Crypto & Blockchain Venture Capital - Q1 2023

This report utilizes data from Pitchbook. Data on venture deals is often reported on a lag and thus the Q1 2023 data is subject to revision by Galaxy Research in future reports.

Key Takeaways

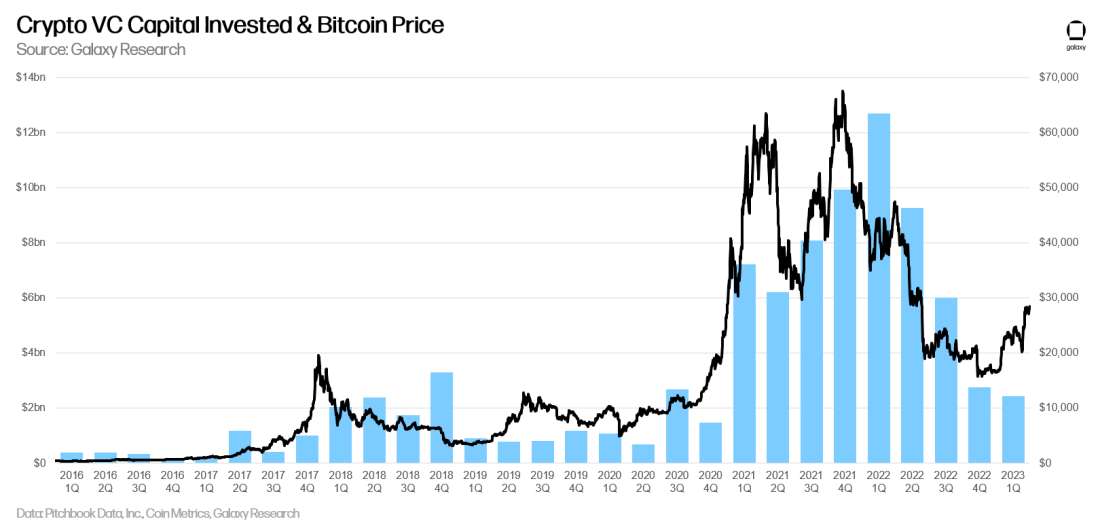

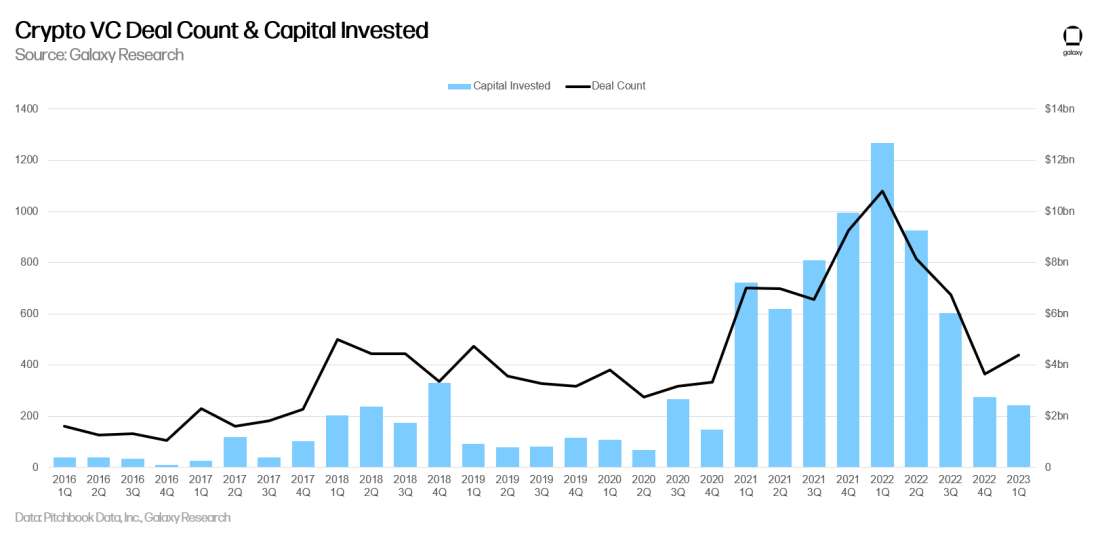

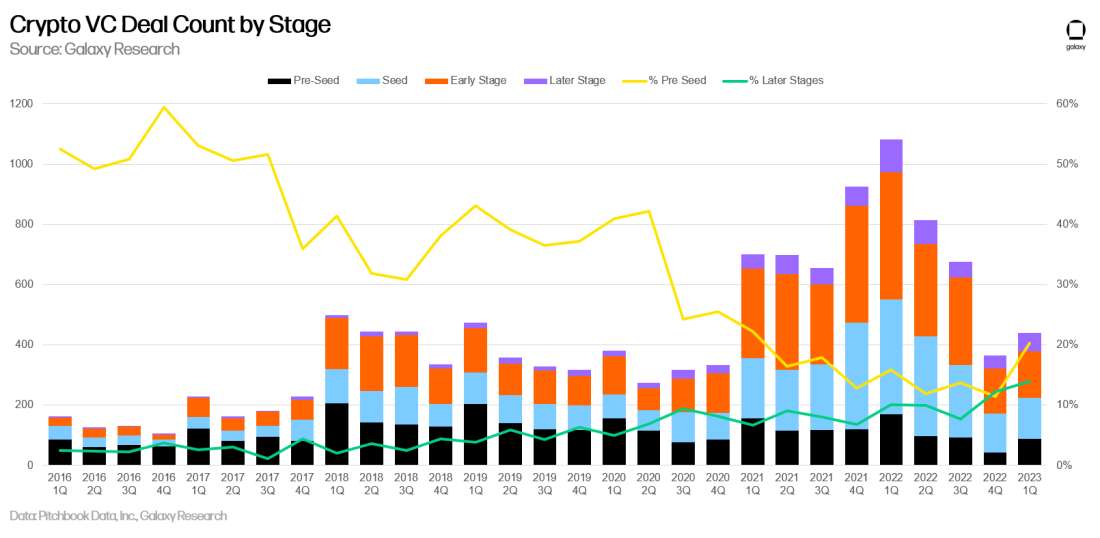

Venture capitalists invested $2.4bn into crypto-focused startups and protocols in the first quarter of 2023, the lowest sum in over 2 years (since Q4 2020). Deal count was up from Q4 2022 at 439 (vs. 366 in the prior quarter), with growth in pre-seed deals driving most of the gains (20% of the deals, the largest share since Q1 2021).

Median deal size continues to decline ($2.5m) from the all-time highs seen in Q3 2022 ($4.5m) and median pre-money valuation was $18.8m, its lowest point since Q1 2022.

Companies building in the Web3, NFTs, DAOs, Metaverse, and Gaming subsector raised the most deals (116), while Trading, Exchange, Investing, and Lending companies raised the most capital ($538m).

