Executive Summary

The impact of real-world assets (RWAs) goes beyond simply tokenizing off-chain assets and reflecting them on-chain. RWAs also enable new models, products, revenue, and strategic partnership opportunities for decentralized applications (dapps). In our last report on RWAs, we discussed the catalysts for the growth of the RWA narrative and the types of RWA tokens that have been gaining traction in 2023.

In this report, we highlight:

the ways established non-RWA focused decentralized finance (DeFi) applications have incorporated RWAs into their protocols,

the risks associated with DeFi-based RWA strategies,

and the broader impact RWAs may have on the evolution of DeFi over the long-term.

For background on the types of tokenized RWAs that exist on-chain and the entities issuing these tokens, read our previous report.

Key Takeaways

MakerDAO, Frax Finance, and Aave are non-RWA focused DeFi protocols that have incorporated off-chain assets into their products and services and decentralized autonomous organization (DAO) frameworks.

MakerDAO is using RWAs as collateral for its stablecoin, DAI. The protocol’s incorporation of RWAs has benefitted the economic health of the MakerDAO protocol and DAI stablecoin.

The Frax Finance development team is also using RWAs to improve the stability of its stablecoin, FRAX, and create unique DeFi yield products like Frax Bond tokens.

The Aave DAO is using RWAs to generate revenue from the crypto-native assets under its management that would otherwise be idle and unproductive.

RWAs have the potential to improve the stability and efficiency of on-chain DeFi products and services. However, they also bring unique risks due to their off-chain nature, such as the reliance on centralized third-parties to acquire and custody RWAs.

Introduction

The three most common types of RWAs being incorporated into the design of DeFi applications are:

Off-chain private credit lending

Treasury securities

Other off-chain yield generating tools and cash equivalents (e.g. shares in money market funds, and repurchase agreements)

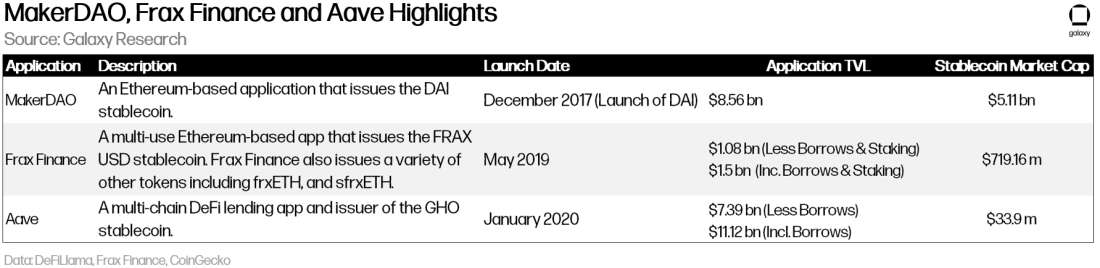

MakerDAO, Frax Finance, and Aave are leading examples of DeFi protocols that have leaned on RWAs. These protocols are among the earliest and largest DeFi applications in the crypto ecosystem. The following is an overview of the main functions and market value of these three DeFi protocols as of January 17, 2024:

These three DeFi protocols have incorporated RWAs into their services in the following ways:

RWAs as a new yield product for end-users.

RWAs as a new collateral type for stablecoins.

RWAs as a treasury management tool to bolster DAO revenues and thereby help fund continued protocol development.

In this report, we will provide a detailed overview of how RWAs are being used in MakerDAO, Frax Finance, and Aave, as well as the risks associated with RWA integrations in DeFi. Finally, we will discuss the impact and outlook of these integrations on the development and maturation of the DeFi space.

RWA Integration in DeFi: Benefits

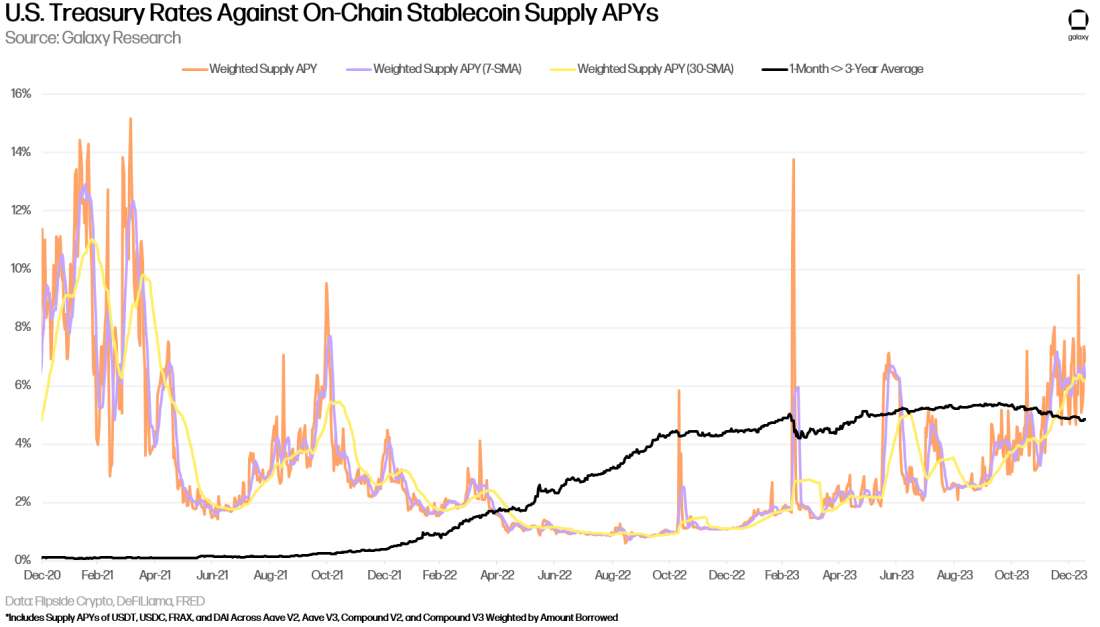

The adoption of RWAs by DeFi protocols can dampen the cyclical nature of on-chain yields by taking advantage of the inverse relationship in demand between crypto-native assets and off-chain assets. The chart below depicting U.S. treasury rates against stablecoin yields illustrates this dynamic:

From December 2020 to roughly April 2022, stablecoin yields were relatively high while Treasury rates in contrast were low. From April 2022 to late November 2023, as the average rate for 1-month to 3-year U.S. Treasury Bills increased, on-chain yields declined and consistently stayed below T-Bill rates.

The implementation of RWAs on-chain allows users to benefit from real world interest rates when they can offer more attractive yields than crypto-native sources, and vice versa when on-chain rates are more attractive. RWAs have the potential to help optimize on-chain yields and create a steadier rate environment that reduces cyclicality in DeFi protocol use, yields, and revenues.

RWAs can also be used within existing DeFi protocols to improve the stability, efficiency, and effectiveness of protocol operations and functionality. For example, Frax Finance’s introduction of a DeFi-native yield curve that relies on tokenized bonds has introduced a new way for end-users to price risk on-chain and position their DeFi portfolios. It also gives the protocol an outlet to raise funds through debt auctions in ways similar to that of off-chain entities. If RWAs are successfully implemented and widely adopted among existing DeFi protocols, DeFi end-users stand to gain from the exposure to more mature traditional financial products. These ideas will be illustrated in more detail later in this report when we discuss MakerDAO’s and Frax Finance’s use of RWAs.

RWA Integration in DeFi: Risks

RWAs can bring operational and economic benefits to the on-chain economy through the development of innovative supporting infrastructure harnessing both on-chain and off-chain assets. However, there is the danger of overreliance on off-chain assets for stability and yield. Simply emulating off-chain processes, procedures, and products across DeFi, rather than supplementing crypto-native products, services, and development with the unique characteristics and assurances of off-chain assets can lead to outsized risks associated with disruptions and lack of technological advancement. The following are four major risks to the integration of RWAs in existing DeFi protocols:

Real World Events

First and foremost, the integration of RWAs in DeFi can make DeFi dapps more sensitive to real world events. The global economy already has an impact on the demand for crypto-native assets, but the inclusion of RWAs in DeFi may introduce new operational risks to DeFi protocols. For example, changes in DeFi policy and regulation around the world in different jurisdictions may more directly impact a DeFi protocol relying on RWAs by limiting the extent to which it can offer its products to users based on their geographic location. Additionally, changes to global rates policies extrinsic to crypto markets, such as central bank policy, will now more directly impact onchain DeFi activity.

Default and Asset Redeemability

DeFi protocols must be careful with partner selection in the case of some RWAs, particularly private credit. US Treasuries and cash equivalents are more sheltered from default risk than private credit lending, as the entity issuing them (such as the US government) is considered very unlikely to not pay their obligations, while private credit is more prone to default. For example, a private credit loan used to collateralize the dollar-pegged stablecoin DAI went into default back in August 2023 after the borrowing companies, Hanhwa AUS Pty Ltd and Hanwha New Zealand Pty Ltd, were ordered by the Australian Supreme Court to unwind all their financial activities and positions including freezing payments to debtors. There are many such cases of loan defaults in the real world across several private credit platforms.

