Top Stories of the Week - 9/1

This week in the newsletter, we write about Grayscale’s legal win at the DC Circuit Court of Appeals, the IRS proposal on the broker rule, and the SEC’s settlement with an NFT issuer.

Subscribe here and receive Galaxy's Weekly Top Stories, and more, directly to your inbox.

Grayscale Wins Suit Against SEC over GBTC

On Tuesday, a panel of three judges of the US DC Circuit Court of Appeals unanimously ruled in Grayscale’s favor by vacating the SEC’s denial of Grayscale’s application to convert GBTC to a spot ETF. The decision effectively sends Grayscale’s application back into the SEC’s bitcoin ETF approval queue. Writing for the court, Judge Rao said that “the denial of Grayscale’s proposal was arbitrary and capricious because the Commission failed to explain its different treatment of similar products.”

Grayscale first applied to convert GBTC into an ETF that would be listed on the New York Stock Exchange’s Arca market in October 2021. The SEC rejected the application in June 2022 and Grayscale sued just days later under the Administrative Procedures Act. Specifically, Grayscale argued that it was unfair and arbitrary for the SEC to approve futures based ETPs but deny its spot ETF. Ruling in favor of Grayscale, the Court specifically disagreed that futures and spot ETFs are distinguishable, “The Commission’s unexplained discounting of the obvious financial and mathematical relationship between the spot and futures markets falls short of the standard for reasoned decision making.”

The SEC has repeatedly denied past spot ETF applications for a lack of surveillance sharing agreements that cover a regulated market of sufficient size. On this topic, the Court wrote, “The surveillance sharing agreements with the CME are identical and should have the same likelihood of detecting fraudulent or manipulative conduct in the market for bitcoin and bitcoin futures.” In a 2021 filing supporting the Wise Origin bitcoin ETF filing, quants at FMR (Fidelity) presented evidence that the “CME bitcoin futures market has consistently led Bitcoin price discovery across global USD bitcoin markets,” suggesting that surveillance of futures markets should be sufficient to prevent market manipulation.

As a next step, the SEC can appeal the case, either directly to the U.S. Supreme Court, or they can seek an en banc rehearing by the DC Court of Appeals, which would have the case reheard by a full panel of circuit court judges (as opposed to the 3-judge panel that ruled on this case).

Bitcoin jumped almost 10% on the news, but in the days following Grayscale’s court win, BTC has entirely retraced to its pre-ruling levels around $26k.

OUR TAKE:

The ruling is a rebuke for the SEC, but does not guarantee that a GBTC conversion is immediately forthcoming. The outcome of the case, in practical terms, kicks Grayscale’s application back into the SEC’s increasingly crowded Bitcoin ETF queue. It’s unclear whether the clock on Grayscale’s application now completely restarts or whether the SEC must re-review it on an expedited time frame.

The ruling is a setback for the SEC’s ability to deny a spot bitcoin ETF. A spot Bitcoin ETF provides safe, transparent, efficient, and simple exposure to Bitcoin for large swaths of investors who currently lack sufficient market access vehicles. Repeated SEC rejections have resulted in the U.S. lagging behind other nations in this space, with at least 13 jurisdictions already offering spot-based Bitcoin ETPs, including major economies like Canada and Brazil.

While it’s possible the SEC will re-review GBTC’s conversion application and deny it for a different reason, two of their strongest arguments are now off the table – that spot and futures ETFs are different, and that surveillance sharing agreements and market sizing do not support a spot ETF. Other ETF applications, such as the amended filings from other issuers in June, are also likely on stronger footing following the ruling. (Note: all that Bitcoin ETF applications filed in June, such as those from BlackRock, Fidelity, and Invesco/Galaxy, were delayed yesterday by the SEC, with the next deadlines for SEC approval/denial/delay coming in mid-October).

The SEC is unlikely to appeal this case directly to the Supreme Court since that court has recently proven very hostile to regulatory overreach and the administrative state, generally, and furthermore the Supreme Court could deny a writ of certiorari (refuse to hear the case). While an en banc appeal is more likely, if the SEC is already in the mood to approve a Bitcoin spot ETF, as clearly some of the proposed issuers believe given their applications in June, then perhaps it’s a waste of time to bother with an appeal. - Alex Thorn

SEC Charges Impact Theory for Unregistered Offering of Securities as NFTs

The SEC charged the founders of the NFT collection, Impact Theory, with an unregistered securities offering for the sale of its NFTs. Impact Theory, a Los Angeles-based company that produces entertainment and educational content, raised $29mn through primary sales of Founder's Keys NFTs from October 13, 2021 to December 6, 2021 and almost $1mn from royalties on secondary sales. The NFTs functioned as a membership pass granting holders access to events, future projects, collaborations, and discounts on paid content.