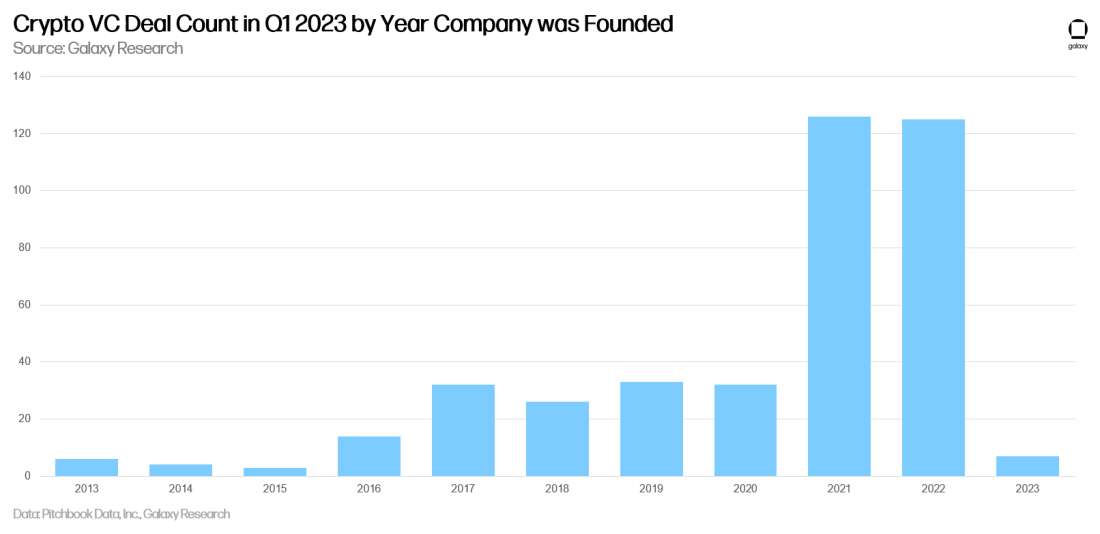

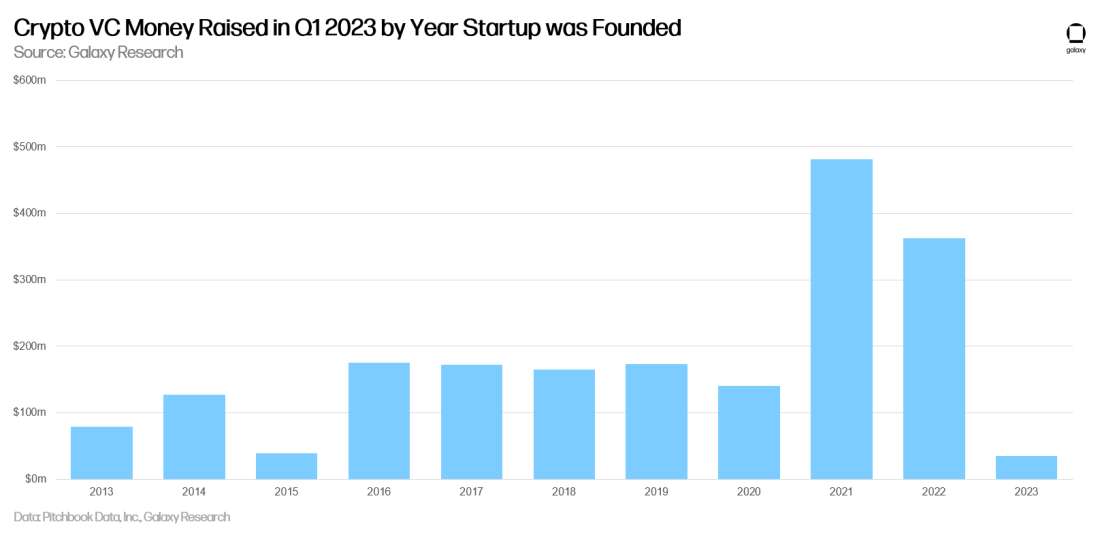

Companies founded in 2021 raised the most capital in Q1 2023 ($481m), but startups founded in 2022 were close behind ($363m).

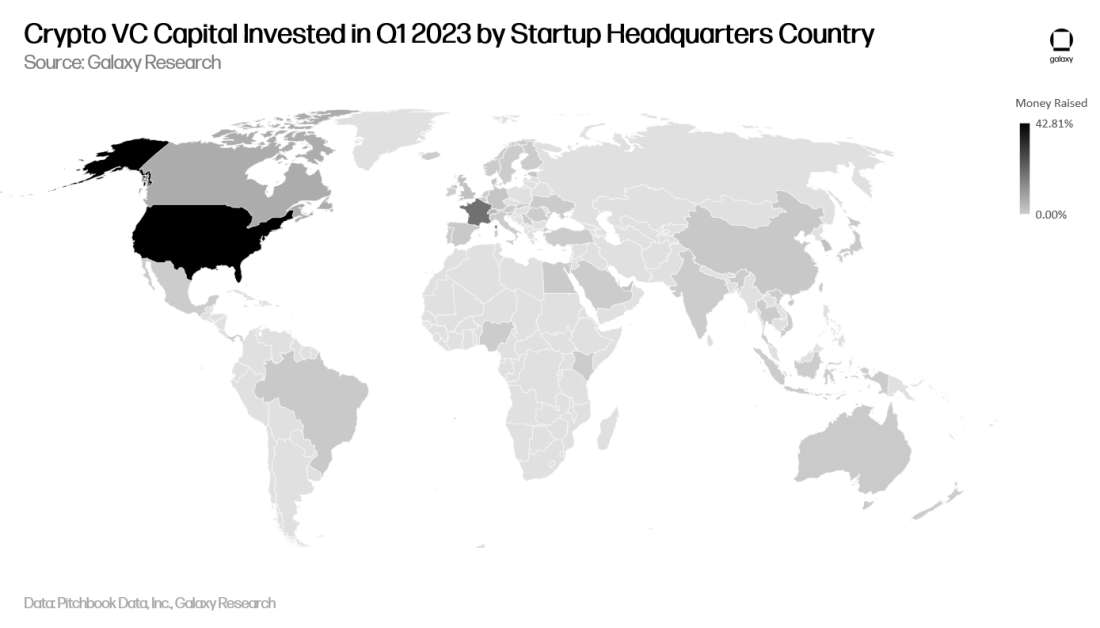

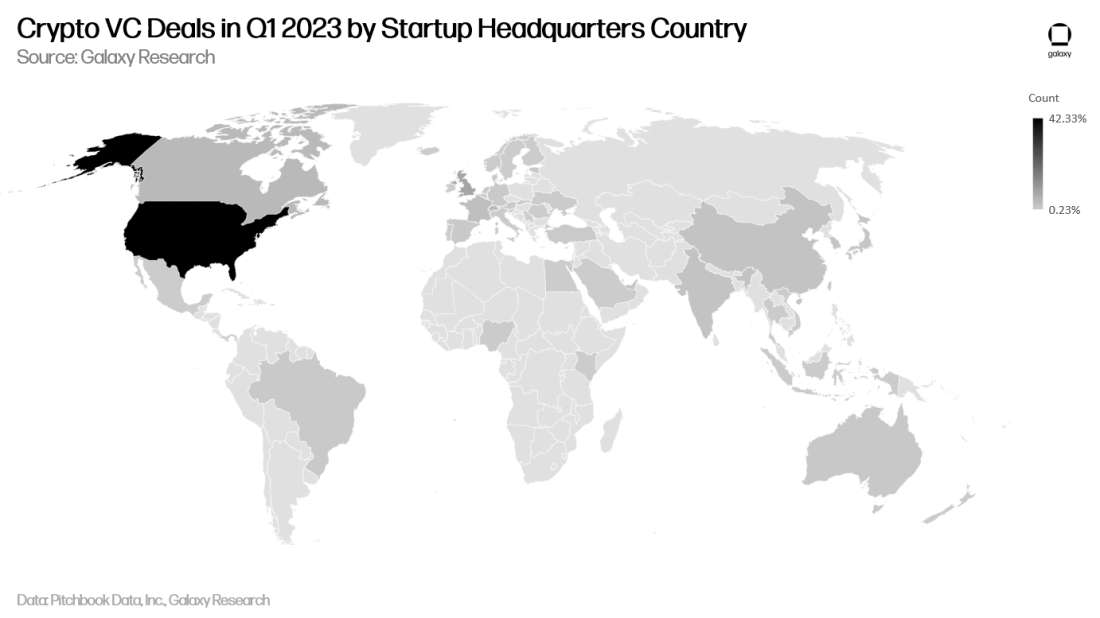

42% of crypto VC deals completed in Q1 2023 funded companies whose headquarters is in the United States (185 deals). Startups headquartered in the United Kingdom were second with 37 deals done in Q1 2023. US-based companies dominated capital raised with 42%, while France was second with 19%.

