would have been alerted that something was amiss.

Also promising are developments in on-chain infrastructure and products. User experience is improving rapidly across the crypto ecosystem since the onset of the bear market (many of those improvements have been documented in previous newsletters). Coupled with a growing suite of sophisticated on-chain financial products and reductions in fees afforded by L2s and alt L1s, it’s becoming increasingly viable to replicate the centralized trading experience on-chain... (increasingly...definitely not fully there yet). Regulatory questions here still remain, but these platforms, while still prone to hacks, often offer more transparency than centralized exchanges, particularly as it relates to issues of solvency.

Centralized actors will always have a role in this space. They are essential for growth, adoption, liquidity, and regulatory compliance. However, the FTX fallout underscores the vital principle of “not your keys, not your coins.” It’s more than a meme, it’s a unique advantage arising from the transparent and permissionless ledgers that are foundational to the crypto ecosystem, and which traditional assets cannot (yet) replicate. - Lucas Tcheyan

20 Lido Validators Get Slashed

On Wednesday, October 11, 20 Lido validators were slashed (penalized and forcefully removed from the network by the Ethereum protocol). Lido is the largest Ethereum liquid staking protocol and controls over 274,000 validators, close to one-third of all Ethereum validators. Lido validators are operated by 31 () professional blockchain infrastructure providers that are vetted and voted on by. All 20 validators that were penalized on Wednesday were validators operated by, a blockchain infrastructure provider based out of the United Kingdom which formally joined Lido’s Ethereum Node Operator set in August 2023 (alongside SenseiNode, a blockchain infrastructure provider based out of Latin America).

As of Thursday, October 12, a full post-mortem of the incident by Lido and Launchnodes is still forthcoming. The Launchnodes team hinted on Twitter that the root cause of the slashing events is linked to “infrastructure and web3signer configuration issues.” In total, Lido validators were penalized 23.06 ETH (roughly $35,000). The penalty amount accounts for 2.25% of average daily rewards earned by all Lido validators. Launchnodes has since disbursed the exact amount back to the Lido protocol so that Lido liquid staked ETH holders are fully compensated for the reduction in their daily rewards. This was not the first time Lido validators have been slashed. In April 2023, 11 Lido validators operated by RockLogic GmbH, a blockchain infrastructure provider based out of Austria, were slashed. The total penalty was close to 14 ETH, which represented ~2.4% of daily Lido rewards at the time.

Since the launch of Ethereum’s proof-of-stake (PoS) consensus blockchain, also called the Beacon Chain, in December 2020, 300 validators have been slashed. This is less than 0.04% of the total number of active validators on Ethereum. The most common reason for slashing is known as the “attestation rule offense.” This occurs when a validator double votes on a block by propagating two block attestations instead of one. The largest slashing incidents on Ethereum are caused by professional infrastructure providers over-optimizing for node downtime and accidentally signing attestations with the same validator key twice. (For more information about Ethereum as a PoS blockchain, read this Galaxy Research report.)

OUR TAKE:

Slashing events on Ethereum are uncommon and most often triggered by accidental software misconfigurations by professional staking entities operating tens or hundreds of validators on a single node. However, one of the benefits of staking through Lido is the ability of users who delegate to professional staking entities to distribute the risk of potential slashing events across over 30 professional staking entities operating in different parts of the world. The penalty levied against Launchnodes validators represented only a small fraction of the daily rewards earned by all Lido validators. Therefore, even without the compensation from Launchnodes, the impact of the slashing event to Lido end-users in terms of lost staking revenue would have been minimal. However, the fact that Launchnodes did compensate their users for their minimal losses highlights one of the norms of the professional staking industry – providing compensation for slashing events. In early 2021, one of the largest slashing events on Ethereum was trigged by US-based blockchain infrastructure provider Staked in which 75 of their validators were slashed. The company took full responsibility for damages and reimbursed their clients.

