Overview of On-Chain RWAs and the Forces Propelling their Growth

Executive Summary

Real world assets (RWAs) are the fastest growing category of assets in decentralized finance (DeFi). Total value locked in RWAs has nearly doubled in 2023, growing from $1.44bn to $2.5bn as of September 30, 2023. The acceleration of tokenized real-world assets has been propelled by changing tides in the broader macroeconomic environment. While onchain yield opportunities were historically driven by new token issuance, and traditional yields were near zero, now rising interest rates coupled with a cryptoasset bear market has increased the attractiveness of traditional yield generating instruments such as U.S. Treasuries and private credit. This in turn has reduced demand for crypto native yield-generating instruments in DeFi and increased demand from crypto native users for products that capture the reward of off-chain yield through on-chain channels. This report is the first in a series on RWAs and their growth. It will cover the expansion of on-chain RWAs in 2023 through the lenses of 1) the issuers bringing them on-chain, 2) the types of on-chain RWAs, and 3) the reasons why RWAs are expanding on-chain.

Key Takeaways

The report will exclude stablecoins (the largest and most established RWA by value capture at $125bn) from charts and RWA TVL calculations. This is done so the growth of the smaller RWAs by market cap is not obfuscated and the forces propelling other RWAs are not understated.

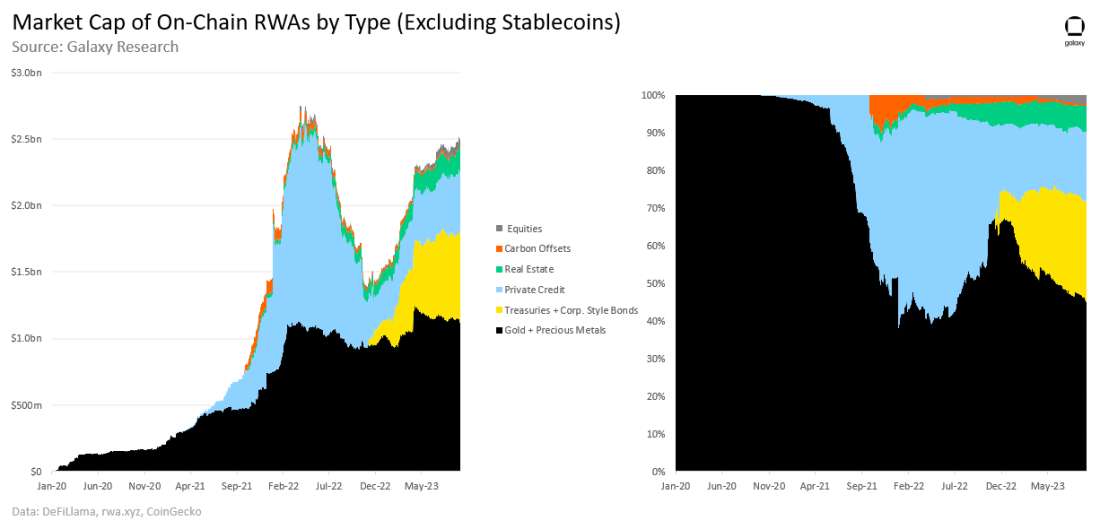

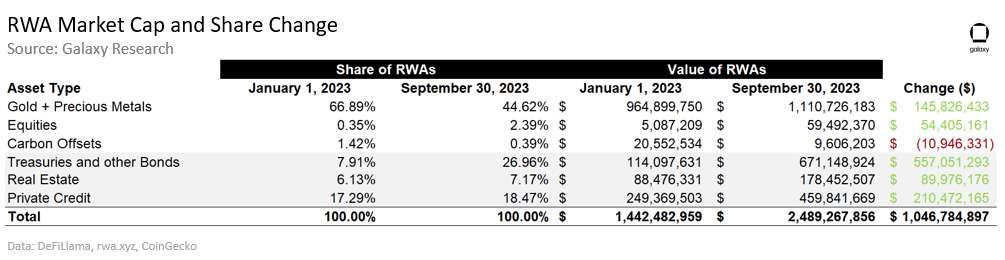

Non-stablecoin RWAs grew in onchain value by $1.05bn in 2023, $855.7m (82%) of which has come from Treasuries, real estate, and private credit - all yield-bearing assets.