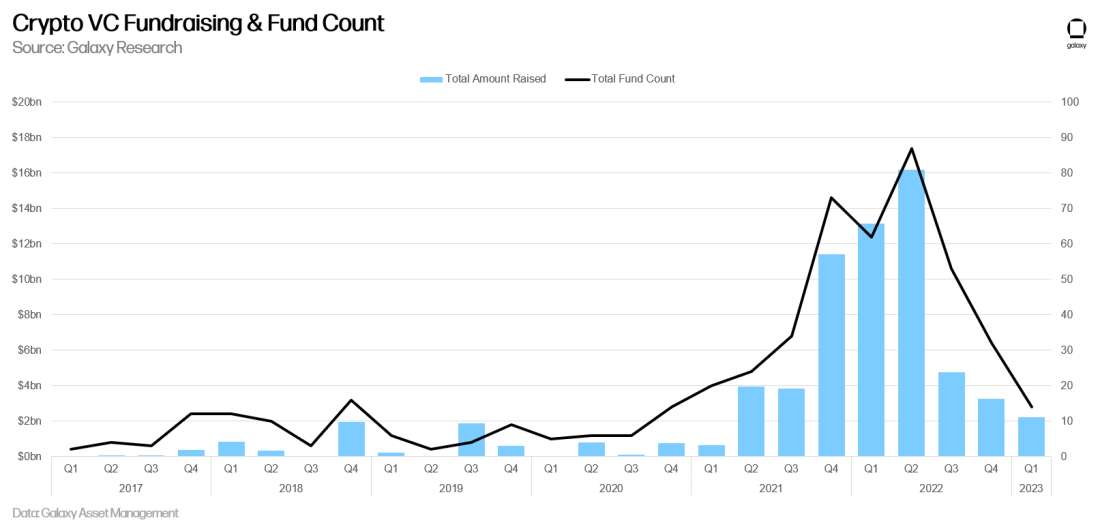

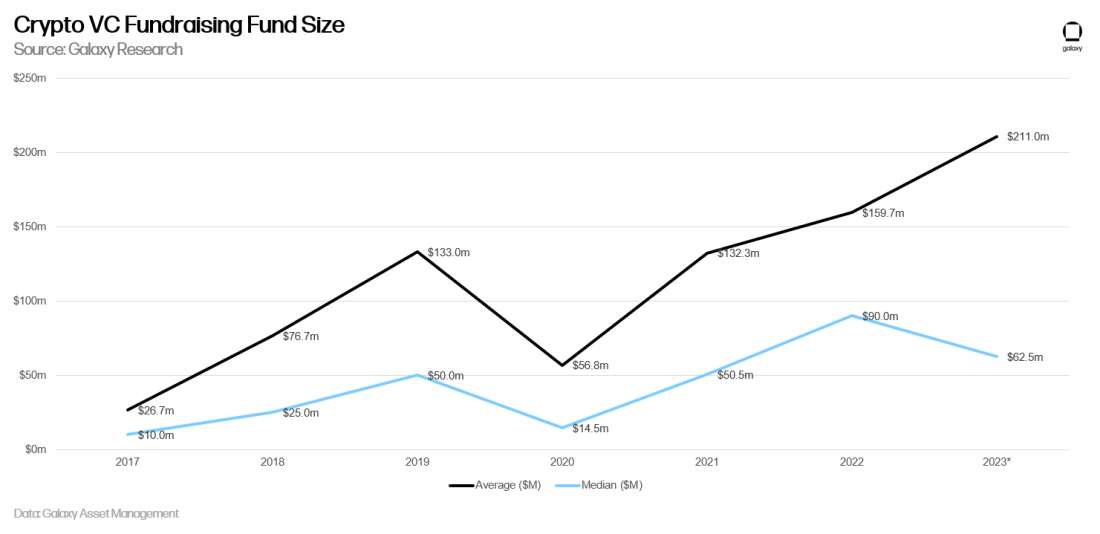

About $2.2bn was raised by 14 new crypto VC funds in Q1 2023, with average fund size increasing to $211m and median fund size decreasing to $62.5m.

Crypto VC Investing

Deal Count & Capital Invested

The crypto and blockchain sector saw $2.4bn invested in Q1 2023, the lowest amount since Q4 2020, continuing a downward trend that begin after a peak of $13bn one year ago. In Q1 2023, crypto and blockchain startups raised less than half the amount raised just two quarters ago.