On a similar note, redeemability risk can hinder a protocol’s access to its off-chain assets under certain circumstances. Some RWAs, like Treasuries, can take several days to be sold and accessed in the traditional finance markets. Further, traditional financial assets brought on-chain may not be traded all hours of the day and all days of the year like crypto-native assets can (though there are innovations in off-chain infrastructure that can mitigate this risk over time). Off-chain RWA providers can also experience downtime and technical malfunctions (as can blockchains and blockchain-native protocols). DeFi protocols must account for the unique characteristics and procedures around RWAs and be selective in the groups that help them facilitate operations involving them.

Third-Party Entities

MakerDAO, Frax Finance, and Aave use centralized third parties to acquire and custody RWAs. Maker does so through Monetalis Clydesdale, BlockTower, Coinbase Custody, and others that acquire and custody assets on the protocol’s behalf. Aave’s is handled by Centrifuge Prime. Frax uses Centrifuge Prime and FinresPBC in conjunction with Lead Bank. The protocols’ relationships with third party custodians that can purchase real world assets on their behalf facilitate the integration of RWAs into their frameworks, through both custody and trading. These partners also allow the protocols to capitalize on a spectrum of traditional financial offerings offered by the custodian such as non-bank trade finance.

At the same time, these relationships expose new risks. The protocols must trust that funds deposited with the third-party are not abused, hypothecated, or otherwise used for purposes beyond the scope of their agreement. The reliance on third party custodians also comes at a financial cost to the DeFi protocol in some cases that may detract from the net benefit of integrating RWAs for end-users. Further, reporting on RWA holdings and operations can get complicated if multiple third party custodians are used, as in the case of Maker.

Frax Finance’s use of FinresPBC (onboarded through FIP-277) to acquire the RWAs integrated into the protocol is unique. This entity is a public benefit Delaware C corporation that acts solely to provide the Frax Protocol access to RWAs for the direct benefit of the protocol alone, without seeking to make profit from this relationship or any others outside of it. The benefits this approach has over the relationships predominantly used by Maker and Aave are three-fold:

increased transparency of the conduit,

the conduit acts in the interests of the protocol and costs of the relationship and counterparty risk are limited,

the conduit is flexible around the specific needs and functionality of the protocol.

However, the tradeoffs of this approach include direct overhead and human capital costs, and the heightened responsibility on the protocol and protocol governance token holders for the continued maintenance, operation, and proper reporting of the conduit to end-users and regulatory authorities.

Off-Chain Asset Monitoring

Proper auditing of off-chain funds, assets, and parties is important to the integration of RWAs in DeFi. It ensures off-chain providers and parties aren’t acting maliciously, misusing protocol owned assets, and that they hold what they say they hold. It also ensures the protocols using off-chain assets are kept in check and offer what they say they offer. In the case of private credit, this means ensuring borrowers are following the guidelines of loans and are not putting loan backers’ assets at risk in ways beyond the scope of the loan terms. Goldfinch faced this issue when a borrower used funds without making backers aware of what they were doing. The result ended in lost funds that were ultimately made whole by the borrower, Warbler Labs. In the case of RWA collateralized stablecoins, this means proving the fidelity of the assets that back the tokens.

Proving the ownership of off-chain assets to end users on-chain can be challenging. APIs, oracles, and other means of communicating details about off-chain account balances play an important role in the monitoring of RWAs. These monitoring tools for RWAs must be paired with the auditing of crypto-native assets and funds to provide end-users with a complete audit of DeFi products and services.

In the next three sections of this report, we will give a detailed overview of three practical RWA implementations in DeFi by examining the use of RWAs in MakerDAO, Aave, and Frax Finance.

MakerDAO

MakerDAO was one of the first DeFi protocols to integrate RWAs into its product at scale, with the first vote among MKR token holders to do so passing in November 2020. Since then, RWAs have become an integral component of MakerDAO’s economic success and the DAI stablecoin.

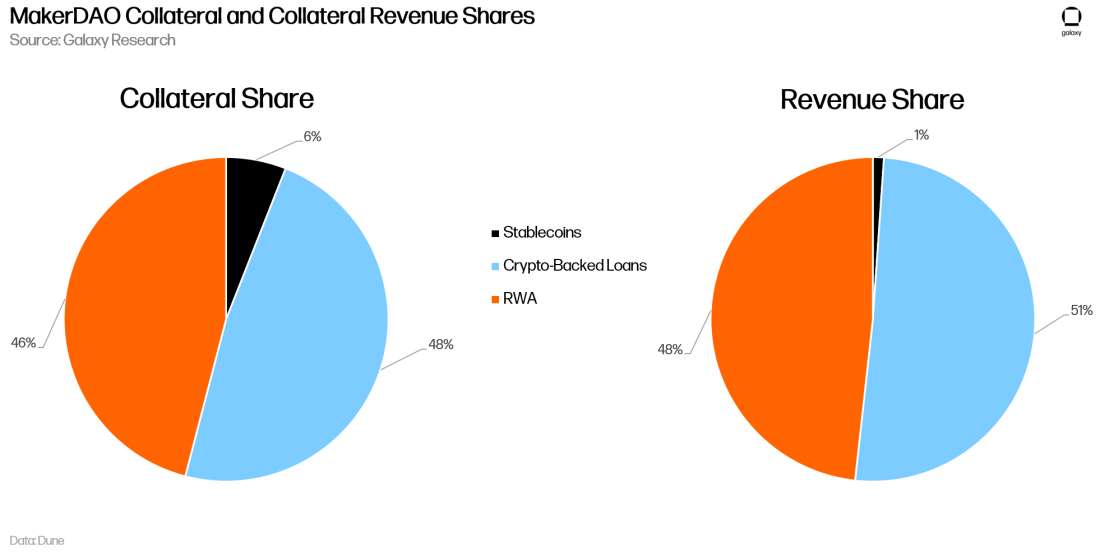

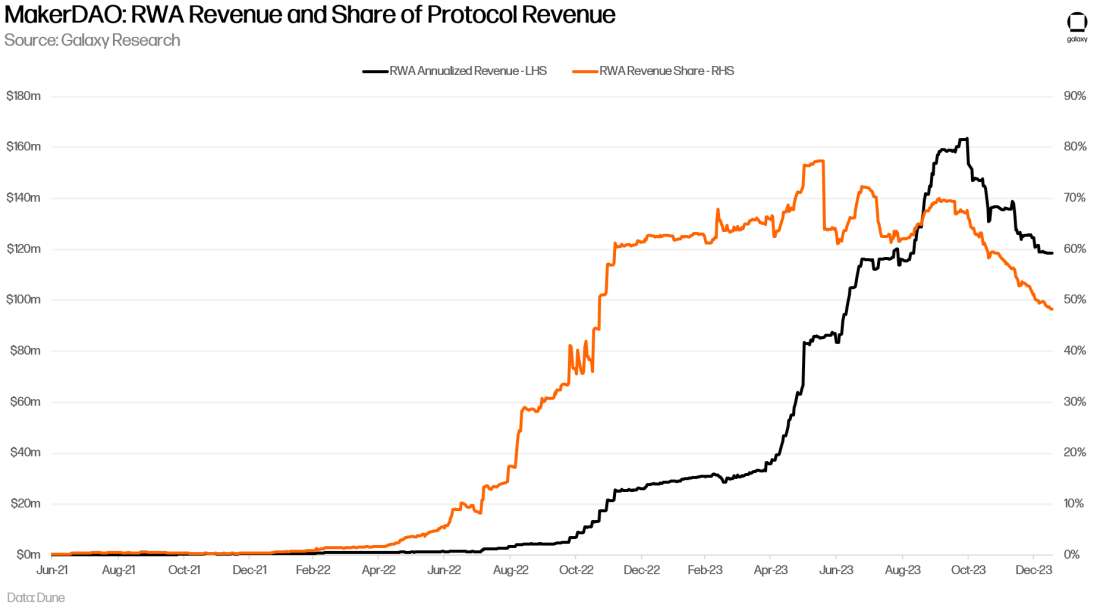

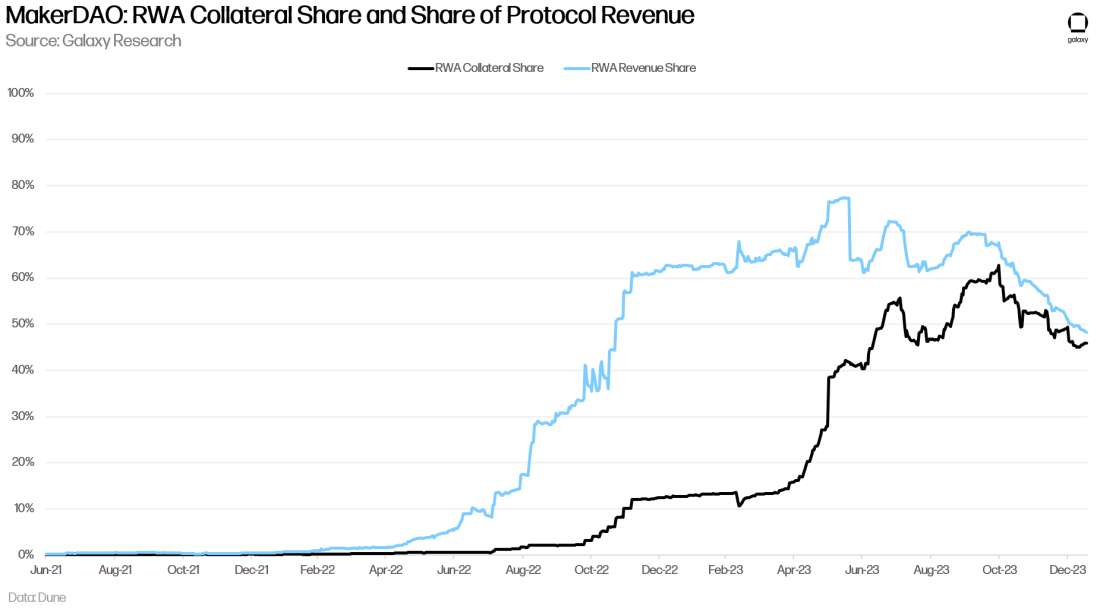

Around 46% of DAI in circulation are collateralized by RWAs, and 48% of MakerDAO’s estimated annualized revenue comes from the collateral type.