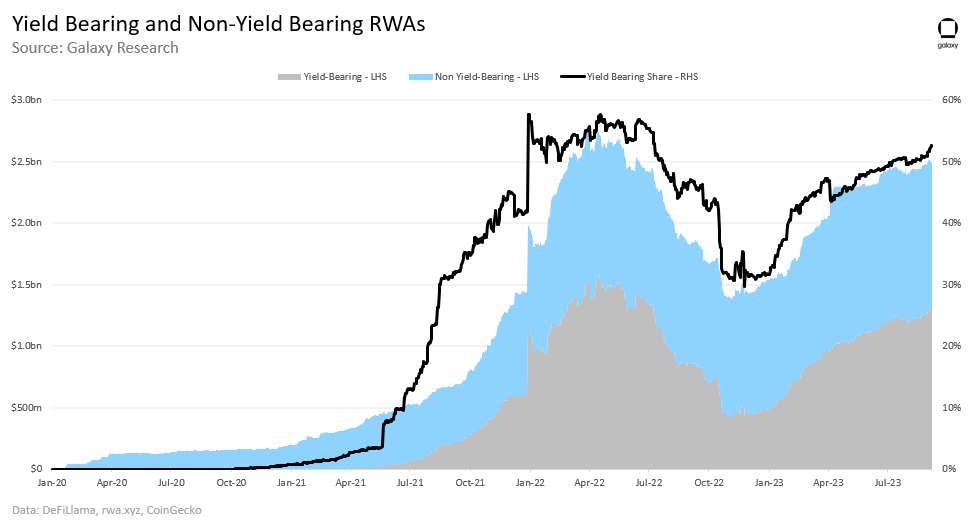

Demand for off-chain yield is fueling the growth of RWAs on-chain. The market share of yield-bearing RWAs has grown from 31% to 53% from January 1 to September 30.

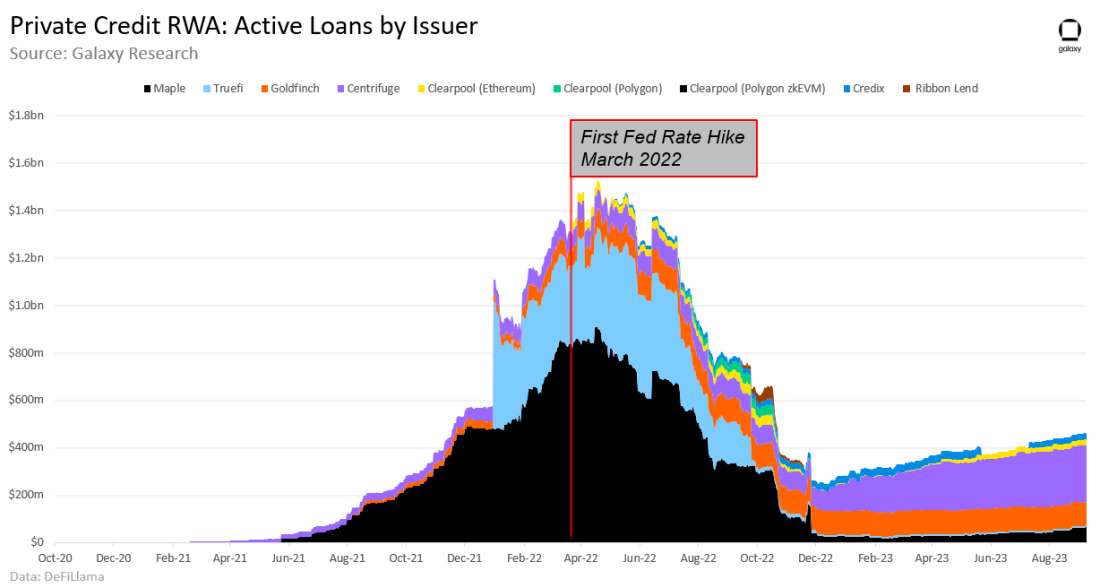

The value of active on-chain private credit loans has expanded $210.5m (84%) over the same period. But is still down 70% from its all-time high.

On-chain real estate grew the least in dollar terms of all the yield-bearing RWA categories covered in this report, adding $90m in value (102% growth) over the same period.

Treasuries and other bonds grew by $557m over the same period. This pool of value consists of a U.S. Treasuries and on-chain corporate-style bonds.

Despite having a strong year of growth in 2023, the market cap of tokenized RWAs is still 9.6% below the all-time achieved in Spring 2022.

Introduction

There are several RWAs that exist on-chain, each exhibiting different qualities and serving divergent use cases. While certain types of RWAs such as stablecoins and tokenized gold have existed for several years, others like Treasuries have recently emerged against the backdrop of a rising interest rate environment. Through this report we will give a brief overview of the following types of yield-bearing RWAs:

Real Estate

Private Credit

Treasuries

Note: The following analysis focuses on RWAs, the tokenized assets, and their market caps. This report does not contain information about the underlying protocols where RWAs are built (e.g. Ethereum, Polygon, Stellar, etc.) or the ancillary blockchain-native services that support RWA trading and treasury management. Moreover, the report will exclude stablecoins (the largest and most established RWA by value capture at $125bn) from charts and RWA TVL calculations. This is done so the growth of the smaller RWAs by market cap is not obfuscated and the forces propelling other RWAs are not understated. For a detailed overview of the stablecoin market, read this Galaxy Research report.

Integrating the Real World with the Digital

RWAs are created by issuers that fulfill one or more of the following activities:

The acquisition of assets in the real world

The tokenization of these assets on-chain

The distribution of RWA tokens to on-chain users

Without issuers, whether they are centralized companies, decentralized protocols, or a combination of both, RWAs would not exist on-chain.

