This is the second part of a three part series originally published in 2019. Read part 1, On Sound Money, here. Read part 3, On Incentives & Scarcity, here.

Abstract

Current monetary standards have been relatively monopolistic and have caused significant wealth erosion of its holders through inflationary policies. However, the crypto asset innovations of the past decade have enabled a free market determination of the best forms of money for its users. A competitive market for money would lead to a free market determination of monetary standards and place natural disciplines on issuers to maintain the soundness of their money.

The Market for Monetary Standards

Similar to any good, service, or form of labor, monetary standards exist in a market, a process by which the price of money for goods and services is established. The market for monetary standards facilitates competition among competing forms of money, and the economic agents responsible for maintaining the monetary standard seek to obtain a share of a finite market chasing scarce resources. Effective usage of monetary standards enables trade and the distribution and resource allocation in societies. The market for monetary standards can emerge spontaneously or deliberately through human interactions in order to enable the exchange of ownership of services and goods.

Monetary standard markets have ranged from free markets, where the best forms of money competed and accurately signal costs and benefits, to monopolies, where monetary standards are controlled by a central agent. Some examples of “free money markets” include barter/commodity economies, free specie markets like early Mesopotamia and the Mongol empire, and even late 1800s America. In general, the common denominator for more competitive money markets have been fairly liberalized economic and political policies. In contrast, most monetary standard markets historically have existed as near monopolies in bounded economies. Whether it was an explicit government diktat or requirements for taxes due to be paid in a chosen media, monopolistic or oligopolistic conditions for monetary markets have persisted for the most part.

The history of money is well documented by many historians, particularly the monopolistic dynamics and externalities of government-issued money. Over the past two thousand years, the monopoly (whether natural or government dictated) of government-issued money has deprived societies and economies from discovering the best forms of money through natural, free market processes. In nearly every instance of monopolistic government-issued money, governments with the ability to fully control issued money have resulted in rapid stock increases and the wealth depreciation of its holders, leading in many instances to economic collapses.

Prior to Bitcoin, the modern market for monetary standards had been monopolistic (or oligopolistic if one were to include other G20 currencies) and monetary standards were extremely similar to one another, sharing similar policies and control by centralized governments. The creation of Bitcoin and the innovations over the past decade have created an experimental testing ground for creating new forms of value and money. In our view, we believe that Pandora’s box has been opened and natively digital currencies and forms of value (whether created as crypto assets or by private corporations) have borne an emerging market for monetary standards. While it is premature to say that we have a free market for money just yet, the US dollar’s position as the global reserve currency is experiencing heightened competition from foreign sovereigns, crypto assets, and private corporate-issued money.

In competitive markets, open competition leads to innovation and product development, providing consumers with a wider selection and better products that serve the needs and wants of its users. In a competitive market for money, monetary standards would compete and lead to the best forms of money for its users. The requisite elements of money become the key points of competition and differentiation, leading to a free market determination of society’s monetary standard.

Monetary Market Competition

There are three widely considered requirements for money: unit of account (ability to specifically measure value), medium of exchange (can be exchanged for good and service as an instrument and avoids the limitations of barter), store of value (ability to retain and exchange value at a future point in time). If a media satisfies these three elements, it can be considered as a form of money and does not need to be limited to what is more colloquially considered “money.” Through this more macro lens, we can see that the categorization of money can extend beyond government-issued currencies, and include crypto assets designed to be money (whether they exist today or are new market entrants), new corporate-issued forms of money, and even digitized traditional assets that, due its newfound digitization and transferability, can be used to transfer value and pay for goods, services, and labor. If asset X can act as a unit of account, retain its value over time, and avoids the limitations of a barter system through market discovery of its price, it should be able to be used as money.

The first two requirements of money are no doubt critical, and hinge upon the ability for economic goods to be measured in discrete units of the media and for the media to have some sort of economic value in the present, a measurement of an asset’s direct or indirect utility. Money has value because society demands the indirect benefit it offers in purchasing power for goods and services. Because society is willing to accept and give money as forms of payment, its value is derived more so from a social convention as opposed to a government mandate. Money has ascribed value ultimately because of supply limitations and resource scarcity. If money was available in unlimited supply, it would be effectively free. Non-zero prices serve as a rationing mechanism whereby consumption is limited to the available supply.

