Crypto & Blockchain Venture Capital – Q2 2022

Despite the drawdown in crypto markets, venture funding for the crypto and blockchain industry has continued to pour in.

Key Takeaways

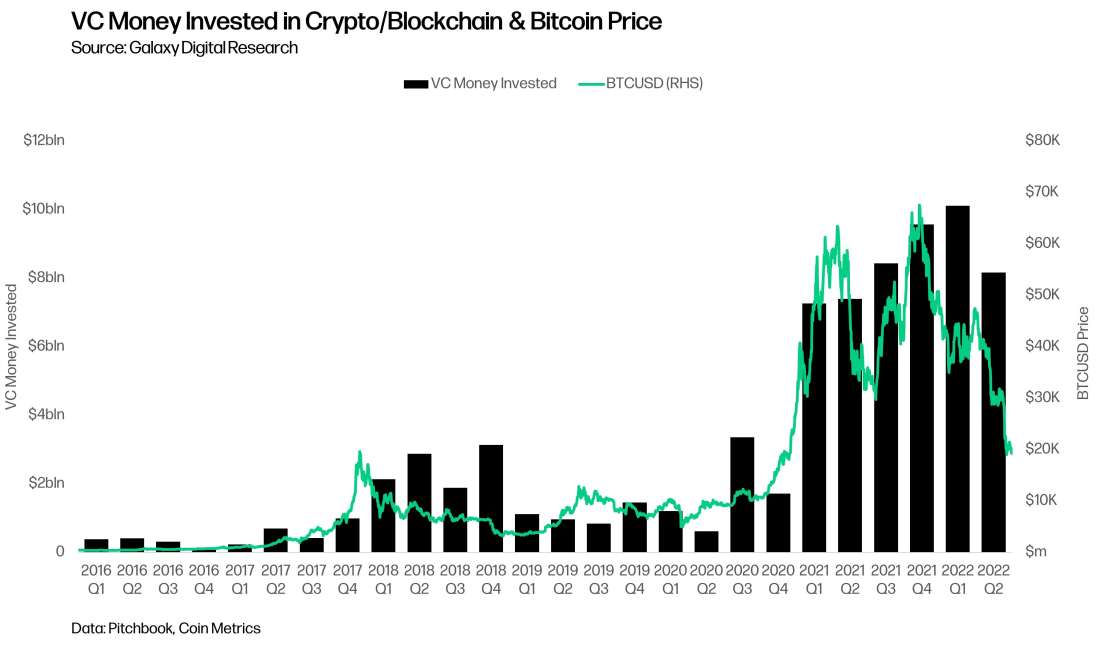

In Q2 2022, venture capitalists invested more than $8 billion in crypto startups, the fourth-largest quarterly sum ever. The conclusion of Q2 marks the first down quarter in total money invested since the beginning of 2021, but the haul was still more than $6 billion above the 7-year average.

For six quarters in a row, valuations and deal sizes in crypto and blockchain have dwarfed the broader VC landscape.

Later-stage companies attracted the largest sum of VC money, but early-stage companies attracted the largest share of deals completed.

Trading/exchange/investing/lending led all subsectors in total capital invested, but Web3/NFT/DAO/Metaverse/Gaming led in the share of deal count by a large margin.

VC Money & Deal Count

For the first time since the beginning of 2021, venture capitalists invested less money in the crypto and blockchain sectors than in the previous quarter. Despite the decrease, the $8 billion invested in Q2 is more than $6 billion greater than the 7-year average of $2.1 billion. The reduction in capital invested was accompanied by a significantly lower deal count of 582, but still the third-highest deal count of all time.

Companies founded in 2018 attracted the most VC money in Q2 of 2022, with over $1.9 billion invested.

Investments by Stage

Continuing a trend from the last two quarters, the share of capital allocated to later-stage companies continued to rise and outpaced earlier stage companies for the first time in Q3 2021.