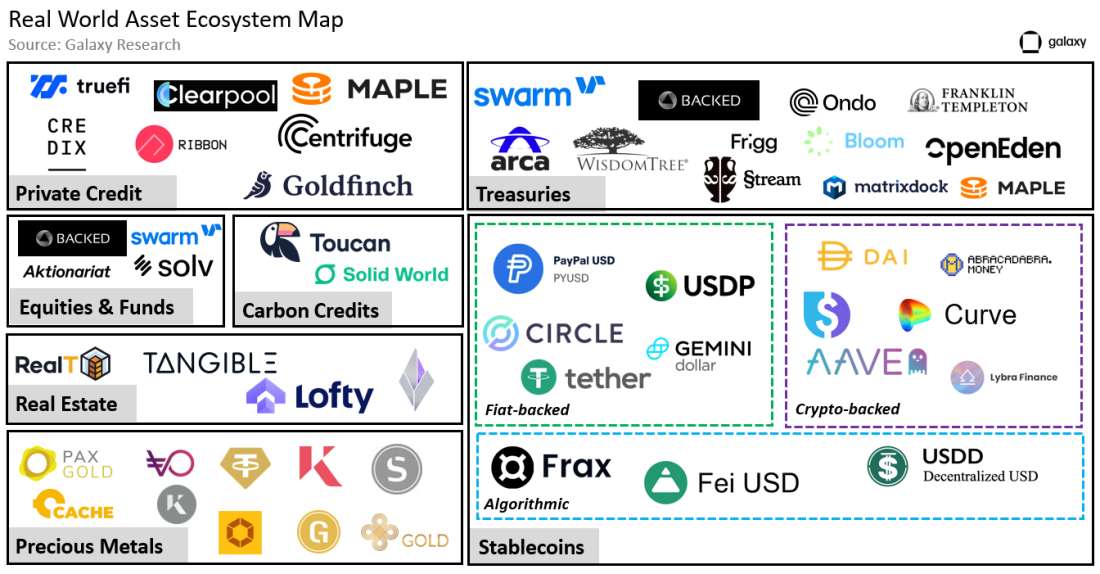

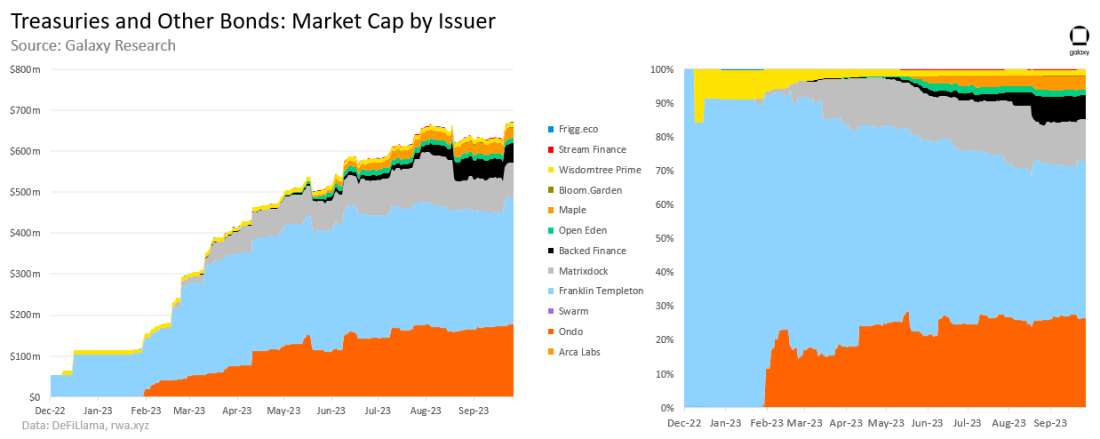

Some noteworthy RWA issuers include:

Centrifuge ($238m in actively issued RWAs) - the largest issuer of on-chain private credit loans.

Franklin Templeton ($310m in actively issued RWAs) – a traditional financial institution issuing tokenized Treasury tokens.

Wisdom Tree ($11m in actively issued RWAs) - an institutional capital marketplace issuing Treasury tracking funds.

This short list, plus the other issuers pictured in the image above, highlights the slew of off-chain entities that back on-chain RWAs. Franklin Templeton and WisdomTree are two veteran traditional finance companies whose primary business is unrelated to cryptocurrencies and blockchain technology. Franklin Templeton is a global investment firm of 76 years offering mutual funds, ETFs, and an assortment of other fund products to individuals and institutions. As a firm, Franklin Templeton manages more than 100 ETF and Mutual Fund products and holds $1.5 trillion in assets under management (AUM). WisdomTree is a global financial innovator founded in 1985. The company offers a diversified suite of exchange-traded products (ETPs), models, and solutions. WisdomTree has $95.948bn in AUM.

Over the past couple years, Franklin Templeton and WisdomTree have started to experiment with RWAs by tokenizing various traditional financial instruments such as tokenized equity-centric funds and Treasuries to service their institutional customers’ needs. Though these efforts are still nascent and in the early stages of development, the issuance of RWAs by veteran traditional finance companies has the potential to catalyze the onboarding of large swaths of new users to crypto that have never interacted on-chain before.