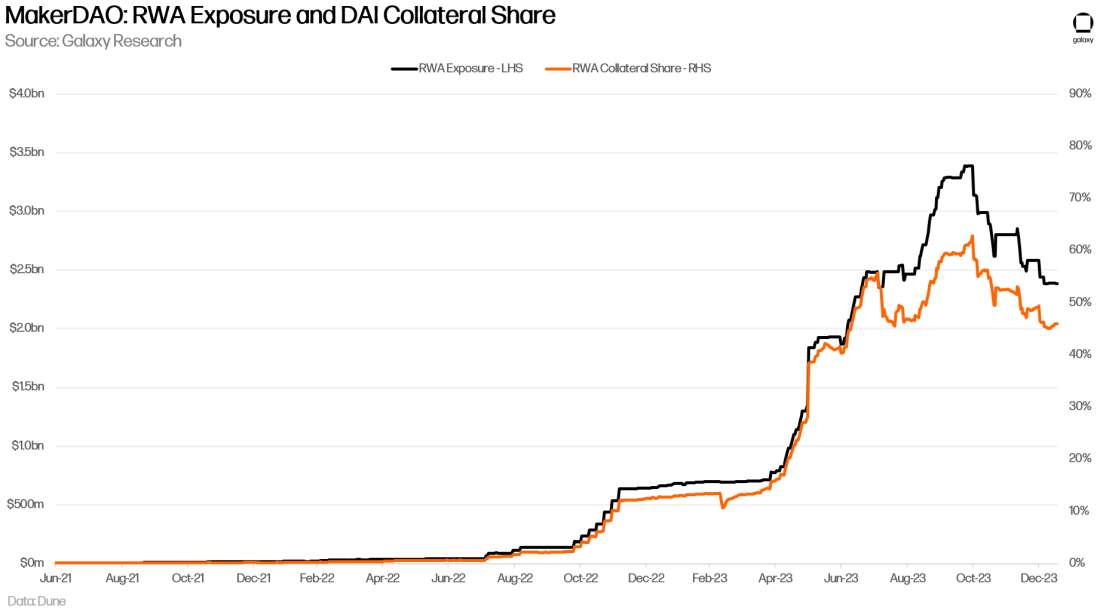

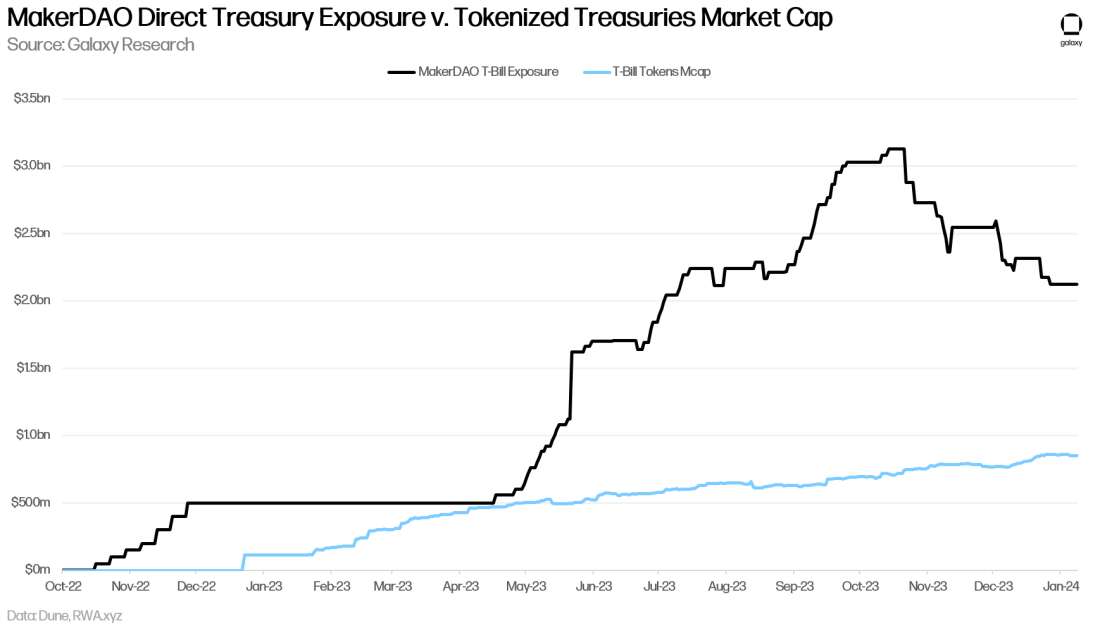

The protocol has been growing its exposure to RWAs in relative and absolute terms. It now has $2.4b worth of exposure to RWAs, representing growth of $1.73b (267%) since this time last year. However, MakerDAO’s RWA exposure has dropped about $1b (42%) from its high of $3.4b after seeing reductions in the DAI issued in the Coinbase Custody, Monetalis Clydesdale, and BlockTower Andromeda collateral vaults. These vaults were drawn down to bolster USDC-PSM liquidity in October 2023, November 2023, and December 2023.

The share of revenue coming from RWAs has grown in tandem with collateral share of DAI in circulation. They capture $118.5m of $245.6m in total protocol revenue on an annualized basis as of January 17, 2024.

Historically, the RWA share of MakerDAO revenue has exceeded its collateral share, meaning RWAs generate a greater portion of Maker revenue than the share of DAI issued against them. In Q1 of 2023 the spread between revenue share and collateral share from crypto native assets reached 48.2%. As of January 17, 2024, it is just 2.3%. Two forces have been narrowing the spread: 1) the growing amount of onchain crypto-backed loans being used to mint DAI and 2) swelling onchain rates as a result of renewed activity allows Maker to carry higher stability fees for onchain debt collateral. More details on both of these points will be covered below in MakerDAO’s RWA strategy.

Overall, the trend highlights the historical revenue generating robustness of RWAs when onchain revenue generating opportunities are sluggish.

The tokenized market cap of treasury RWA tokens is $852m (all time high of $862m), while Maker’s direct exposure to treasuries exceeds $2.1b (all time high of $3.1b) as of January 17, 2024. This underscores the massive role that RWAs are playing in supporting the products and services of existing DeFi protocols, like MakerDAO, that surpasses the value of similar RWAs issued on-chain directly to end-users through RWA-focused tokens. It also highlights the importance of dapps and utility to the scalability of RWAs on-chain.

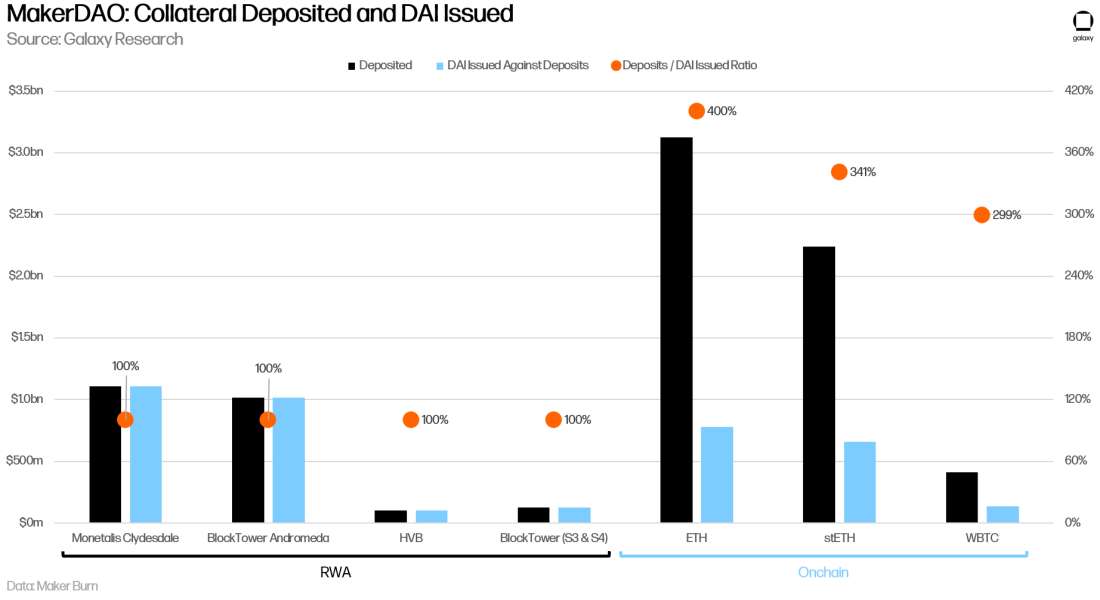

Comparing collateral deposits and DAI issuance amounts further highlights the relative efficiency of RWAs in MakerDAO operations. RWAs hold a 100% collateral ratio, meaning $1 of RWAs mints $1 worth of DAI. This compares to other collateral types, like ETH, stETH, and WBTC, which require a minimum of $1.30 to $1.75 to mint $1 of DAI (collateral ratios of at least 130% to 175%). In practice, they hold collateral ratios between 299% and 400%. RWAs offer a significantly more capital efficient way for DAI to be issued, even compared to yield-bearing on-chain assets like stETH.