Most centralized, professional blockchain infrastructure providers staking on behalf of users do offer clients full compensation for slashing penalties if and when they occur. Regardless and as stated above, end-users of Lido have the additional benefit of spreading out the risk and subsequent costs of slashing events across multiple node operators. To ensure these costs are distributed equally across node operators and to prevent one node operator from potentially become a single point of failure for the Lido protocol, the Lido development team has outlined that guide what types of blockchain infrastructure providers can be onboarded as node operators to the protocol and when. One of these core principles is: “No one node operator should have >1% of total ETH staked via Lido.” Another is: “Node operators should be distributed jurisdictionally.” This latter principle ensures that regulatory risk for Lido node operators is mitigated and distributed such that the rules and policies about staking as an activity in one country does not pose an existential threat to the Lido protocol. Because Lido is a more centralized protocol than the Ethereum network on top of which it operates, the members of the Lido DAO and the Lido development team can enforce principles and guidelines to intentionally distribute the risks of staking that the Ethereum protocol itself (and the disparate, amorphous ecosystem of independent stakers and professional blockchain infrastructure providers alone) would otherwise not naturally be able to coordinate to do.

In the weeks prior to this slashing event, the Lido protocol has been the target of severe criticism by influential Ethereum core developers and community members including but not limited to Danny Ryan, Ben Edgington, and Evan Van Ness. The main criticism against Lido is that the protocol controls too much stake, dangerously close to the one-third threshold that would effectively enable Lido to prevent the Ethereum network from finalizing. Not only does this criticism overlook the natural market forces propelling the growth of Lido only made possibly by Ethereum’s PoS design, but it also overlooks the fact that the Ethereum validator set would likely be more centralized, both geographically and technologically, without Lido, than with Lido. Judging by the largest competitors to Lido by number of validators, which are Coinbase and Figment (both companies based out of North America), fears about a single node operator posing a centralized point of failure to Ethereum are likely to have become more exasperated if liquid staking market forces had not propelled Lido’s growth. For many accusing Lido of not being culturally or politically “aligned” with the Ethereum ethos, it is important to consider to what values of the Ethereum ethos exactly are being challenged by Lido and if its design is really usurping those values, rather than upholding them. - Christine Kim

Frax v3: “The Final Stablecoin”

Frax releases official docs for Frax v3 with a new strategic focus around real-world assets (RWA). On Monday, the Frax team published the official docs for Frax v3, the new version of its protocol, sharing details around changes to the FRAX stablecoin / protocol and presenting several products built around a new RWA strategic focus. Some of the core concepts and features introduced with Frax v3 include:

Full exogenous collateralization of FRAX. The original version of the FRAX stablecoin launched in December 2020 operated as a hybrid collateralized stablecoin with an algorithmic backing using the FXS token (i.e., fractional reserve) that would occasionally permit FRAX's collateral ratio (CR) to fall below 100%. (To read more about the types of stablecoins, including hybrid stablecoins like FRAX, read our report Digital Dollars.) To improve the safety perception around FRAX's collateralization, the protocol now aims to keep >= 100% CR at all times. FRAX collateralization will be through AMO (algorithmic market operations) contracts and RWAs (e.g., T-bills, reverse repos, USD deposit yields at Fed master accounts, select shares of MMFs) held by partner entities. Following the passing of FIP-277, FinresPBC became the first RWA partner for v3.

Non-redeemability of FRAX. The v3 docs specify that "holding a FRAX stablecoin does not guarantee you the right to redeem it for any specific financial instrument or token at any particular time." The original Frax v1 protocol honored FRAX redemptions with a combination of USDC & FXS tokens depending on the CR. To stabilize FRAX price to $1.000 starting with v3, the Frax Protocol’s only function is to use AMO contracts (introduced with Frax v2), RWAs, and governance actions through frxGov.

Frax v3 also introduces two new token products to deliver treasury yields on-chain:

sFRAX (staked FRAX) is a staking vault (ERC4626) that distributes yield originating from RWA strategies to stakers (denominated in FRAX), aiming to keep the vault APY close to the IORB rate (the interest on reserve balances of the US Federal Reserve). Every Wednesday at 12 UTC, the Frax protocol mints new FRAX proportional to its earnings and adds them to the sFRAX vault. The sFRAX vault APY is based on a utilization function starting at 10% APY - as more FRAX is staked in the vault and the APY approaches the IORB benchmark rate, the protocol will deploy sFRAX strategies to keep the bottom APY close to the IORB benchmark.