Yield-bearing RWA Growth

The market cap of RWAs stood at $2.49b as of September 30, which is 9.6% off the $2.75b all-time high reached on April 19, 2022. Despite strong growth from Treasury-bound RWAs, the sharp reduction in active loans from private credit issuers over the last 18 months has kept the market cap of RWAs under its all-time high.

Non-stablecoin RWAs have grown in value by $1.05bn from January 31 through September 30. $855.7m of this new growth over the past three quarters has come from Treasuries and other bonds, real estate, and private credit.

In the next section of the report, we will breakdown the growth observed in tokenized private credit, real estate, and Treasuries/ other bonds. We will also explain the differences between these types of RWAs and their yield generating qualities.

Private Credit

Private credit loans are a form of lending where financing is provided by non-bank institutions. Because banks have faced increasing regulation since the 2008 financial crisis, there has been significant growth in the private credit market with borrowers seeking auxiliary sources of capital. This trend has only expanded during the current rate cycle, with bank balance sheets particularly constrained (as demonstrated by the bank collapses earlier this year). Private credit solutions are beneficial for both borrowers and lenders. They give borrowers flexibility that bank loans lack; and their floating rates give lenders interest rate protection that fixed-rate alternatives don’t have. As of August 2023, the global private credit loan market is estimated to be worth $1.5 trillion.

The value of active on-chain private credit loans expanded by $210.5m (84%) from January 1 through September 30. Most of that rise (74%) came from Centrifuge, whose active outstanding loans grew by $155.7m. Clearpool, a decentralized credit marketplace, experienced the greatest relative change over the past three quarters. From January 1 to September 30, the platform’s loan balance grew 966%, reaching $23.96m by September 30. Cumulatively, Clearpool has originated more than $400m worth of private credit loans across 3 chains (Polygon, Polygon zkEVM, and Ethereum) in its lifetime.

Despite the growth in 2023, the value of total active private credit loans represented on-chain are still down 70% from the May 2022 all-time high of $1.54bn. Aggressive hiking from the Federal Reserve has coincided with a wide reduction in active loans, and higher yields to maturity over the 9-month period following the first interest rate hike back in March 2022.