Despite the downward trend in capital invested, deal activity picked up in Q1 2023, with 439 deals raised vs. 366 in Q4 2022. The gains were largely driven by relative gains in pre-seed deal activity (89) after a dismal Q4 2022 that saw only 42 pre-seed deals.

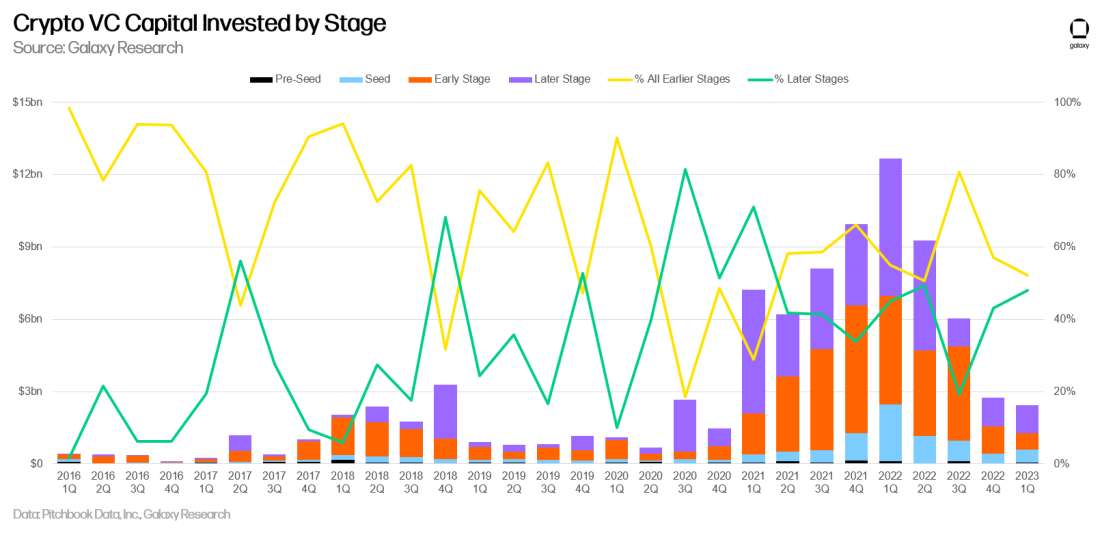

In terms of capital invested, almost an equal share of capital was deployed in earlier stage companies (pre-seed to Series A) vs. later stage companies (Series B+).

VC Investing by Company Vintage

Companies founded in 2021 and 2022 completed the most venture deals in Q1 2023.

Despite the near even deal count between 2021 and 2022 vintages, companies founded in 2021 commanded the most capital invested in Q1 2023. Intuitively, companies founded in 2021 are older than those founded in 2022, and thus raise larger amounts of capital at their later stages, which accounts for the divergence.

Crypto VC Capital Invested & Deal Count by Company HQ

Companies based in the United States dominated by both deals completed and money raised. US-based companies raised 42.8% of all crypto VC money in Q1 2023, followed by France (19.4%), Canada (6.6%), and Switzerland (4.1%).

The picture is similar when looking at deals completed. US-based companies completed 42.3% of all crypto VC deals in Q1 2023, followed by the United Kingdom (8.5%), Singapore (6.2%), Canada (4.1%), and Switzerland (3.9%).

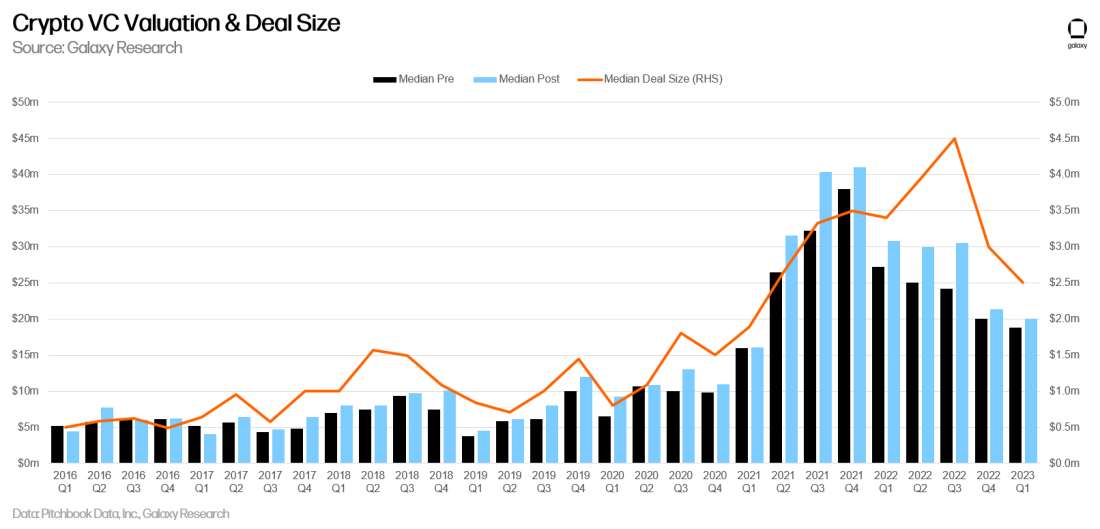

Crypto VC Deal Size & Valuation

In Q1 2023, deal sizes and pre-money valuations for crypto VC rounds were at their lowest point since the beginning of 2021. The median crypto VC deal in Q1 2023 was $2.5m on an $18.8m pre-money valuation.