FXB tokens resemble zero-coupon bonds convert to FRAX stablecoins at a predefined maturity timestamp. FXB tokens are not collateralized by RWAs or any other assets - they are only redeemable for FRAX tokens on a one-to-one basis. According to the docs, "FXBs allow the formation of a yield curve to price the time value of lending FRAX back to the protocol itself." Price discovery for FXB tokens occurs through a gradual Dutch auction system that ensures FXB tokens are not sold for prices lower than the floor limit.

The sFRAX token launched Thursday evening, attracting over 31m staked FRAX in less than 24 hours with an APY of 8.87% as of writing. Note: Frax v3 deployment will be gradual and not all features discussed have been deployed at this time.

OUR TAKE:

With the introduction of v3, Frax becomes the latest DeFi protocol to hop on the RWA trend aiming to bring high Treasury rates on-chain. (We wrote about this trend in our recent report on RWA.) So far in its short lifetime, the stability mechanism behind the FRAX stablecoin has gone through several iterations - with v3, the Frax team now completely ditches the original hybrid-algo stablecoin vision as it leverages RWAs to maintain 100%+ collateralization at all times for FRAX (should the team consider renaming the protocol & stablecoin given FRAX is no longer fractionally-reserved?). Frax v3 also removes direct redeemability of the stablecoin through the protocol (presumably due to regulatory pressure), meaning FRAX holders may have to turn to secondary markets (e.g., Curve) to exit their positions.

The more significant development around v3, in our view, is the launch of the two new RWA-based tokens: sFRAX & FXB. sFRAX shares some similarities with Maker's sDAI, which recently helped reverse the downward trend in DAI supply after lifting the DAI savings rate (DSR) in August to 8%, now 5%. Both sFRAX and sDAI pass favorable yields generated from T-bills and other RWAs to token holders, and both are built on the ERC-4626 vault token standard. However, an important distinction between the two tokens is the scalability of the yield vs. the deposited supply. Maker relies upon RWA deals with various financial institutions that each come with governance-set debt ceilings, which limits the protocol's revenue opportunity from each deal. On the other hand, Frax sources RWA yield in a more dynamic strategy through RWA partners like FinresPBC, enabling sFRAX APY to follow a yield curve based the weekly minted amount by the protocol & utilization rather than a step-wise yield function like with sDAI.

Moreover, FXB complements sFRAX by providing benchmark treasury yields across longer durations, enabling the construction of an on-chain yield curve (sFRAX represents the zero-duration point in the curve). If the yields from sFRAX and FXB track closely to the actual benchmark rates, Frax's yield curve could become a new standard adopted across DeFi with the potential to provide more efficient markets and unlock new risk capabilities through greater duration matching capacity.

These new RWA products will add to Frax's already diverse and complementary product suite that includes the FPI price index token, frxETH LST, Fraxswap AMM, Fraxlend, & the Fraxferry cross-chain bridge - with the Frax protocol already offering just about all the core DeFi primitives, the rationale for launching their own dedicated Fraxchain L2 becomes much clearer. These complementary offerings and integrations can be important differentiators between products for adoption as the competitive space among RWA-focused protocols becomes more crowded with more yield-bearing stablecoin offerings (e.g., the USDM yield-bearing stablecoin issued by Mountain Protocol which just went live on Curve). While RWA / tokenization appears to have long lasting power, recent credit defaults and depeggings (e.g., $20m RWA loan defaulted on Goldfinch’s platform or the depegging of real-estate-based USDR stablecoin on Polygon) remind us that RWAs come with their own unique set of risks that should be carefully monitored. - Charles Yu