Deal Count by Stage

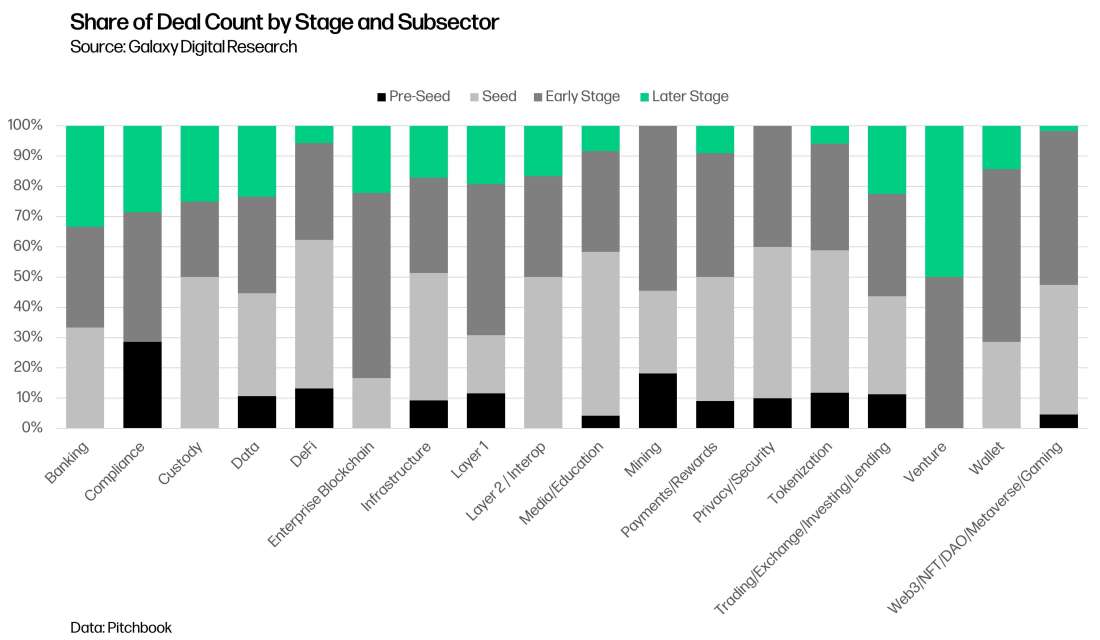

Last quarter’s total deal count was well below the all-time high in Q1 2022, although the deal count remains robust with Q2 2022 seeing the third most deals completed in history. Q2 2022 saw less than half the pre-seed deals as Q1, with pre-seed deals now accounting for less than 10% of all deals for the first time.

Valuation & Deal Size

After a brief respite in Q1 2022, both Median Pre and Median Post valuations have made all-time highs.

Venture capital valuations and deal size in Crypto/Blockchain continue to dwarf the broader VC industry.

Investments by category

Q1 2022 saw the meteoric rise of VC money in Web3, NFT, DAO, Metaverse, and Gaming, but Q2 2022 capital flow painted a different picture. Trading, Exchanges, Investing, and Lending took the pole position with more than $2.3 billion invested; data and infrastructure attracted $1.6 Billion and $1.3 billion, respectively.

VC deal count by subsector paints a different picture, with Web3, NFT, DAO, Metaverse, and Gaming sectors far outpacing that of any other subsector.

In almost every subsector, seed and early-stage deals accounted for most deals completed. Notably, nearly 30% of deals completed in the compliance subsector occurred at the pre-seed stage, indicating market demand for new compliance offerings.

Conclusions

Examining the data from Q2 2022 leads to several takeaways on trends in the crypto and blockchain startup investment landscape:

Total VC money invested remained extremely robust, despite the falling Bitcoin price YTD. Q2 2022 saw the price of Bitcoin fall from peak to trough by -62% and the price of Ethereum by more than -75%. Despite the significant drop in liquid crypto asset prices, venture capital flows remained extremely robust in the crypto and blockchain sectors. While Bitcoin and Ethereum each fell below their 2017/2018 highs, the total money invested in the industry reduced by only 20%, from $10bn to $8bn, and remained more than $5bn above 2018 levels. Despite declining crypto prices and tightening financial conditions, VC investor appetite remains resolute and will likely result in elevated investments throughout the year.