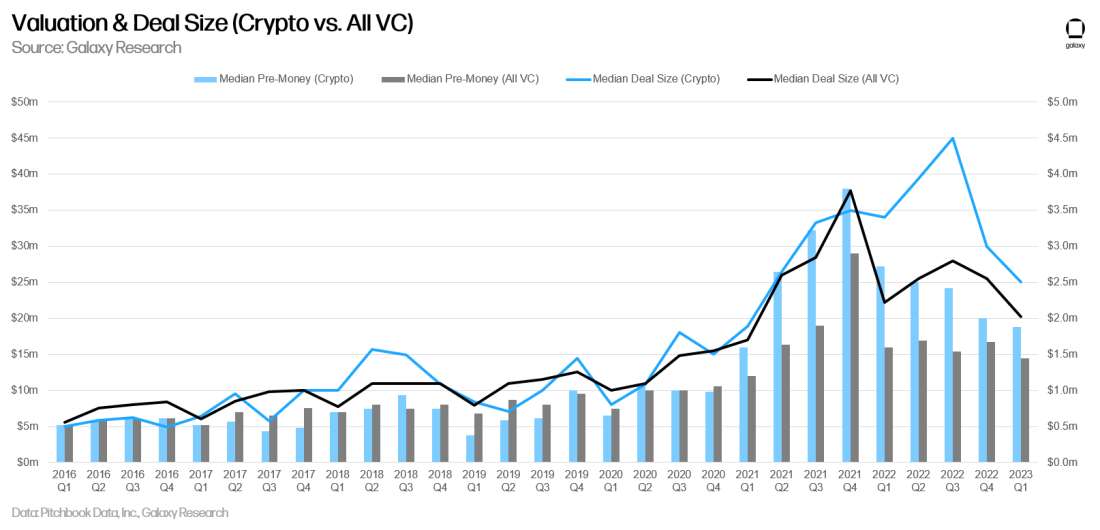

The declines in crypto VC deal size and valuation mirror declines in the broader VC market.