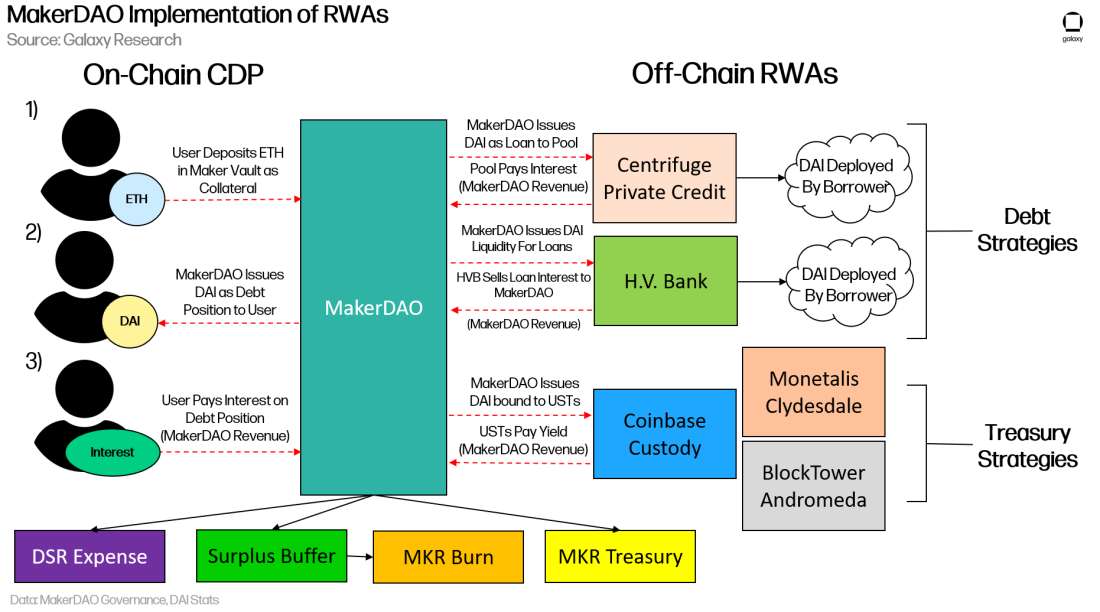

MakerDAO’s RWA Strategy

MakerDAO’s RWA strategy is part of a larger initiative to build a resilient, decentralized, and revenue-generating stablecoin. To achieve this, the protocol has on-boarded multiple types of RWAs and RWA strategies according to different terms, sources, and processes. This was done intentionally in accordance with the DAO’s goal of diversifying the backing of DAI to the greatest extent possible. However, the RWAs captured by Maker have one common characteristic: they all generate yield that accrues to the DAO as revenue.

The mechanics and implementation of major RWAs in MakerDAO are pictured below. Note, this is a simplified visualization used for the purpose of illustrating Maker’s integration of RWAs. The detailed dynamics of the underlying relationships and off-chain processes that make the strategies possible are not illustrated in the chart below.

The interest rate paid by users minting DAI through on-chain collateralized debt positions (CDPs) and off-chain debt is called the “stability fee.” In the case of on-chain CDPs, this fee is variable and determined through governance. In the case of RWAs, the stability fee is determined by off-chain forces such as the interest rate paid out on T-Bills or interest of off-chain loans. The stability fee is the cost to mint DAI (or get DAI liquidity) for an end-user and accrues to the protocol in DAI as revenue. The Maker protocol also earns revenue from the liquidation of users’ debt positions if their loans become impaired. This occurs when the value of a user’s DAI collateral falls below the threshold determined in advance by the collateral asset’s vault conditions.

As mentioned, the stability fee associated with minting DAI through U.S. treasury bills (T-Bills) is not determined through governance. Instead, the stability fee is equivalent to the rate paid out by the underlying T-Bills or T-bill related strategy. MakerDAO does not accrue additional revenues through the stability fee beyond the interest rate for T-Bills. Though protocol revenue from stability fees accrues to the DAO, these revenues also benefit users, specifically DAI and MKR token holders, through the DAI savings rate and MKR token buybacks, respectively.

DAI Savings Rate

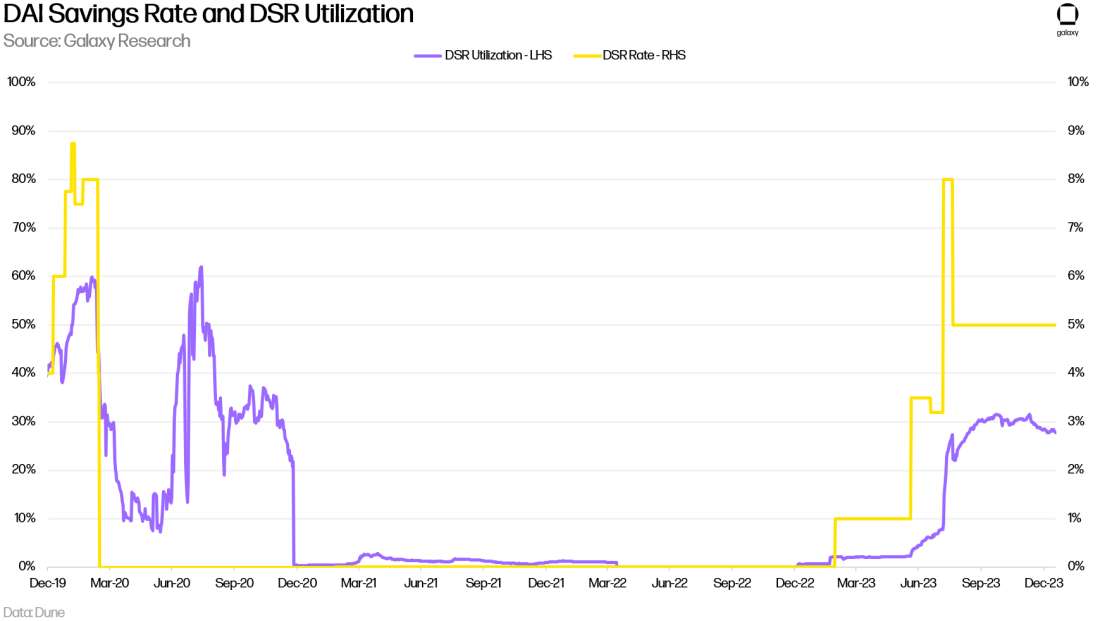

MakerDAO’s DAI Savings Rate (DSR) vault functions like a savings account for DAI token holders. It allows DAI holders to deposit their stablecoins into a smart contract and earn interest on their deposits. The smart contract is modelled after ERC 4626, which is a popular extension of the ERC 20 token standard for building yield-bearing vaults. The yield on staked deposits is determined by Maker governance and updated as the community sees fit. The rate offered is typically less than the average stability fee to issue DAI, as the proceeds funding the DSR come from protocol revenue.

The EDSR (Enhanced DAI Savings Rate) adds a multiple to the DSR that fluctuates in accordance with the share of DAI deposited into the DSR. When the share of DAI deposited into the DSR increases, the EDSR declines, and vice versa. The EDSR is not a separate rate from the DSR. It is simply a multiple that increases the effectiveness of the DSR vault that is made available to DAI depositors on an ad hoc basis. This mechanism was introduced to spark increased demand for DAI and make the stablecoin competitive with other yield generating opportunities on-chain.

While the DSR can be used as a device to attract users to DAI, it comes at a cost. On an annualized basis, the amount paid to DSR depositors topped 118m DAI on August 19, 2023 (1.478b DAI in DSR at 8% APY). As of January 17, 2024, the annualized amount paid to DSR depositors is 71.88m DAI (1.44b DAI in DSR at 5% APY). This cost has direct implications on MakerDAO and its economic health as revenue earned by the DAO funds the DSR, as well as other protocol costs, including the MKR burn engine, which will be discussed in the next section of the report, and the surplus buffer, which is a reserve of DAI accumulated from protocol earnings. It is used to fund various functions of the MakerDAO protocol, including the Maker Smart Burn Engine and backstopping bad debt built up from overleveraged vaults.

The DAO must weigh out the costs and benefits of allocating its revenues judiciously for the long-term sustainability of the protocol. In August 2023, MKR token holders passed a governance proposal reducing the maximum EDSR from 8% to 5% in efforts to implement more conservative policies that restricts how much protocol revenues can be used to fund the DSR.