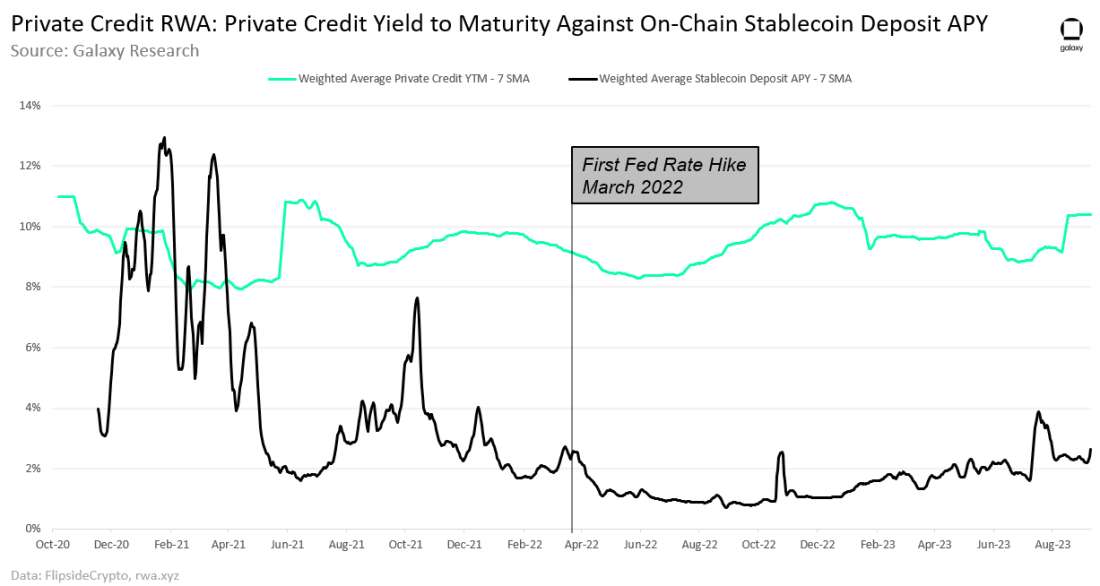

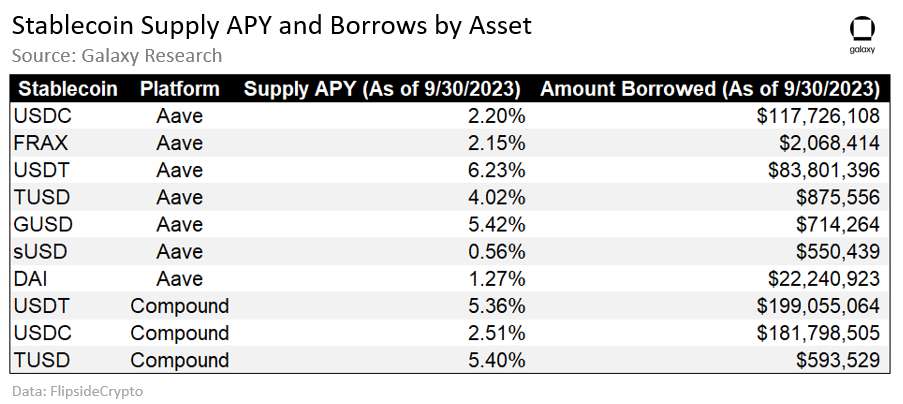

The yield users can earn by depositing their stablecoins for on-chain private credit loans is significantly higher than the yield users can otherwise earn for their stablecoins on DeFi lending protocols such as Aave and Compound. From January 1 to September 30, the average daily spread between yields from private credits loans tokenized on-chain vs a weighted average of Aave and Compound stablecoin supply rates has been 7.7%. The stablecoin deposit rate is calculated as a weighted average by amount borrowed on Aave and Compound for the following assets:

It is worth noting the differing risk profiles of depositing stablecoins into DeFi lending protocols like Aave and Compound versus depositing stablecoins into the likes of Centrifuge and Clearpool that offer tokenized representations of real-world private credit loans. While most loans issued on DeFi lending protocols are overcollateralized, the loans issued for tokenized private credit loans may not be. The implications of these risks will be further discussed in the Outlook section of this report.

Real Estate

Real estate is a tangible asset class that encompasses properties such as residential homes, commercial buildings, and land. Real estate is a particularly attractive asset class to investors because of its potential for positive cash flows from passive streams of income such as rental income. Real estate is the largest asset class in the world, capturing an estimated $613 trillion in value in 2023.

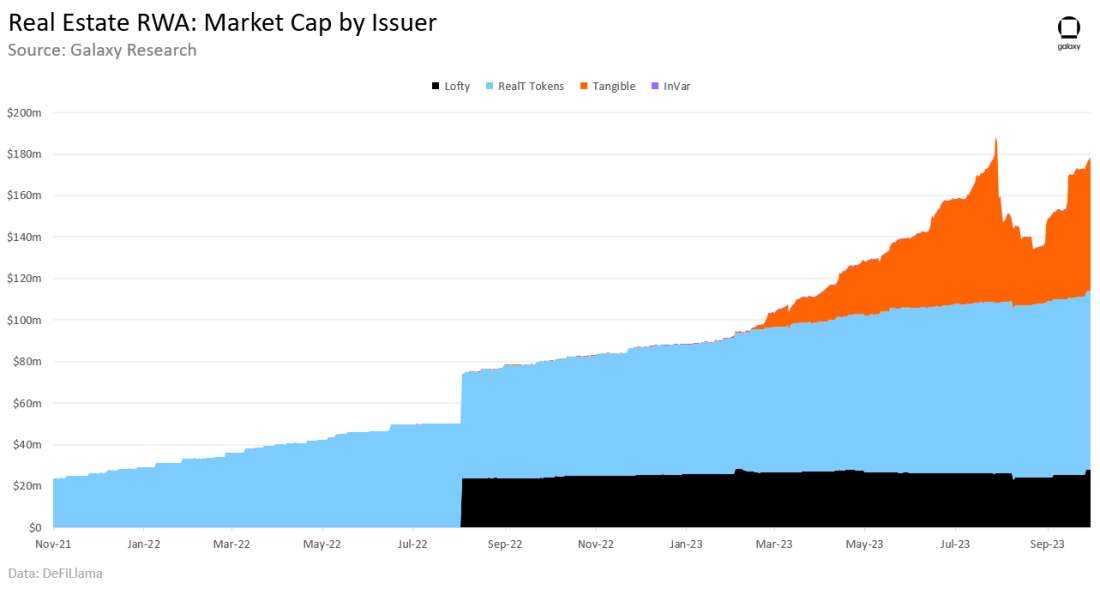

On-chain real estate grew the least in dollar terms of all the yield-bearing RWA categories covered in this report. These tokenized assets grew $90m in value (102% growth) from January 1 to September 30. The total value of tokenized assets, representing fractionalized claims on real estate in some cases, is $178m. RealT Tokens is the biggest issuer of tokenized real estate with a 49% market share. Tangible, another real estate focused RWA issuer, has seen the strongest growth this year. Total value locked in Tangible’s tokens grew from $100,000 to $64m over the first three quarters of 2023.

Treasuries and Other Bonds

U.S. Treasuries are government-backed debt securities. They are widely considered the safest and most reliable types of yield-bearing assets, known worldwide as “risk free” (to be clear, the risk is a U.S. government default). In contrast, corporate bonds are debt securities issued by companies, offering potentially higher yields but with increased risk compared to treasuries. In 2022, the global bond market was estimated to be worth $133 trillion and an estimated $1.02 trillion in corporate bonds was issued by US companies alone in the first three quarters of 2023.

Tokenized Treasuries and other bonds have grown in value by $557.05m from January 1 to September 30. Ondo Finance ($OUSG), Franklin Templeton ($FOBXX), and Matrixdock ($STBT) are the top 3 issuers of Treasury-bound RWAs. Together, they combine for $572.05m in issued assets (or 85% of the tokenized Treasury and other bonds category) and issued $468.5m of Treasury RWAs this year.