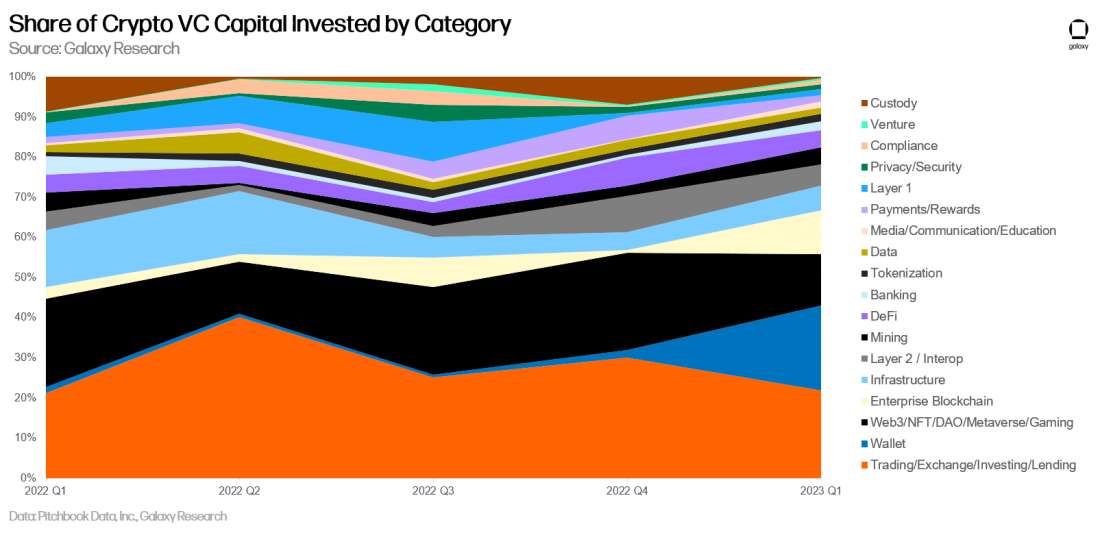

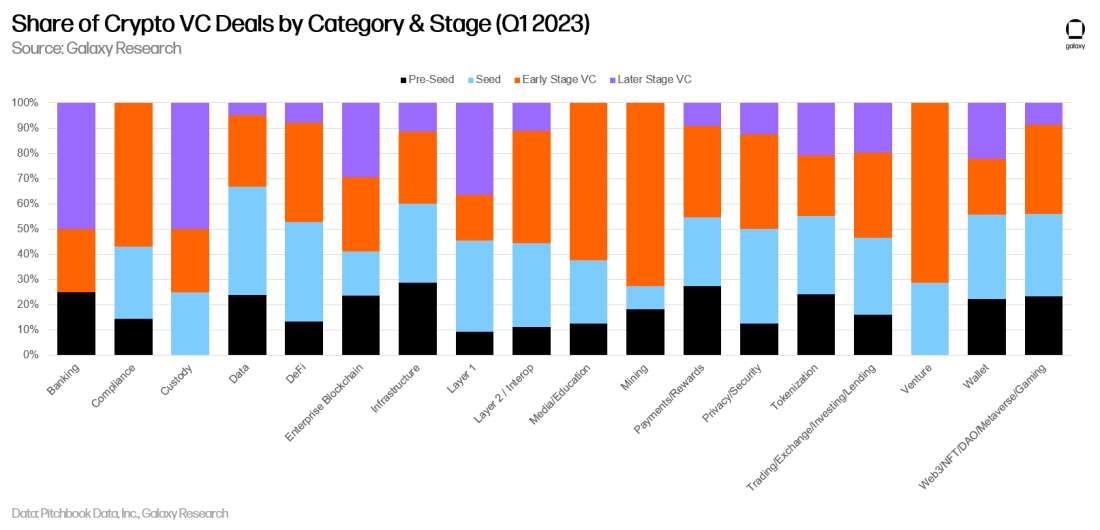

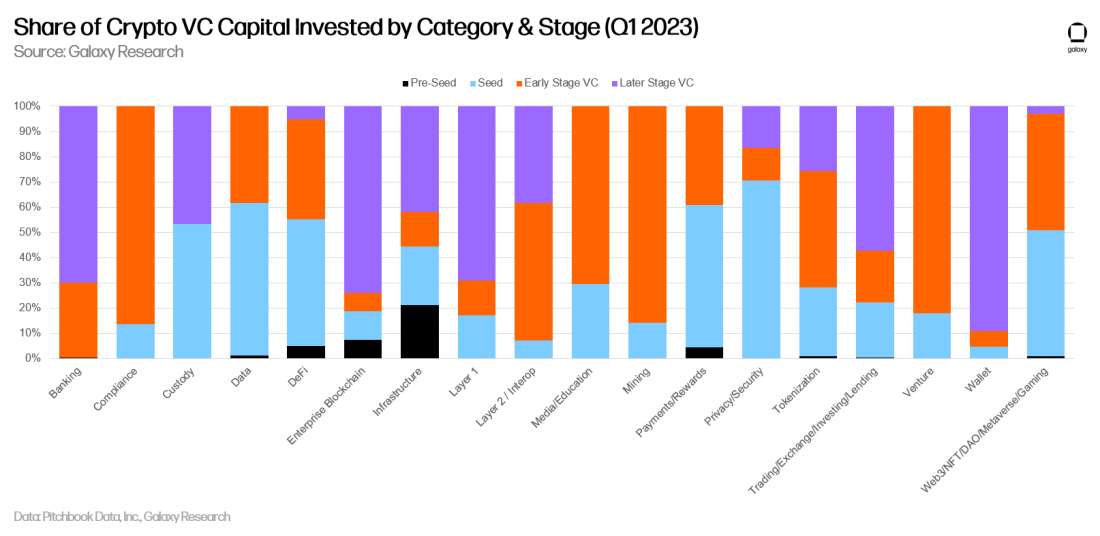

Crypto VC Investment by Category

Trading, Exchange, Investing, and Lending startup raised the most venture capital in Q1 2023 ($538m, 22% of all money raised), while Wallet companies raised the second largest share ($519m, 21%). The Wallet segment was dominated by hardware wallet manufacturer Ledger, which raised a $108m extension in March 2023 to its $386m 2021 Series C.

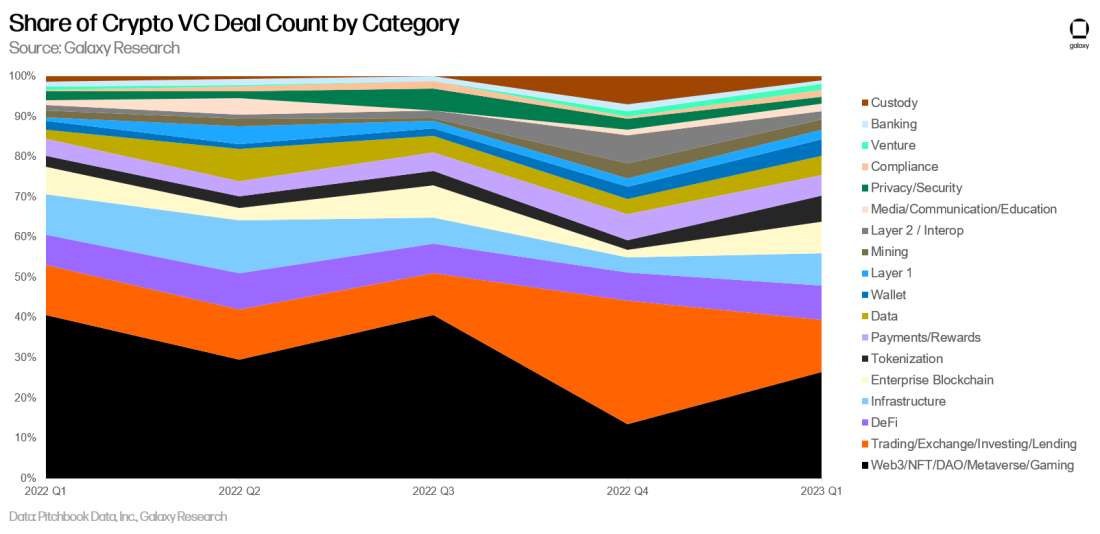

By deal count, companies building in the Web3, NFT, DAO, Metaverse, and Gaming subsector regained the top spot, followed by Trading, Exchange, Investing, and Lending companies.