We will focus our discussion on the 3rd requirement of money: store of value, perhaps the hardest requirement for money to achieve and retain. The focal determinant of money’s ability to retain value is 1) high stock to flow ratios (thereby preventing the rapid increase in stock and loss of salability) and 2) lasting social conventions to accept the money. Government-issued money has historically been susceptible to losses in value, as the effectively zero cost of production and printing of unsound money to finance national spending creates a vicious cycle of borrowing from the future to satisfy the needs of the present and alarming devaluation of money. This phenomenon of irresponsible money stock management persists because there are no currently imposed disciplines on government issuers to control the quantity of money in an appropriate manner. The lack of monetary standard competition prevents the market determination of these natural disciplines, and furthermore changes the primary goal of an issuer from providing its citizens with good money to creating a system by which a government can tap into a money supply by owning its manufacturing process.

It is particularly peculiar that fiscally irresponsible governments exist in capitalist economies — capitalist economic participants such as corporations are required by the market to remain fiscally responsible to maintain and grow the value of their currency (i.e. their “stock”) through long-term growth, driven by responsible capital investment, the extension of the production cycle, and increased productivity. Natural market forces also place determinants on how a corporation manages its currency, preventing a company from grossly diluting current holders of their currency with market checks and balances. It becomes quite apparent that the stocks of many corporations could actually serve as better forms of money than many of the government-issued fiat currencies.

Monetary Policy

Monetary policy’s impact and influence is unquestionably an important element in modern economies. Policymakers seek to achieve inflation, growth, interest rate, and employment objectives. Central banks use various tools, including open market operations, lending to banks, and bank reserve requirements, to achieve these objectives. It can be used in conjunction or as an alternative to fiscal policy, which federal governments use to manage the economy through a combination of taxes, government borrowing, and federal spending. Using its levers, central banks play a critical role in managing the rates of inflation, growth, and unemployment by increasing or decreasing the money supply and changing consumption and spending propensities through interest rate manipulation.

Productivity is a critical factor in the long-term wealth and health of societies. Improvements in economic productivity over time (increased aggregate outputs for the same aggregate inputs) causes a relative decrease in broad price levels if the money supply remains constant: if the amount of goods produced in an economy are doubled but the amount of money stays the same, the cost of the goods are halved. Increases in economic productivity generally lead to increases in nominal labor income, as some of the profits generated by businesses flow to its labor. The relative changes in productivity and nominal labor income affect the ultimate inflation in an economy: if wage inflation is higher than productivity (holding consumption propensity and savings rate constant), there is “more money chasing fewer goods” and hence overall price inflation (the rise in the nominal cost of goods). Conversely, if productivity is higher than wage inflation, the cost of goods in an economy falls, or creates deflation.

Central banks play a deeply influential role in managing these dynamics of price level changes. It would stand to reason that with such influence, there should be express or market-driven disciplines that enforce a policymaker’s fiscal responsibility with how a nation’s money supply is managed to promote price stability, enduring purchasing power, and long-term prosperity. Yet, quantitative evidence shows the severe longer-term consequences of monopolistic control and the printing of money when gone unchecked. In particular, the US dollar has emerged as the primary reserve currency of the world over the last two hundred years. However, using core CPI inflation figures, the US dollar has lost 96% of its purchasing power over the century. In the aftermath of the 2008 Global Financial Crisis, the USD M2 money stock doubled to $17t leading to a 16% decline in the USD’s purchasing power and a 31% increase in the US’ debt-to-GDP ratio in just ten years.