Frigg.eco is different from the other issuers in this category in that they issue bonds around sustainable infrastructure developers. These instruments are more like corporate bonds than the Treasury RWAs issued by the other parties in this sub-category. The bonds issued by Frigg.eco allow token holders to earn yield for funding developments and allow developers to issue debt that funds their initiatives.

Another notable tokenized Treasury asset with a market capitalization of roughly $1.8b is stUSDT. stUSDT is the first RWA project launched on Tron. Recently, the asset has been criticized for a lack of transparency behind its backing and sources of yield. Due to its uncertain nature, the token has been removed from RWA calculations in this report.

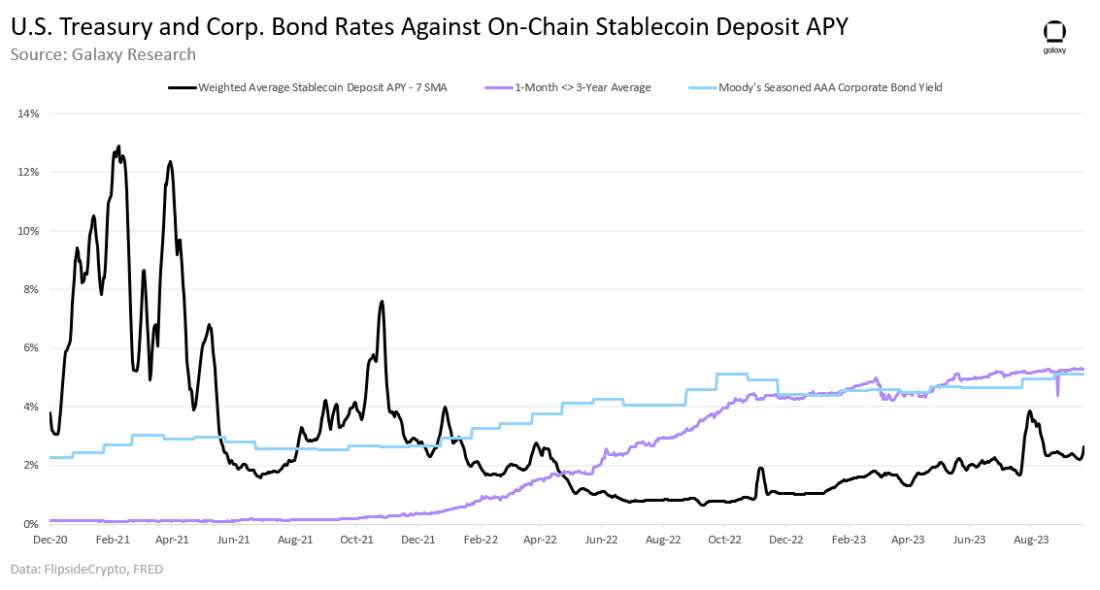

For nearly 18 months, the average yield achievable through U.S. Treasuries with durations less than 3 years (the most adopted on-chain U.S. Treasury durations) has trended higher than the average yield achievable through stablecoin deposits. The average daily spread between the rates of these treasuries and the weighted average of Aave and Compound stablecoin rates (average Treasury rate – on-chain rate) has been around 3% in 2023. This compares to an average spread between Moody’s AAA corporate bond yield and on-chain stablecoin yields (corp. Bond yield – on-chain rate) of 2.7%.

Outlook

Demand for yield from crypto natives is fueling the growth of on-chain RWAs. Roughly 82% of the new value created in the RWA sector this year has come from yield-bearing RWAs like tokenized private credit, real estate, and Treasuries. Of the total RWA market cap, the share of yield-bearing RWAs compared to non-yield bearing RWAs like gold, equities, and carbon offsets has nearly doubled over the past three quarters, growing from 31% to 53% from January 1 to September 30 (4% off the all-time high share of 57%).