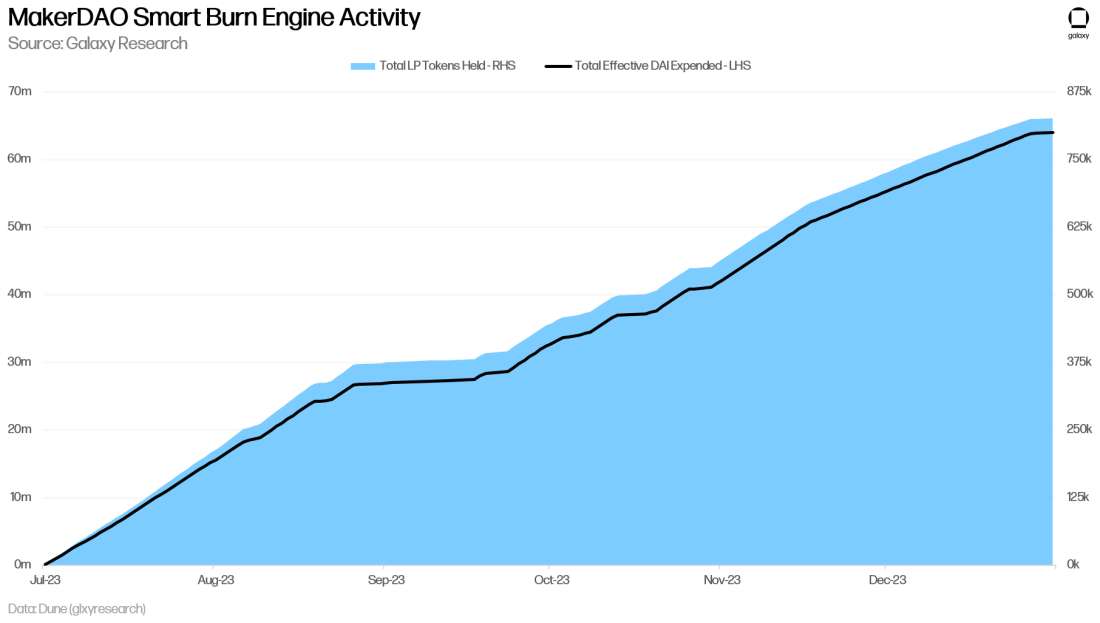

MKR Smart Burn Engine

The second way protocol revenues indirectly benefit users is through the MKR smart burn engine. In June 2023, MKR token holders passed a governance proposal titled, “Introduction of Smart Burn Engine Launch Parameters”. The smart burn engine is an iteration of the protocol’s previous MKR token burning effort that buys back MKR tokens through Uniswap v2 LP (liquidity provision) tokens. In the past, the DAO bought back MKR tokens on decentralized exchanges such as Uniswap using protocol revenues and burned them. This in turn benefitted MKR by creating a demand stream for the token and putting deflationary pressure on its supply. The updated smart burn engine has a similar effect but doesn’t burn MKR tokens.

Instead of burning MKR tokens, MakerDAO is building an LP position in the DAI-MKR Uniswap V2 pool. The MKR tokens it acquires are paired with additional DAI and deposited into the pool. Upon launch, the DAO was buying MKR tokens in 5,000 DAI bundles every 1,577 seconds any time the surplus buffer exceeded 50m DAI (DAI funding the smart burn engine is sourced from the surplus buffer). This totals the acquisition of 100m DAI worth of MKR per year nominally, or 200m DAI worth effectively (as MKR acquired is paired with DAI on a 1:1 basis for the LP position, so every 1 DAI of MKR buybacks must be paired with an additional 1-unit of DAI). These parameters stay in compliance with MIP 104: 9.1.2.1 that set the target rate of DAI usage for MKR burning. A proposal updating smart burn engine parameters passed on August 7 to 20,000 DAI of MKR buybacks at 6,308 second intervals. The longer time interval ensures higher gas cost savings from MKR buybacks.

Maker builds the LP position by purchasing MKR on Uniswap v2, matching it with an equivalent amount of DAI, and depositing both the MKR and the DAI it into the Uniswap v 2 MKR-DAI pool together. In exchange for being a liquidity provider, the DAO receives LP tokens representing its deposit. LP tokens are equivalent to a coupon proving a user’s deposit into a liquidity pool. The coupon entitles them to benefits, such as the fees generated by the users swapping the assets in the pool. Once acquired, the MKR-DAI LP tokens are held in an address owned by MakerDAO.

By using DAI from the surplus buffer to build liquidity for the MKR-DAI pool, the DAO builds liquidity for its token by putting upward pressure on the amount of MKR and DAI in the pool. This also creates a demand stream for MKR tokens by purchasing them to pair with DAI for its LP position. Since launching, the DAO has effectively expended around 64.03m DAI from the surplus buffer and amassed more than 826.5k MKR-DAI LP tokens through the smart burn engine as of January 17, 2024. It’s important to note that MakerDAO is exposed to all of the risks of normal LPs as it accumulates MRK-DAI LP tokens, namely impermanent loss. It also capitalizes on the benefits of being a liquidity provider by capturing fees generated by users swapping between MKR and DAI in the pool.

In summary, MakerDAO is using RWAs as collateral for its stablecoin. Whenever DAI is minted, the protocol generates revenue through the stability fee, or the yield generated by the underlying RWA. Protocol revenues directly accrue to the DAO but indirectly benefit users through the DSR and MKR buybacks. Through RWAs, the DAO can issue DAI in more capital efficient and economically advantageous ways that increase the protocol’s capacity to offer products such as the DSR and MKR smart burn engine; all while diversifying the backing of its stablecoin.

Frax Finance

In October 2023, Frax Finance introduced a 2-pronged RWA product and a reformed stablecoin collateralization strategy with its roll out of Frax v3. The v3 upgrade, which formally went live on October 12, announced two new tokens:

sFRAX. These tokens represent staked FRAX tokens earning yield from RWAs. The yield earned by these assets is deposited into the sFRAX vault and can be redeemed by users upon unstaking their sFRAX. sFRAX is not a rebasing token. Instead, the value of sFRAX continuously rises against FRAX as yield accrues.

FXBs. Frax Bond tokens (FXBs) are flexible utility tokens representing FRAX stablecoins that function like zero-coupon bonds with a predefined maturity timestamp. These tokens bear the assurance of earning a fixed yield over a period of time that best aligns with users’ investment strategies. Together, FXBs of varying maturities introduce the formation of an on-chain native yield curve.

In addition, Frax v3 supports the overcollateralization of FRAX by incorporating RWAs into its collateral mix. A goal of the v3 upgrade was to better facilitate the transfer of yield from off-chain assets to on-chain DeFi products and thereby enhance the stability and efficiency of the FRAX stablecoin.

Frax Before and After v3

At its launch in December 2020, FRAX was a fractionally reserved algorithmic stablecoin, meaning the stablecoin had a collateralization ratio (CR) less than 100%, but greater than 0%, at any time and was backed by another crypto-native token, FXS. Frax Finance used a price-stability algorithm that would automatically calculate the amount of FXS needed to mint FRAX based on the market value of FXS. The protocol effectively relied on market dynamics to determine how much FXS collateral was necessary for FRAX to maintain a value of $1.00 USD. At the time, the FRAX stablecoin protocol was an innovative stablecoin design in DeFi.

In February 2022, FXS token holders, that is Frax Finance governance tokens holders, voted on a proposal to increase the protocol’s CR to 100%. This was around a time when algorithmic stablecoins became increasingly brought into question as Terra’s UST reached nearly $20b in market cap. Its collapse in May 2022 led to the outright rejection of algorithmic stablecoins by the crypto community at large. The passing of this proposal, FIP-188 (snapshot vote), marked the beginning of Frax Finance’s move away from an algorithmic and fractionally reserved stablecoin design toward an over-collateralized one. The launch of v3 and incorporation of RWAs is the continuation of the protocol’s initiative to move toward an over-collateralized stablecoin model like DAI.

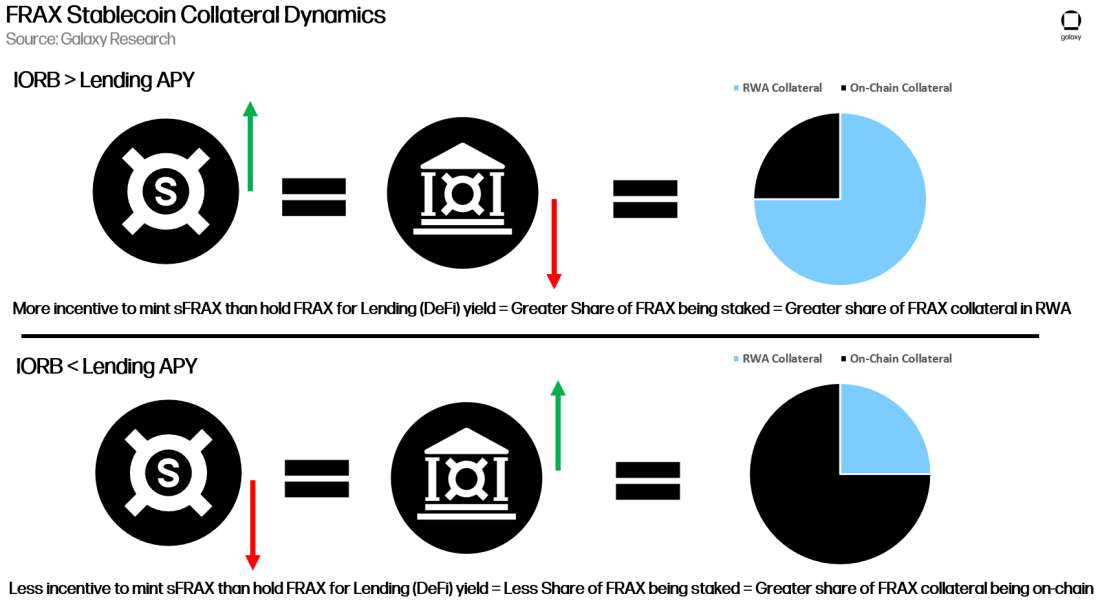

RWAs play an integral role in Frax Finance v3. The protocol now utilizes an oracle that tracks the interest that banks earn from the U.S. Federal Reserve, also called the Interest on Reserve Balances (IORB) rate. This benchmark rate is generally accepted as the “risk free rate” of the US Dollar and U.S. economy. Though considered the safest asset in the world, even U.S. government bonds are not without some risk. The risk is a U.S. government default.