Charts of the Week

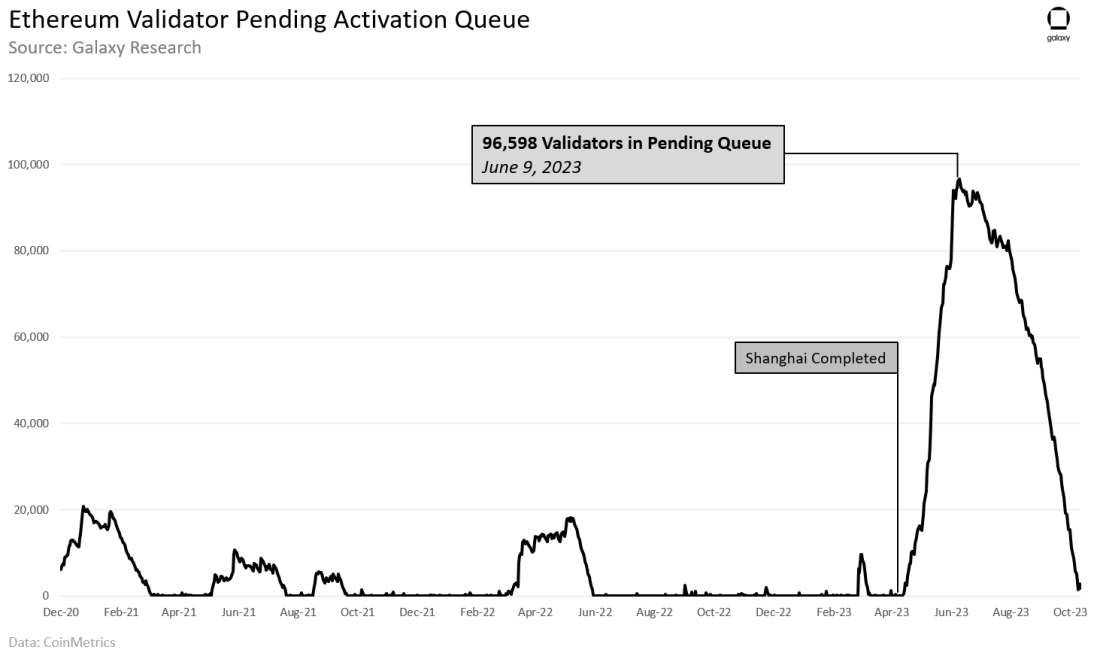

There are 1,821 validators left in Ethereum’s pending activation queue. The number of validators waiting to come online has seen a steep decline in recent months, dropping 98% (or 80,497 validators) since July 29. The pending activation queue reached an all-time high of 96,598 validators on June 9, and is currently at levels last seen just after Shanghai in mid-April.