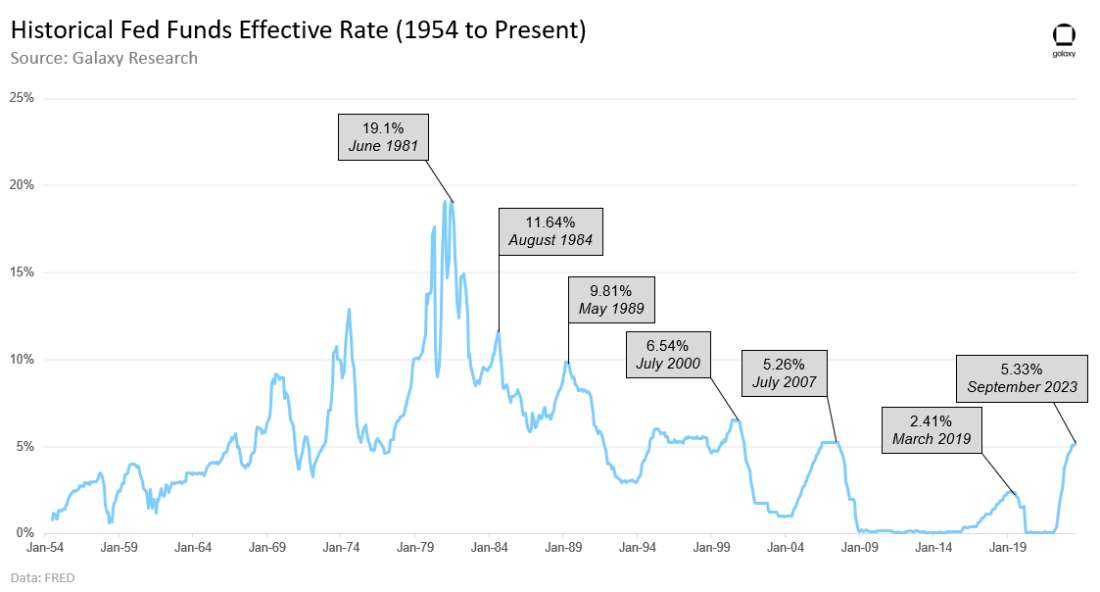

Aggressive shifts in the monetary policy of the Federal Reserve between 2021 and 2023 have taken benchmark interest rates to levels not seen since 2007. This has created newfound demand for certain types of RWAs from native DeFi users seeking higher yields on their crypto assets.

Most RWA Users Are Crypto Native

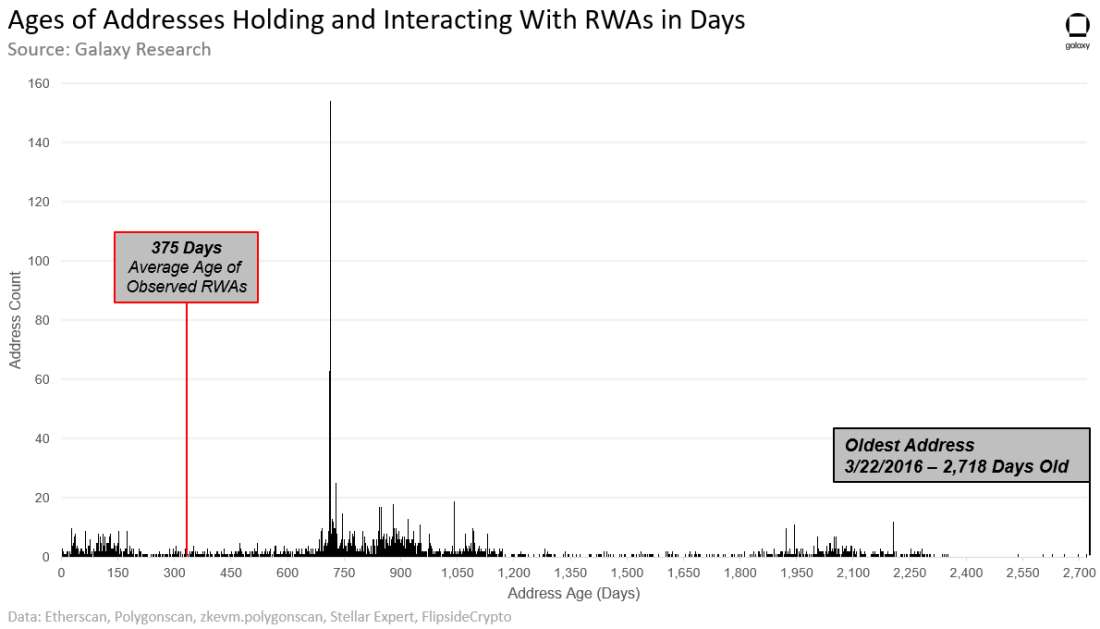

Most of the on-chain demand for RWAs is driven by a small number of native crypto users, as opposed to new crypto adopters or traditional investors moving onchain. The average age of user addresses interacting with RWA tokens predates the creation of these assets on-chain, and highlights that the average RWA holder has already been transacting on-chain for some time.

The below chart illustrates the age of unique user addresses holding RWA tokens that have been issued by the following companies and protocols. The ticker symbols for the RWAs issued by the following companies and protocols are listed in parentheses. These assets collectively represent nearly 70% of total yield-bearing RWA TVL:

Ondo ($OUSG),

Matrixdock ($STBT),

Maple ($MPLcashUSDT and $MPLcashUSDC),

Open Eden ($TBILL),

Backed ($bIB01 and $bIBTA),

Arca Labs ($RCOIN),

WisdomTree ($WSTY),

Swarm ($TBONDS13 and $TBONDS01),

Stream Finance ($US4W),

Bloom ($TBY-Feb1924, $TBY-mar24(a), and $TBY-mar24(b)),

Franklin Templeton ($FOBXX).