When the off-chain IORB rate exceeds what is achievable lending FRAX through DeFi lending protocols like Aave and Fraxlend, users are incentivized to stake their FRAX in the sFRAX vault. Once staked in the vault, FRAX is then converted by Frax Finance through FinresPBC to USDC, USDP, or other stablecoins which are used to purchase off-chain RWAs that collateralize sFRAX. More users will presumably stake their FRAX as incentive to do so grows, which pushes an increasing share of FRAX collateral into off-chain RWAs.

The inverse occurs when the IORB rate declines and on-chain rates rise. In this environment users will redeem their sFRAX for FRAX to lend across DeFi. In some instances, users may also sell or redeem their FRAX entirely. As this happens, the off-chain RWAs are sold for the stablecoins they were purchased for back into FRAX, and the proceeds get pushed back on-chain via automated market operations contracts (AMOs) and through users unstaking their sFRAX. This allows users to redeem their sFRAX tokens and create new FRAX via over-collateralized loans backed by crypto-native assets. Over-collateralized FRAX loans are like MakerDAO’s issuance of DAI through on-chain CDPs. In this scenario the backing of FRAX becomes dominated by crypto-native assets rather than RWAs.

In summary, the mechanisms explained above that uphold the value of FRAX under the v3 model is illustrated in the following diagram:

The fluid and incentive driven collateral strategy of FRAX insulates the stablecoin from the cyclical nature of both off-chain and on-chain markets. The Frax Finance protocol does this by creating incentives for users to benefit from both collateral types and seamlessly switch between the two at their discretion as one becomes more attractive than the other. These dynamics also help reinforce the stability of the stablecoin’s peg by assisting it in bringing its collateral ratio to the 100% + target outlined by FIP-188. The original vision of FRAX as an innovative, market driven, and fractionally reserved algorithmic stablecoin does not appear to be lost in Frax v3. It still holds a market driven, algorithmically adjusted collateral mechanism that is “fractionally” backed by multiple collateral types (that is, for example 50% RWAs / 50% on-chain CDP to achieve a 100% CR); the difference now rests on the assets backing it and the move towards 100%+ of collateral.

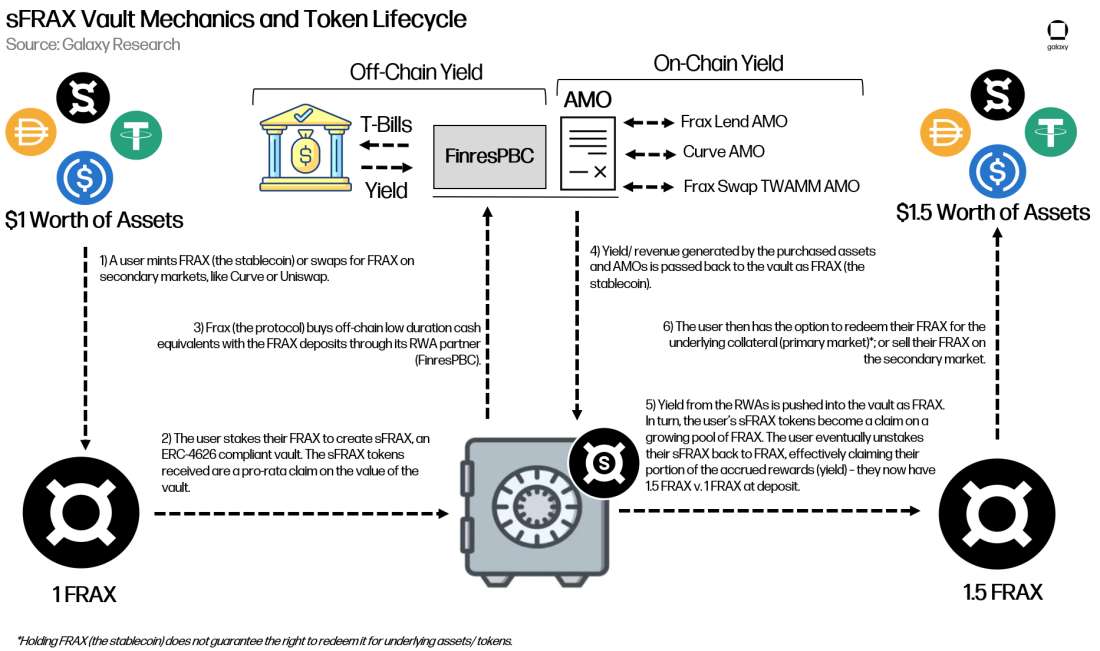

sFRAX Vault Mechanics

Like Maker’s DSR vault, the sFRAX vault is an ERC 4626 smart contract that distributes yield originating from off-chain RWAs to users staking the FRAX stablecoin. Frax Finance aims to keep the sFRAX vault APY close to (but does not guarantee absolute reflection of) the off-chain IORB rate with as little duration risk as possible. sFRAX deposits are used to purchase the following types of RWAs, all of which have been approved through frxGov, the Frax Finance governance process:

Short-dated United States Treasuries

Federal Reserve Overnight Repurchase Agreements

USD deposited at Federal Reserve Bank master accounts

Select shares of money market mutual funds

FinresPBC, in a partnership with Lead Bank, is the custodian partner of Frax Finance that aids in the process of acquiring and disposing of these assets. Per the governance proposal onboarding FinresPBC, the conduit’s “public mission is to provide the Frax Protocol access to safe cash-equivalent assets and near Fed rate yields for the benefit of all without seeking to make profit from this relationship or charge fees (other than to pay for minimum costs related to serving its mission).”

Every Wednesday at 11:59:59 UTC, the Frax protocol mints new FRAX to the sFRAX vault proportional to its earnings from yield generated by RWA collateral. The sFRAX vault APY is based on a utilization function (sFRAX Staked / Total FRAX Supply) and a cap rate (maximum rate) determined by frxGOV. The cap rate is also dependent on the IORB rate. The vault APY declines towards the IORB rate (bottom or target rate) when the total share of FRAX supply staked increases; and climbs towards the cap rate when the share of FRAX in the sFRAX vault decreases. Thus, sFRAX yield has a top end target determined by a function of frxGOV and the IORB rate APY and theoretically has no bottom as the IORB rate can turn negative. The yield earned from RWAs is also supplemented by onchain yield from Frax AMOs.

The mechanics and lifecycle of sFRAX are visualized in the image below. Note, the yield depicted is hypothetical for the purpose of visualizing the sFRAX staking process.

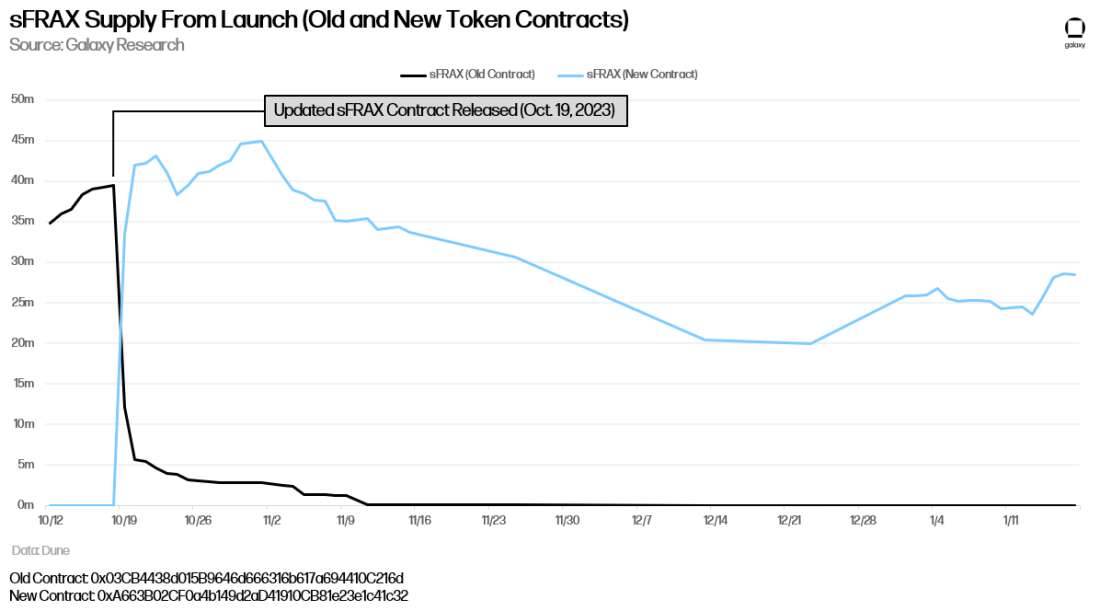

The supply of sFRAX reached as much as 44.96m units but is down to around 28.5m sFRAX as of January 17, 2024 (-36.6% from high). The slow growth is due to one primary factor: the rates achievable through onchain channels have been strongly contesting that of offchain rates (such as the IORB rate). This notion manifests itself in a couple ways, with users directly capitalizing on stablecoin lending rates across applications like Fraxlend, Aave, and Compound; and users carrying out more complicated strategies tapping into ETH staking yields. In either case, demand for sFRAX and offchain yields are detracted.