Inflation & Purchasing Power

While these data points may seem alarming, many have argued that developed market inflation has been relatively low in the last decade, on average sitting below the 2% stated inflation target by policymakers. Monetary printing simply has not surfaced into inflation. Some policymakers have even expressly stated that the phenomenon of low inflation despite the aggressive monetary stimulus has left them confused. In part, increased globalization and automation have led to a weakening of domestic firms’ pricing power and the passing along of rising costs into wages and ultimately goods’ prices. Furthermore, there are a multitude of innovations that are not captured in inflation measures that have improved the aggregate quality life for the average citizen; the basket itself and hedonic quality adjustments in CPI do not capture these innovations and could even suggest there has been price deflation in goods. (1)

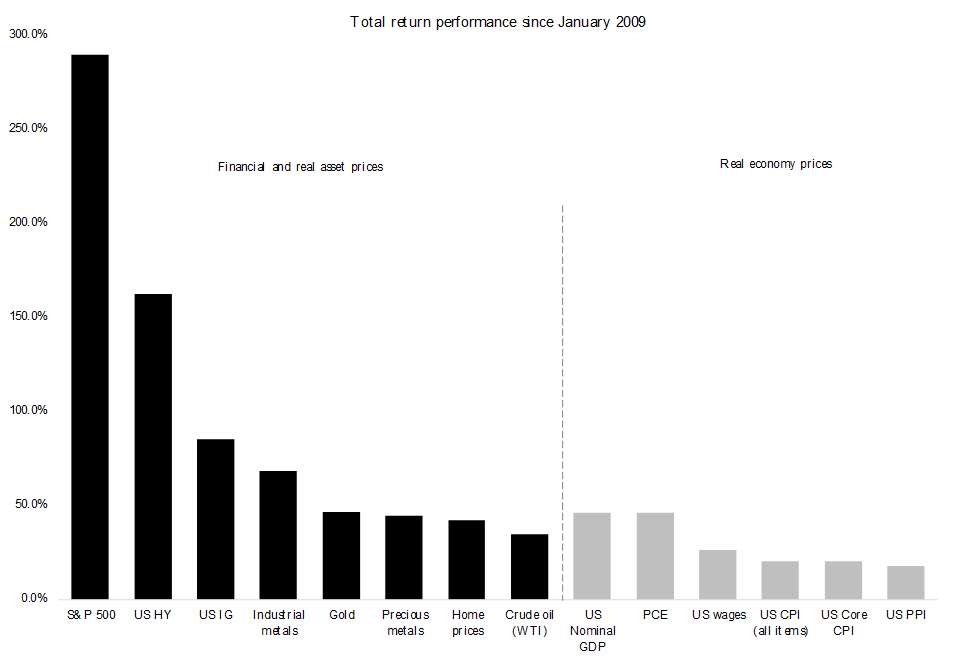

However, the historical inflexible dependence on traditional inflation metrics severely understate the broader pricing dynamics that have occurred in the past ten years. Consumption and goods are just one outlet for monetary stimulus. The capital flow dynamics into other ultimate outlets of the newly minted money paints an inflation reality that is actually far worse than many imagine: real and financial asset inflation have grown substantially and have been the primary beneficiaries of the Fed’s stimulus (see Figure 1). Overall inflation of goods and assets, when adjusted for these monetary outlets, is far higher than the reported sub-2% inflation.

Fig. 1: Total return performance, financial & real asset inflation versus real economy inflation. (2)

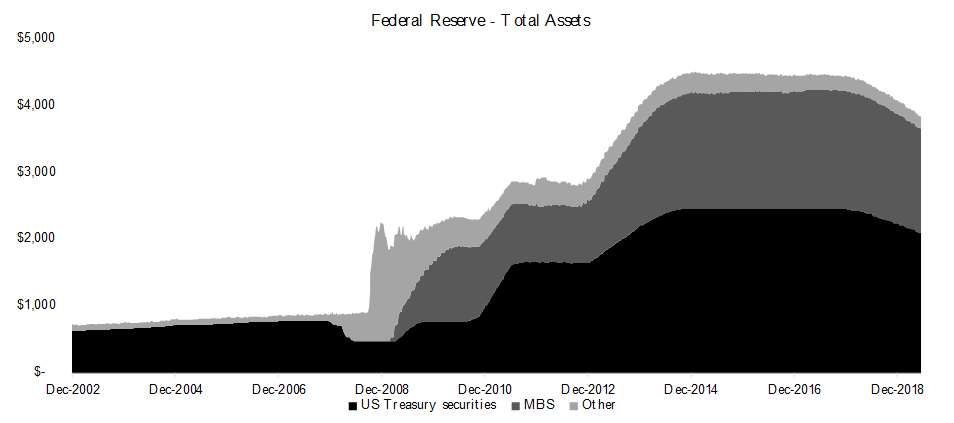

Real and financial asset inflation is a predictable phenomenon of monetary stimulus given the mechanics of monetary open market operations and flow of capital. While the Treasury is responsible for printing paper currency and minted coin, the Fed can “print” money by extending credit to banks and charging an appropriate interest rate. The Fed also purchases Treasury notes and mortgage-backed securities from banks and adds credit to the banks’ reserves. Since 2008, the size of the Federal Reserve’s balance sheet has grown substantially; open market operations have led to a 4x increase in the Fed’s balance sheet from $1t to roughly $4t (see Figure 2).