The SEC claims that purchasers of Impact Theory's NFT had reasonable expectations of obtaining future profits based on Impact Theory’s managerial and entrepreneurial efforts. During the initial NFT sale, Impact Theory emphasized that the company was “trying to build the next Disney,” and, if successful, it would deliver “tremendous value” to purchasers. Additionally, the team alluded that in the event the project is successful, the value of the NFTs would be significantly greater than their original purchase price. The SEC's claim that purchasers of the NFT expected future profit based on Impact Theory's efforts was reinforced by statements saying they would use NFT proceeds to fund the project’s future development.

As part of the settlement, Impact Theory is now obligated to comply with the following SEC requests:

Destroy all NFTs in its possession or control

Provide an official notice to the community on the projects closure

Revise the smart contract metadata underlying the NFTs to eliminate any royalty that Impact Theory might receive from future secondary sales

Assist the Commission staff in the administration of a monetary relief distribution plan to affected investors

Pay disgorgement of $5.12mn, prejudgment interest of $483k, and a civil money penalty of $500k to the SEC

In a statement on Twitter/X, Impact Theory Founder Tom Bilyeu announced they had settled with the SEC but would continue to “operate our go-forward business consistent with our good faith best understanding of all applicable laws, rules, and regulations.”

OUR TAKE:

This is the first time the SEC has taken an enforcement action against a company for the sale of an NFT as an unregistered security, marking a significant regulatory development for US-based NFT issuers. Despite the SEC's longtime campaign against unregistered securities offerings in crypto, NFTs had largely evaded the agency's spotlight. The SEC's decision to charge Impact Theory sends a clear warning to other NFT collections. Most NFT projects today offer roadmaps that allude to added value for holders in the future. While a segment of collectors purchase NFTs for their artistic appeal, many view them as licenses to a brand's intellectual property and/or speculative vehicles. Markets have often valued NFTs partially based on the founding team’s marketing plans, roadmap, and real-world applications.

Although we have seen substantial partnerships with NFT projects and notable companies/individuals, these examples never explicitly mention the intentions of increasing monetary value for NFT holders. However, these types of developments could create buying pressure and increase the NFT’s floor price. Based on the SEC suit against Impact Theory, it’s likely that similar projects are also in their crosshairs due to the SEC’s view that NFT holders have an expectation of profit derived from the efforts of others; the last two prongs of the Howey test. The SEC's stance, which interprets brand growth initiatives by NFT creators as offerings of unregistered securities, is poised to make NFT collections reconsider their marketing strategies.

In the wake of SEC's expending its self-proclaimed, scarce resources on an irrelevant NFT project down 67%, SEC Commissioners Hester M. Peirce and Mark T. Uyeda voiced a strong dissent. They stressed that the NFTs in question neither represented company shares nor yielded dividends for buyers. The dissent also highlighted the SEC's inconsistency; the agency typically refrains from regulating sellers of tangible goods (like watches or paintings) who may broadly promise to bolster brand value for better resale prices. In this light, why should NFTs be treated differently? Pierce, a known advocate for sound crypto regulation, and Uyeda also argued the SEC should have taken the time to build out a clear regulatory framework and offer “guidance when NFTs first start proliferating” rather than waiting till now.

While the SEC's actions against Impact Theory may serve as a precedent for NFT collections to sidestep regulatory pitfalls, the NFT realm needs a transparent regulatory framework. This will ensure founders can evolve their brands without regulatory fears. Otherwise, as the NFT market strives to recover from a downturn, enforcement by regulation will continually threaten its growth. - Gabe Parker

DeFi Questions After IRS Proposes “Broker Rule”

The Treasury issued its proposed regulations to require certain digital assets entities to provide tax reporting as “brokers.” On Friday Aug. 25, the Treasury issued its proposed regulations emanating from the authority granted in the Infrastructure Investment & Jobs Act. The proposed language is quite expansive and would require IRS tax reporting from a wide swath of entities, even including many non-custodial services.