Note: the snapshot of these asset holders was taken on August 31, 2023. So, the age of addresses is counted as the number of days between an address’ first on-chain transaction and August 31, 2023. User addresses that hold multiple RWAs are counted once. Multiple addresses identified to be controlled by a single user are also counted once using their earliest transaction. The data tracks the age of addresses across all chains that the above assets are issued on which includes: Ethereum, Stellar, and Polygon. The following data also features the age of user addresses that hold tokenized representations of private credit issued by the following three protocols:

Clearpool on Ethereum and Polygon zkEVM,

Maple on Ethereum,

And Goldfinch on Ethereum.

As of August 31, there were 3,232 unique addresses that held RWA assets issued by the aforementioned companies and protocols. The average age of addresses holding and interacting with RWAs is 882 days, or 2.42 years. This means the average address has been on-chain since April 2021. Conversely, the average age of RWA assets is 375 days. For tokenized treasury assets, the ages of these types of RWAs were calculated as the number of days between the first token mint date and August 31, 2023. For the ages of assets issued by private credit platforms such as Clearpool, Maple, and Goldfinch, these are calculated as the number of days from protocol launch to August 31, 2023. For private credit RWA assets, using the protocol launch as the starting date for these assets’ age compensates for the rolling nature of on-chain private credit (i.e. loans mature/ pools are closed and new ones are open).

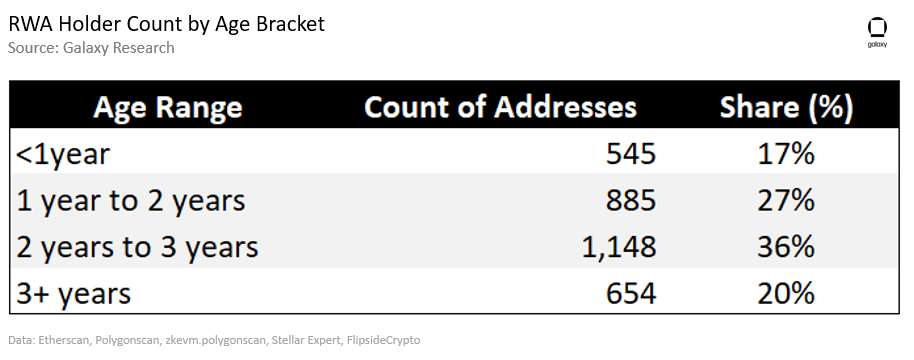

20% of addresses interacting with or holding the aforenoted RWAs started transacting on-chain more than three years prior to 2023 and the rise of RWA assets on-chain. The following table summarizes the age range of user addresses holding RWAs, as of August 31, 2023:

Many RWA holders that are highlighted above as having executed their first transaction less than one year ago are RWA holders of assets issued by Franklin Templeton and WisdomTree (34%, 188 addresses), indicating that the RWA products created by veteran financial firms may be succeeding in on boarding a newer suite of users into crypto, though the majority of RWA users still appear to be crypto-native users.

RWAs Mean Real World Risk and Limitations

While many RWAs are issued on public blockchains, they do not offer users permissionless access to financial products and services. In most cases, users interacting with RWAs on-chain are required to complete KYC/AML or whitelist verification, accreditation checks, and possibly meet minimum balance requirements to mint, purchase, deposit, and/or redeem RWAs. RWAs are gated by similar, or in some cases more, limitations than their traditional financial counterparts. This means RWAs are not broadening access to financial instruments by enabling individuals to engage in financial activities that they would otherwise not be able to access.

Further, there are unique risks associated with RWAs, in addition to the technological risks that are associated with all on-chain applications and services. For example, since private credit lending in traditional finance is unsecured in some cases, the tokenized representation of private credit loans must also reflect this reality. If a borrower off-chain defaults on their loan, then on-chain depositors can lose funds. To compensate for such risks on-chain, RWA private credit issuers must find ways to position assets along a risk/return spectrum using tranches and vet new loans through transparent processes of on-chain governance, usually involving decentralized autonomous organizations (DAOs). (Read this Galaxy Research report for more information about DAOs.)

Fed Policy Matters

The actions of the Federal Reserve have contributed heavily to the popularity of RWAs this year. Off-chain yield has become more attractive for on-chain users because of interest rate hikes. Additionally, the most valuable types of RWAs have changed as interest rates have increased. For example, in Q2 2022, private credit-backed RWAs made up as much as 56% of total RWA TVL while the share for Treasuries-backed RWAs made up 0%. In Q3 2023, the share of total RWA TVL from private credit-backed RWAs declined to 18% while the share from Treasury-backed RWAs increased to 27%. Fed policy acts as a strong hand influencing the expansion and topography of the RWA DeFi sector.

Conclusion

The growth of RWAs, and the introduction of new types of RWAs onchain, is primarily driven by demand from native crypto users as opposed to new crypto adopters. However, there are early signs of adoption for RWAs by major traditional financial companies like Franklin Templeton and Wisdom Tree that illustrate the potential for this budding sector of DeFi to attract new users in the future. Momentum for RWAs has grown in 2023 and the market value of many of these assets are trending towards new all-time highs. The evolving macro environment will continue to influence the evolution of this sector, as will continued demand for these types of assets from native and non-native crypto users alike.

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2023. All rights reserved.