On October 19, Frax Finance developers issued an update to the sFRAX token contract. The update introduced 3 key changes from the original contract:

Fixed punctuation of the name string from Staked Frax to Staked FRAX.

Added pricePerShare() function to the contract for easier integrations Curve pools and vault protocols (making Curve swaps cheaper than was achievable with the previous contract).

Minor gas improvements from updating contract language to Solidity 0.8.21 and other smart contract optimizations.

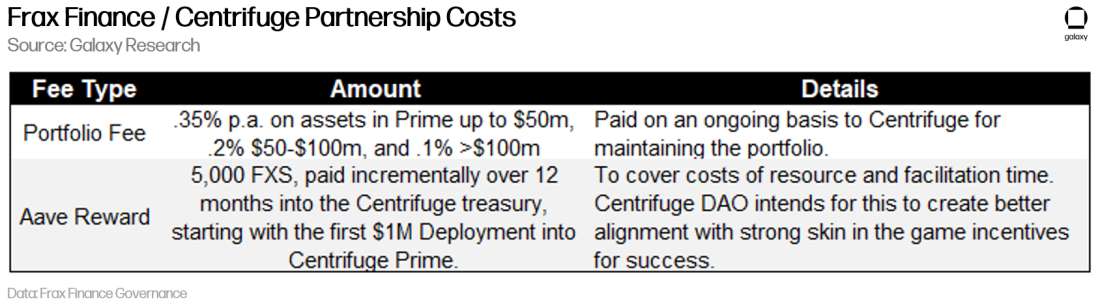

In addition to the dynamic RWA strategy introduced through the sFRAX vault, Frax governance voted in favor of leaning on Centrifuge Prime to move $20m of FRAX collateral to the Anemoy Liquid Treasury Fund. The passing of this vote enables Frax to replace a portion of its existing stablecoin collateral with T-Bills, and carries the following costs:

Frax Bond Tokens

Frax Bond tokens (FXBs) are flexible utility tokens that resemble zero-coupon bonds with a predefined maturity timestamp. FXBs effectively allow users to purchase FRAX at a discount to its $1 peg today and redeem them for the full $1 value at a future date. Frax Finance can use the proceeds generated by users bidding on FXBs to support protocol operations or enact strategies that generate the yield that will be delivered to FXB holders upon maturity (such as acquiring off-chain assets that match the durations of auctioned FXBs). The zero-coupon nature of FXBs means users do not receive periodic yield payments. Instead, the fixed yield is realized upon maturity. FXBs mature at the end of the day of their maturity date in UTC and have no expiration. For example, FXBs can be burned back for their corresponding FRAX prior to their maturity date. FXBs are a liability to Frax Finance, as they are a future promise on user proceeds.

FXB tokens, in contrast to sFRAX, are not associated with or redeemable for RWAs or any other on-chain or off-chain assets. FXBs also play no role in supporting the FRAX peg - they are only redeemable for FRAX tokens on a one-to-one basis at the predefined maturity date.

According to Frax’s documentation, "FXBs allow the formation of a yield curve to price the time value of lending FRAX back to the protocol itself," effectively setting a benchmark yield for, and in turn cost to borrow, FRAX across longer durations in accordance with their maturities. The benchmark rate isn’t necessarily indicative of the actual rate which is driven by the market.

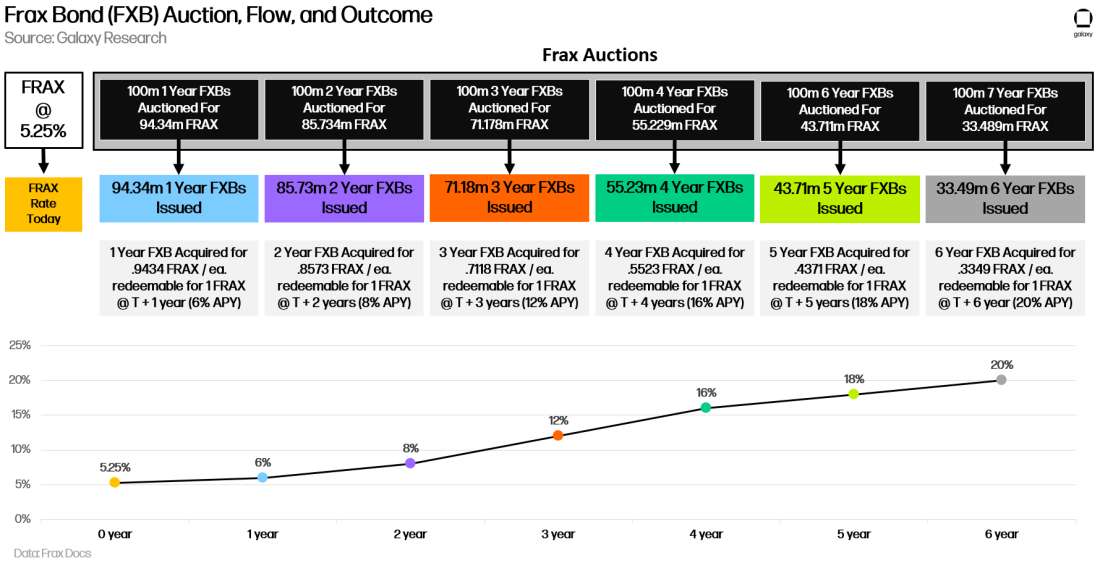

Price discovery for FXB tokens occurs through a gradual Dutch auction system that ensures FXB tokens are not sold for prices lower than the floor limit. A gradual Dutch auction system is a variation of the traditional Dutch auction method, tailored to allow for a more measured and controlled sale process. In a Dutch auction, the auctioneer starts with a high asking price, which is lowered until a participant accepts the price. This method is commonly used for selling items quickly, often in financial markets or for perishable goods. Gradual Dutch auctions allow for more controlled price reductions, give the market more time to respond and assess the auction, in turn allowing for better price discovery by giving the market more time to digest the auction, and grant more flexibility to buyers than traditional Dutch auctions. In a gradual Dutch auction, the price reduction occurs at a predetermined rate over a set period.

The following graphic visualizes the process by which FXBs are auctioned and the yield curve they create. The values associated (i.e. FXB auction values, durations, and yields) with the graphic are hypothetical and used for demonstrative purposes. In practice, they are determined by the market and frxGov.

As mentioned, FXBs can be used to raise funds that support Frax Finance in any capacity. For example, they can be used to assist the off-chain to on-chain RWA procedures of the protocol. The RWAs incorporated by Frax can carry T+1 settlement cycle, or in some cases T+2 or more, meaning it can take 1 to 2 days or more to settle the sale of the RWAs, get stablecoins in return, and fulfill the redemption of assets on-chain. Even though the value exists, the time duration mismatch can cause protocol instability. FXBs offsets this risk by allowing Frax Finance to raise liquidity through FXBs and fulfill on-chain redemptions more quickly.

Frax’s FXB module went live on January 19, 2024. It launched with three FXB auctions, each holding an expiration date of January 24, 2024 at 23:59:59 UTC across maturities of June 30, 2024, December 31, 2024, and December 31, 2026. New sets of auctions went live on January 23, 2024, holding the same maturities as the initial set launched on January 19. The current auctions expire on January 30, 2024 at 23:59:59 UTC.

FXB pools are also live on Curve, allowing users to swap between FXBs and the FRAX stablecoin; or supply their FXBs for yield. Additionally, Curve’s isolated lending pools that are currently under audit will allow users to mint crvUSD with FXB collateral. This brings a unique use case to FXBs, giving users the ability to deploy their bonds as they wait for them to mature. It also gives crvUSD an outlet to be collateralized by stable, yield-bearing onchain native assets.

Through the combination of sFRAX, FXBs, and the revamped approach to FRAX’s collateral strategy, Frax Finance introduces a unique on-chain and off-chain yield model that relies on RWAs, crypto-native assets, and a new type of utility token that functions like traditional zero-coupon bonds. Frax Finance’s v3 upgrade offers a unique approach for DeFi protocols to seek to improve the stability of their stablecoins and reduce the cyclicality of on-chain yields by taking advantage of the inverse relationship in demand between crypto-native assets and traditional safe haven assets.