Fig. 2: Total assets, Fed's balance sheet. (3)

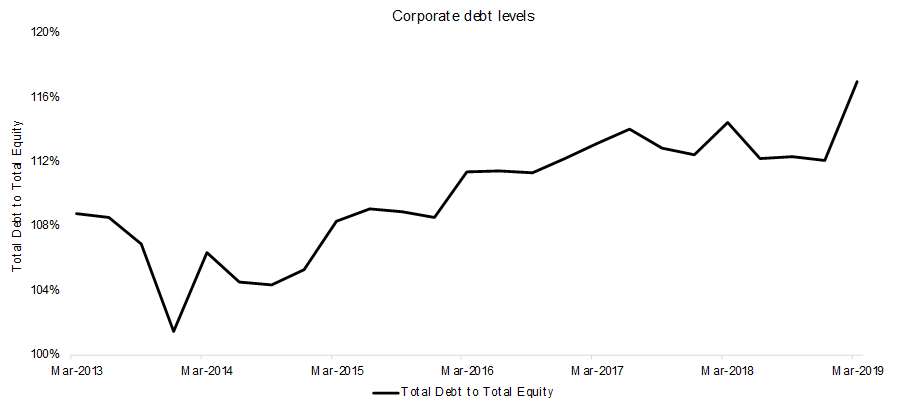

The Fed can also tweak bank reserve requirements and the overnight Federal funds rate, thereby influencing credit extension and its cost in the market. Once banks receive credit from the Fed, they can turn to the market and lend it out to market participants. These market participants tend to be large corporate institutions, who in theory can use corporate loans and debt for increased investment and expansion. This dynamic can be viewed in historical balance sheet data: the total debt-to-equity ratio from the S&P 500 rose from 101% to 112% between December of 2013 to 2018 (see Figure 3). As of March 31, 2019, this ratio stood at 117%.

Fig. 3: Corporate debt levels. (4)