When evaluating category investment by fundraising stage in Q1 2023, a clearer picture of crypto VC activity comes into view. The largest share of deals done at a later stage was in the Mining category, while the Infrastructure category, which includes node hosting and staking-as-a-service companies, had the largest share of deals done at the pre-seed stage. Two of the biggest categories (Web3/NFT/DAO/Metaverse/Gaming and Trading/Exchange/Investing/Lending) were roughly split by stage in terms of deals completed.

In terms of capital invested, the Wallet and Enterprise Blockchain categories saw the largest share of capital go to later stage companies, while the Infrastructure category saw the largest share of pre-seed investment. Understandably, Trading/Exchange/Investing/Lending companies had a large share of capital invested in later stage companies, while the newer category of Web3/NFT/DAO/Metaverse/Gaming companies had very little capital invested to companies at the latest stages.

Crypto VC Fundraising

We worked with Galaxy Asset Management to compile information on venture capital fundraises in Q1 2023 – that is, money raised by VCs for new funds or new fund vintages. Q1 2023 saw the fewest new funds launched since (14) and lowest money allocated ($2.23bn) since the beginning of 2021 and end of 2020, respectively.

Average new fund size continued to increase in Q1 2023, reaching $211m, while median fund size declined for the first time since 2020 ($62.5m).

Analysis & Conclusions

There is no doubt that crypto VC is experiencing a bear market along with cryptoassets themselves. But the declines in crypto VC activity (deal count, money invested, and funds raised) are not particularly divergent from the pullback across the broader VC landscape, for which the rising rates environment bears significant blame. Other important takeaways from Q1 2023’s crypto VC data include:

Crypto VC activity is roughly double the prior crypto bear market. Despite significant drawdowns from the all-time highs in venture activity seen in 2021 and 2022, crypto VC activity remains elevated when looking back to the crippling previous crypto winter, even despite the rising rate environment stifling allocator interest. If the current pace holds exactly, albeit an unlikely scenario, 2023 will see more money invested than 2018, the biggest year for crypto VC prior to the last bull market.

Venture investors face a tough fundraising environment. There is no doubt that rising rates have resulted in an environment where allocators are less keen to bet on long-tail risk assets like venture funds than they were under a decade of zero interest rate policy. When combined with the bear market in cryptoasset prices and the fact that many allocators feel burned after the spectacular blowups of several venture-backed companies in 2022, venture investors will find it difficult to raise new funds in 2023.

The lack of significant new venture dollars will continue to pressure founders. The era of “growth at all costs” is over, at least for now, and venture-backed startups need to prepare for a difficult fundraising environment for the foreseeable future. Founders must focus on revenues and sustainable business models and be prepared to raise smaller rounds and give up more equity. The founder-friendly environment of the last several years is in the rearview mirror.

Pre-seed deals are picking up. After a dismal fourth quarter in 2022, the number of pre-seed deals is rising on both a relative and absolute basis. 20% of all crypto VC deals completed in Q1 2023 went to the earliest stage companies, an indication that entrepreneurs are active and venture investors are attentive. With many exiting crypto entirely during the bear market, savvy investors may find gems among the die-hards who found companies in a challenging environment, as they did during the prior bear market.

The United States continues to dominate the crypto startup ecosystem. Despite an unclear if not shaky regulatory environment and even outright antagonism, crypto startups based in the United States continue to pull the vast majority of venture capital activity. US-based companies dominate the crypto ecosystem, and policymakers seeking to retain top talent, promote technological and financial modernization, and extend American leadership into the economy of the future would be wise to develop progressive policies that foster growth and innovation.

New and old categories are seeing growth. While the long-dominant category in crypto of Trading, Exchange, Investing, and Lending companies continues to see significant activity, the newer category of Web3, NFT, DAO, Metaverse, and Gaming companies, which includes everything from NFT marketplaces to DAO tooling to blockchain-enabled game developers, continues to see significant capital invested and deal counts, particularly at earlier stages. Conversely, older concepts like Tokenization and Enterprise Blockchain saw growth in both deal count and capital invested in Q1 2023, a sign that the market is hunting for “blockchain use-cases,” and we expect that tokenization and blockchain use-cases will continue to mature and evolve in 2023, particularly given the crypto bear market and challenging US regulatory environment. That being said, crypto is global, and demand for new economic and community models, as well as access to cryptoassets, continue to be the biggest drivers of venture activity.

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2023. All rights reserved.