For the first time, pre-seed deals accounted for less than 10% of all deals. In just six years, the share of deals done by pre-seed companies fell from 53% to 8% in Q2 of 2022. Our Q1 VC report provided insight into the causes of this decline, and in Q2 2022 they appear to persist.

Early in the crypto industry, the market was immature and lacked the necessary infrastructure to build upon efficiently. Entrepreneurs saw this need and jumped at the opportunity, resulting in an explosion in early-stage equity investments. Today, many of those same companies are some of crypto’s major players and are now raising at higher valuations and later stages. With most of the glaring structural needs now met, the opportunity for to create new startups to meet glaring market infrastructure needs is diminished.

A decentralized ethos is fueling many of the builders and entrepreneurs today. New entrants are building products or services on-chain and thus do not raise capital through traditional channels that are trackable through Pitchbook. Defi, DAOs, and NFTs are use cases that allow founders to raise capital and deploy products or services more anonymously.

Later Stage companies attracted the largest share of VC money in Q2 2022. However, along with this outperformance, the stage remained flat in QoQ deal count and saw a decrease in median pre-money valuations.

The greater share of capital allocated to later-stage companies last quarter could signal that mature companies with proven business models were more attractive to capital allocators due to recent market dynamics. In crypto bear market cycles, bitcoin market cap dominance typically rises, illustrative of a “flight to safety” away from new projects and protocols and back to Bitcoin. During bear markets, this dynamic is not always due to an increase in Bitcoins price but more a relative decrease in altcoins price. Transposing this to the VC market, the dominance of later-stage firms may be less the result of their performance and more the result of tepidness on the part of venture investors to make riskier, early-stage bets. The crypto and blockchain industry has matured tremendously and now has a collection of established reputable companies that can attract a more consistent flow of capital during market turmoil. The data provided in this report shows that older and more mature companies founded in 2018 led in VC money invested; firms founded in 2017 and 2015 attracted the 2nd and 3rd most VC money.

The divergence between an increase in money invested and a decrease in median pre-money valuations is most likely a sign that VC investors have still been investing, the founder-friendly dynamic we have seen may be starting to abate. Said differently, VC investors are getting a better deal, with founders in precarious capital situations suffering more dilution to attract investment.

Trading/exchange/investing/lending and Web3/NFT/DAO/Metaverse/Gaming continue to show strength compared to other subsectors. Although the subsectors have given up ground in their share of deal count and VC money raised, they continue to be a central focus for VC investors. Trading/exchange/investing/lending increased its share of VC money invested, pulling in $2.4 billion, but decreased slightly in its share of deals. Web3/NFT/DAO/Metaverse/Gaming saw its share of VC money invested and deal count decline but still managed to attract over $1.1 billion in Q2 2022.

More money and deals are flowing to the data & Infrastructure subsectors; together, they accounted for $2.97 billion of all venture investment in Q2 2022, a 33% share. Data companies saw their share of money invested grow by 16% from Q1 to Q2. The closely related subsectors play an integral part in the adoption of crypto, user experience, and regulatory compliance. Crypto & blockchain adoption is accelerating rapidly, and along with it comes a demand for expertise in data analytics, network architecture, and UI optimization. Infrastructure and data companies are instrumental in stress testing and fortifying the industry to ensure systems run optimally. As crypto crosses the chasm into the early majority phase, more capital and attention will likely flow to the data and infrastructure subsectors.

Crypto and Blockchain companies continue to garner higher median pre-money valuations and deal sizes than the broader VC landscape. In Q2 2022, median pre-money valuations for crypto/blockchain companies were double that of the median across all venture capital, $40 million and $20 million, respectively. The median deal size from the quarter paints a similar picture, with crypto/blockchain companies seeing 28% more money invested in their deals than the median across all venture capital. The strength of crypto and blockchain deal sizes and the high valuations are testaments to the significant amount of capital seeking to allocate to the crypto and blockchain sector. While there have been some reported instances of down rounds or another repricing, on balance, we have yet to see the type of reduction in valuations that a prolonged bear market would suggest.

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsement of any of the stablecoins mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2022. All rights reserved.