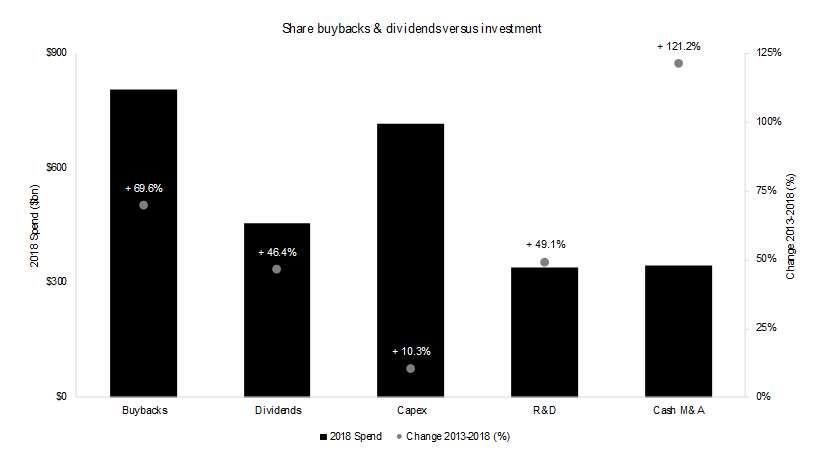

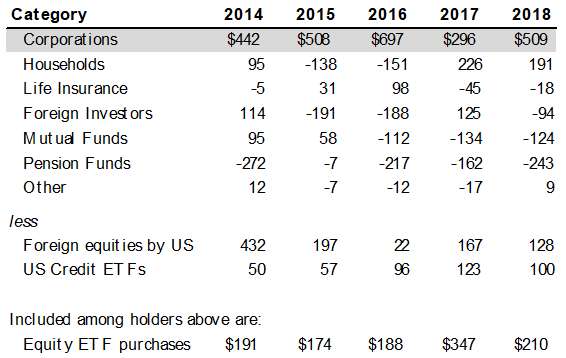

The increased debt levels of corporations, both on an absolute and relative basis, has led to significant increases in share buybacks and dividends relative to capital investment. Between 2013 and 2018, companies increased dividends and share buybacks from $787b to $1.26t, representing a 60% increase (see Figure 4). In comparison, total aggregate spending for capex, R&D, and cash M&A increased just 36% from $1.03t to $1.40t.

Fig. 4: S&P 500 cash spending. (5)

Conceptually, buybacks and dividends provide many benefits for shareholders and long-term economic productivity, releasing underutilized “trapped” capital from companies, prevents suboptimal capital investment, and putting capital toward more productive uses that drive growth, productivity, and innovation. While growth investment in aggregate accounts for a larger share of cash spending and growth investment has risen considerably in recent years, the accelerated share buybacks accounting for the single largest source of US equity demand over the past five years suggest that corporate buyback spending has resulted in elevated equity price levels. Considering this dynamic has occurred on the back of rising corporate debt levels spurred by easy and cheap liquidity from the Fed, we can see that a portion of the considerable monetary stimulus and printing has led to equity asset inflation. (6)

Table 1: Net US equity demand ($ billions) (7)

Competitive Markets for Money

The crypto asset innovations over the past decade have created an experimental sandbox for creating new forms of money. We break down these new types of money into three broad buckets:

Permissionless crypto asset money networks such as Bitcoin

Corporate or foundation-issued money and payments networks such as Facebook, Telegram, and fiat-backed stablecoin networks

Digitized (“tokenized”) traditional assets such as equities, real estate, LP interests, etc.

Permissionless crypto money. Permissionless digital assets that exhibit characteristics of sound money with high stock-to-flow ratios, sufficient network and cryptographic attack resistance, and inflation protection can serve as money. In our view, Bitcoin remains the market leader and will continue to grow its moat through its network effects, feature sets, first mover advantages, and social convention. However, we do see the possibility for other forms of permissionless money to take a smaller market share for more targeted use cases and applications, such as privacy-oriented money.

Corporate-issued money. The desire to transfer dollar-equivalents between exchanges and speculators during closed banking hours led to advent of fiat-backed “stablecoins.” Permissionless asset-backed money like Dai and other algorithmic soon followed with the intention to create a more useable money for everyday use, but have mostly struggled with monetary management issues and expanding beyond speculative use cases. Perhaps the first formidable movements into creating a generalized digital money has come from messenger-oriented companies like Facebook, Telegram, Signal, and even Samsung who are in various stages of development for creating a general crypto money. Since the actual architecture and degree of permission for these platforms is unknown by the general public, we categorize them as “corporate-issued money.” The wide user bases of these applications and deep relationships between the issuer and Fortune 1000 companies can potentially lead to widespread adoption and usage of digital money, competing with legacy payment methods and networks.

General digitized value. Perhaps the furthest from fruition and actual practicality, the move to create smart digital securities for both currently digitized securities like publicly traded equities and previously non-digitized assets like real estate and LP interests creates an interesting potential for new forms of value transfer. The digitization of traditional assets coupled with seamless financial markets creates an opportunity for the full monetization of one’s portfolio and wealth. Imagine for instance a retiree who wishes to pay for a dinner. Today, the retiree must have previously sold a small portion of their retirement portfolio, wait until the trade was settled, then transfer the cash to a primary bank account. Along the way, the brokerage, market makers, payment networks, and banks all take economic rents as intermediaries. In a world in which one’s portfolio is fully digitized and the market infrastructure has evolved, the retiree can instead pay for the dinner using a small fraction of their portfolio (say a share of Apple or a fraction of an LP interest), remitting the due balance as a fraction of a traditional asset which is met with an automatic selling and settlement by the recipient. While there are many barriers associated with such a system (requires a common-denominated value to avoid barter limitations, selection of which shares to sell, and hyper-efficient market and payment infrastructure), there is certainly an interesting potential for financial assets with enduring value into edge case money.