Aave

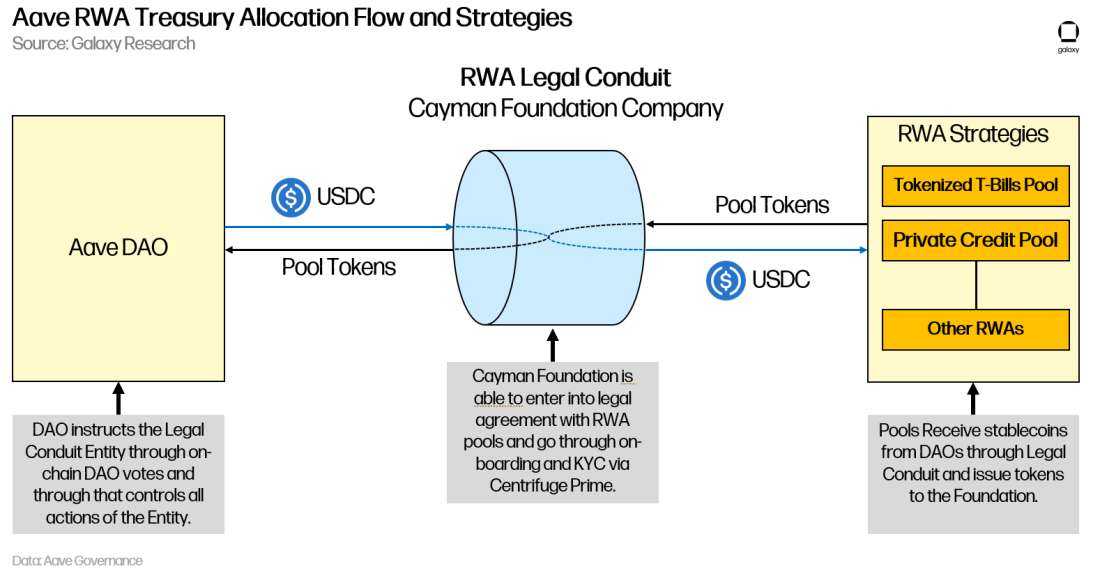

Unlike MakerDAO and Frax Finance, Aave is not actively using RWAs to support its products or services. Instead the protocol plans on deploying $1 million in stagnant capital from its treasury into RWA strategies, such as T-bill vaults. In September 2023, AAVE token holders voted in favor of acquiring RWAs through a strategic partnership with Centrifuge Prime, a company that provides the infrastructure needed for protocols and on-chain native entities to gain RWA exposure.

The process by which the Aave DAO plans on gaining exposure to off-chain yields through its proof-of-concept RWA investment is visualized in the image below (Frax Finance will leverage a similar conduit in its RWA collaboration with Centrifuge Prime):

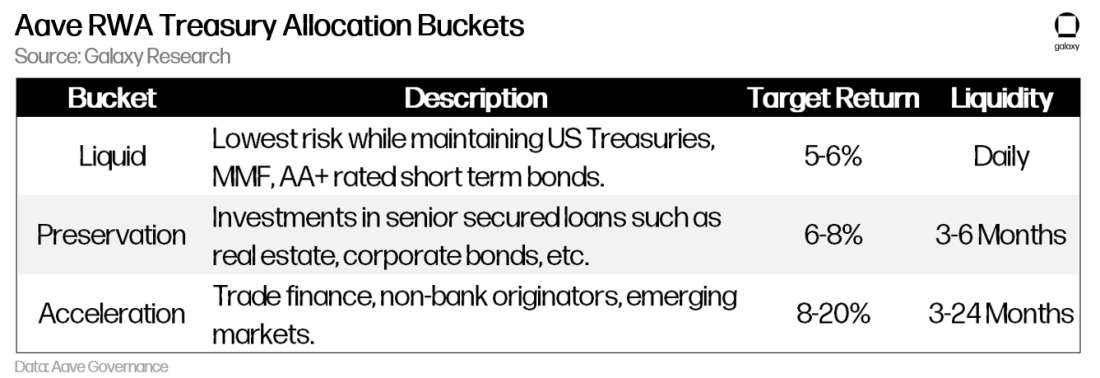

The proof-of-concept investment outlined in the governance proposal passed in September 2023 exclusively gains exposure to liquid T-Bills through Centrifuges Anemoy Liquid Treasury Fund. However, there are additional assets the strategic partnership with Centrifuge Prime can allow for. The other buckets and specifications of RWAs Centrifuge Prime permits Aave to allocate its treasury to include:

It is estimated that the process of setting up the legal conduit and deploying the funds through Centrifuge will take at least 3 months from the vote passing. This lands the deployment date around at least mid-December 2023. Draft legal docs for the structure of the DAO’s RWA strategy were shared in October 2023 [1] [2]. There have been no updates posted in the Aave Governance Forum since then.

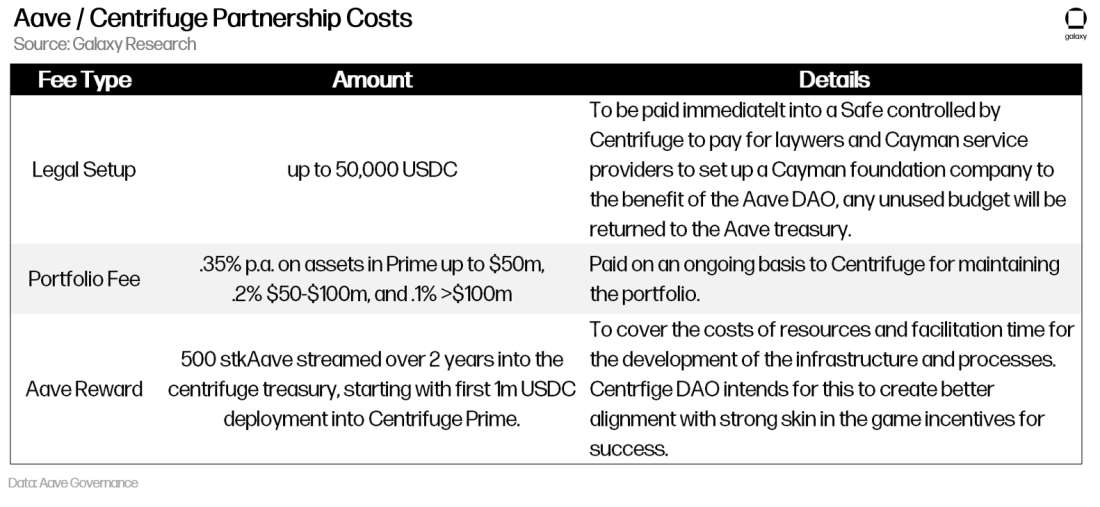

Additional start up details and costs of the partnership include:

There has also been discussions [1] [2] on backing the protocol’s stablecoin, GHO, with RWAs. Per a Q&A forum in Aave Governance, however, GHO Facilitators are not yet ready to allocate to RWAs and there is no tangible timeline for when to expect their implementation. As background, GHO Facilitators are responsible for the trustless burning and minting of GHO tokens. Each Facilitator has a designated strategy and ceiling amount it can mint to create tokens, which allows GHO to be minted and destroyed through a number of different mechanisms. As of November 2023, the two facilitators that are active include:

The Aave v3 Facilitator: GHO can be minted through debt positions and burned via repayments on Aave v3 loans.

FlashMinter: The minting and burning of GHO through FlashMinting is similar in nature to flash loans, whereby users borrow assets, deploy them, and pay the debt back in a single transaction. The FlashMinter facilitator works the same way, but instead of borrowing assets from an Aave pool, users mint GHO, deploy it, and pay it back (burn it) all in one transaction.

Additionally, on October 20, 2023 Singapore-based RWA project, DigiFT, submitted a temperature check on a proposal to include its US Treasury token, $DUST, in Aave’s protocol treasury strategy. It also outlined ways to use their RWA token as collateral for GHO. In the same month, TokenLogic, a company comprised of active Aave community members, proposed the addition of rETH, a liquid staking token, to the DAO’s treasury to achieve a similar revenue generating opportunity as with treasury funds. The snapshot vote for this proposal passed on October 23 with a 99.99% majority.

For now, Aave is using RWAs to generate revenue with unproductive, idle resources owned by the DAO. This is a simple RWA strategy, but it benefits the protocol and users by generating higher protocol revenues that can then be used to fund protocol development. In the future, Aave may collateralize its stablecoin in a similar fashion to MakerDAO and Frax Finance with RWAs.

Outlook

RWAs have the potential to improve crypto-native DeFi protocols, products, and services (albeit with the risks noted). The benefits of integrating RWAs in DeFi are already being capitalized by major DeFi protocols including MakerDAO, Frax Finance, and Aave.

The utility of RWAs in DeFi apps will be a key component for the growth, scalability, and impact of RWAs as a whole on public blockchains. Though overreliance on RWAs for protocol yield and stability is a danger, the integration of RWAs on-chain can create synergies that benefit DeFi protocols and end users. Taking this into consideration, the future of RWAs and their utility is on public blockchains where these types of assets can be integrated with existing on-chain liquidity, infrastructure, and crypto-native communities, not gated and permissioned networks and protocols. However, it is inevitable that the tokenization of RWAs more broadly will bleed into sandboxed environments as issuers experiment with their capabilities and use blockchain as a technology to satisfy their individual needs. Nonetheless, as adoption of RWAs grows and token development/ composability improves, more DeFi protocols are likely to open themselves up to accepting RWA tokens from end-users to fulfill utility such as issuing stablecoins and acquiring leverage.

Rather than replacing or becoming an alternative industry to the existing DeFi space, RWAs should be viewed by users and builders as an outlet to mature and progress DeFi and, more broadly, further the crypto industry’s mission to reshape traditional finance.

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsement of any of the stablecoins mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned, hedged and sold or may own, hedge and sell investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2024. All rights reserved.