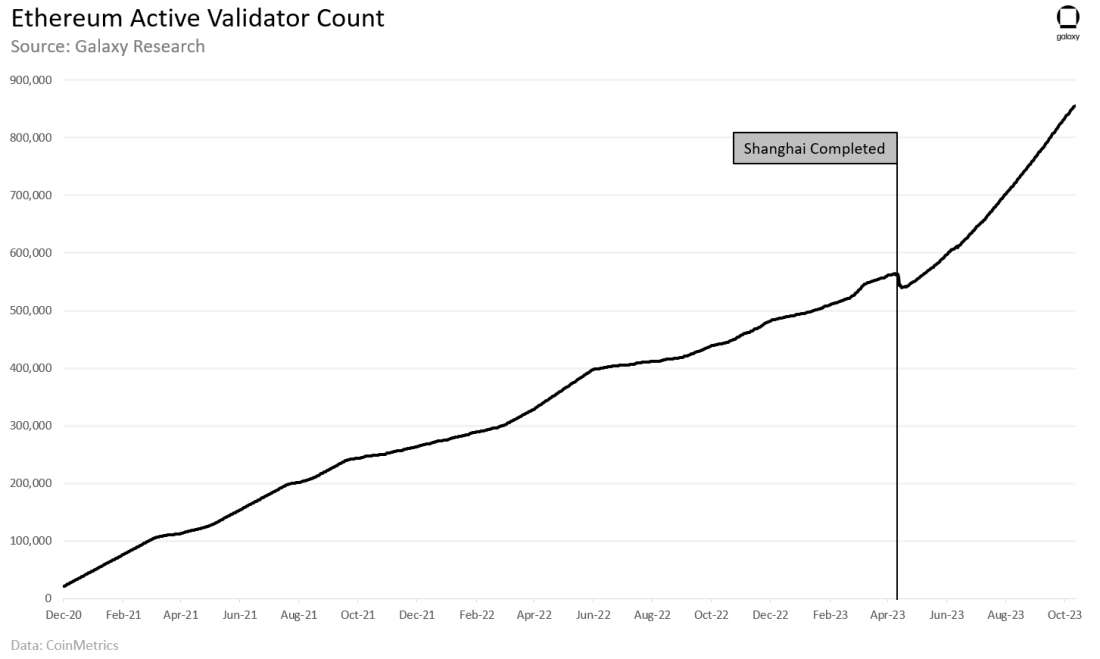

The size of Ethereum’s active validator set has continuously made new highs as the activation queue drained. As of October 11, there were 855k active validators. See this report from Galaxy Research to learn more about Ethereum’s growing validator set and the challenges it poses.

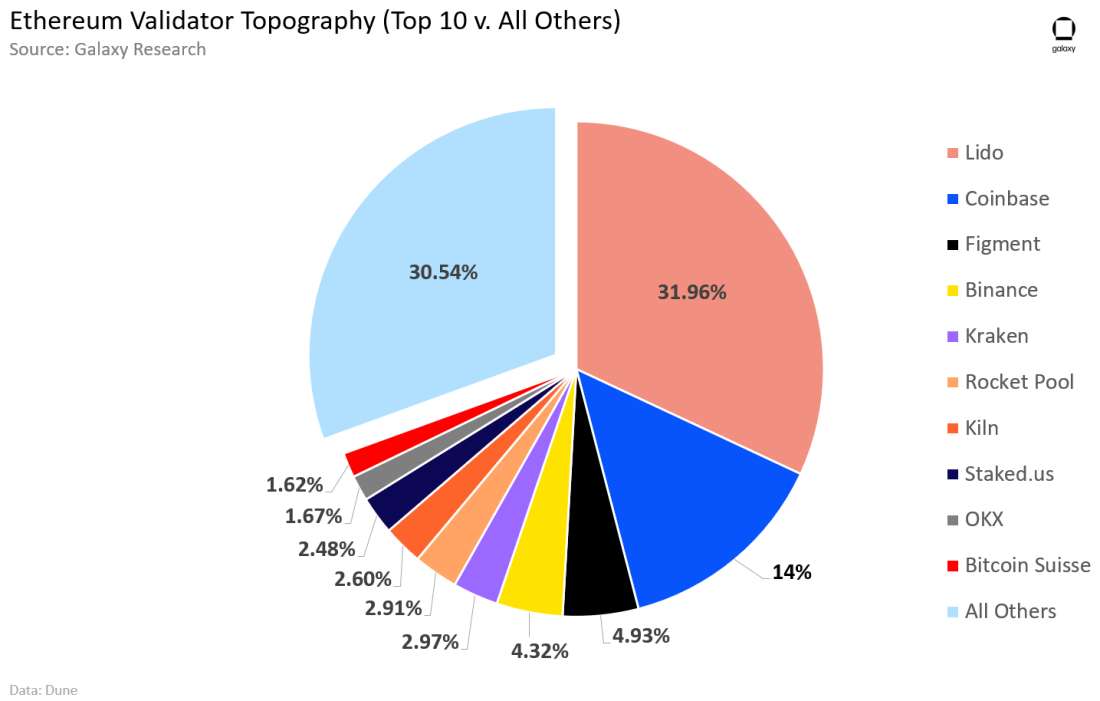

Lido, a liquid staking platform, controls more than 32% of active Ethereum validators (275k validators). The chart below highlights Ethereum’s validator topography, comparing the top 10 validators by share to all other validators.

Other News

BitVM aims to enhance Bitcoin smart contract capabilities without fork

Mastercard successfully wraps up CBDC pilot with Reserve Bank of Australia

CFTC charges Voyager co-founder Stephen Ehrlich with fraud

Hacker returns 90% of stolen funds to Stars Arena following exploit

Solana investment products see largest week of inflows since March 2022

Uniswap launches Android wallet beta for Google Play

Circle rolls out native USDC tokens on Polygon

Real USD (USDR) stablecoin depegs and price crashes by 50%

From the Desk of Galaxy Digital Research

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2023. All rights reserved.