Competitive Forces & Darwinism

The proliferation of monopolistically managed money has deprived users with the ability to find the best money (or monies), despite the lack of evidence that government issuers can responsibly and effectively manage the money supply in the long run. As Nobel Prize winning economist F.A. Hayek explains, “There is no justification in history for the existing position of a government monopoly of issuing money. It has never been proposed on the ground that government will give us better money than anybody else could.” (8)

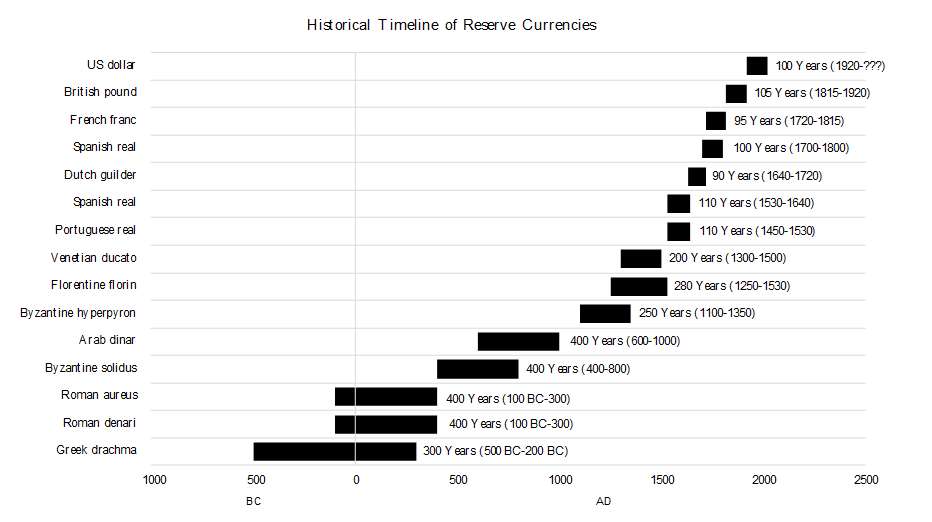

The history of civilization and dead money suggests that despite attempts by empires and imperial powers to maintain lasting political and economic influence, weakened money backed by fragile empires eventually succumb to Darwinian dynamics and are replaced by money with stronger monetary characteristics (Figure 5).

Fig. 5: Historical timeline of reserve currencies, estimates, various sources

A transition from a monopolistic to competitive market does not spell ruin for the US dollar; in fact, it provides the central bank with the opportunity to return the US dollar to a state of “soundness” and make the currency more competitive in an open field of competitors. Market competition for monetary standards would not only open the market to new entrants and innovation, but also force current issuers to remain disciplined with how they manage their money supply, remaining ever-vigilant on maintaining the soundness of its money and providing the best form of money for its users. Rather than establish the default currency by royal or government decrees, monetary standards can exist in an open, competitive market, lead to a free market determination of our monetary standards, and improve monetary standard optionality for the global citizen.

Citations

(1) The hedonic quality adjustments in CPI do not include many of the innovations and goods present in the 21st century, particularly digital goods and services. https://www.bls.gov/cpi/quality-adjustment/home.htm

(2) Bloomberg, Federal Reserve Bank of St. Louis, Economic Research, June 2019. Selected indices: S&P 500 Total Return, iBoxx High Yield Total Return Index, iBoxx Investment Grade Total Return Index, S&P CoreLogic Case-Shiller 20-City Composite Home Price Index, S&P GSCI Total Return Index, S&P GSCI Precious Metal Index, S&P GSCI Industrial Metal Index.

(3) Source: Federal Reserve Bank of St. Louis, Economic Research, June 2019.

(4) Bloomberg, S&P, June 2019.

(5) S&P, Goldman Sachs Global Investment Research, Compustat, June 2019.

(6) Goldman Sachs Global Investment Research, https://www.goldmansachs.com/insights/pages/top-of-mind/buyback-realities/report.pdf.

(7) Goldman Sachs Global Investment Research, Federal Reserve Board, June 2019.

(8) F.A. Hayek, Denationalization of Money, 2nd edition (London: Institute of Economic Affairs, 1978 [1974]), p. 7.

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2019. All rights reserved.