For background, In August 2021, when Congress was weighing President Biden’s Infrastructure Bill, later named the “Infrastructure Investment & Jobs Act,” language was included that broadened the IRS’ tax reporting rules to include a wide swath of entities in the digital assets ecosystem. At that time, we wrote that this language was ‘bad and needs to change,’ arguing that the language was highly problematic because it could require IRS reporting from several types of previously un-covered entities, including several that functionally will be unable to comply.

Under the proposed rules, digital asset entities that qualify as brokers would need to 1) perform KYC on their users and 2) furnish Furnish individual users and the IRS with transaction information (including gross proceeds) for digital asset sales/conversions on Form 1099-DA.

The IRS is accepting public comments until October 30, and if adopted, the rules go into effect for the 2025 tax year (for taxes filed in 2026).

OUR TAKE:

The rules represent a rather substantial expansion of the definition of “broker” for IRS tax reporting purposes. While it’s noncontroversial and perhaps trivial for centralized entities, such as custodians or trading firms, to comply with the rules, the expanded definitions would also capture large swaths of DeFi as it exists today. Specifically, any “facilitative service” that is “in a position to know” its customers’ information and profit-and-losses would qualify as a broker and need to perform tax reporting. “In the position to know” is a significant expansion of the prior language (“ordinarily would know”) because it essentially says that if a digital asset entity could know this information about its users, it must know it. The IRS states that “the ability to modify the operation of a platform to obtain customer information is treated as being in a position to know that information.” The IRS clarifies multiple times that upgradeable smart contracts, whether by governance or admin keys, counts as being “in a position to know” and thus would have to comply.

This standard would capture most website front-ends for DeFi, but also many DeFi applications (i.e., smart contracts) themselves. Non-custodial wallets that provide trading services, whether through a centralized liquidity provider or simply by constructing DEX transactions on behalf of the user, would also qualify as brokers here, including many popular browser extension wallets. (Layer 1 miners and validators, as well as hardware or software wallet providers that do not offer the ability to buy or sell within their platforms, are exempted from the “broker” designation).

It’s very possible that the pragmatic effect of these rules, if they come into force (and we believe there is a strong likelihood that they are enacted with minimal changes), is the wholesale relocation of DeFi outside the U.S., which is a precarious suggestion given that these applications live on global, permissionless ledgers whose jurisdictional nexus is still an uncertain question of law. Rather than undertake the burden of complying (which may have the practical effect of neutering core features), some applications and developer teams may decide instead to try to ban U.S. users, effectively creating a “Great American Firewall” around what many consider to be the future of finance. For more detailed analysis, read our new report from today IRS Broker Rule Puts DeFi in Tough Spot. - Alex Thorn

Charts of the Week

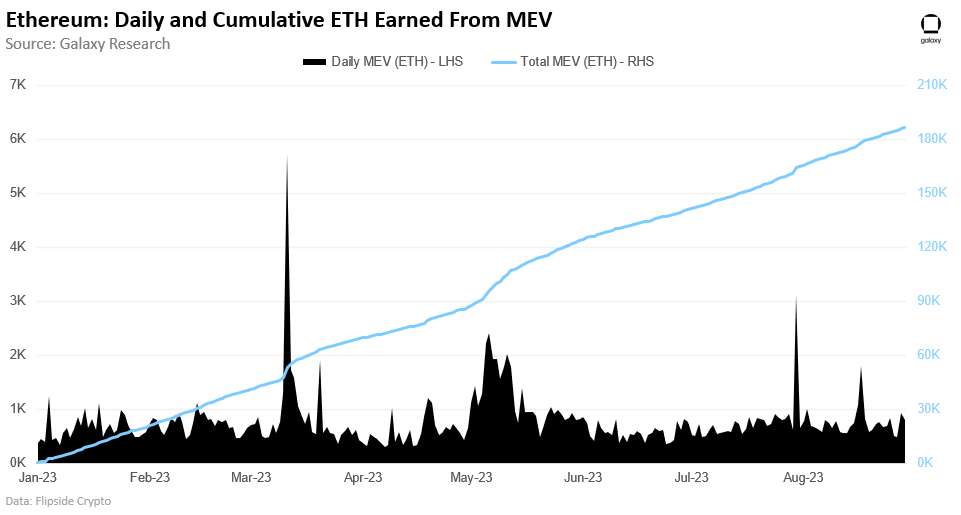

Validators have earned a cumulative 187k ETH in MEV rewards so far in 2023 at an average of 776 ETH per day. The highest daily MEV reward amount was 5,743 ETH on March, and the lowest daily MEV reward amount was 299 ETH on April 7.

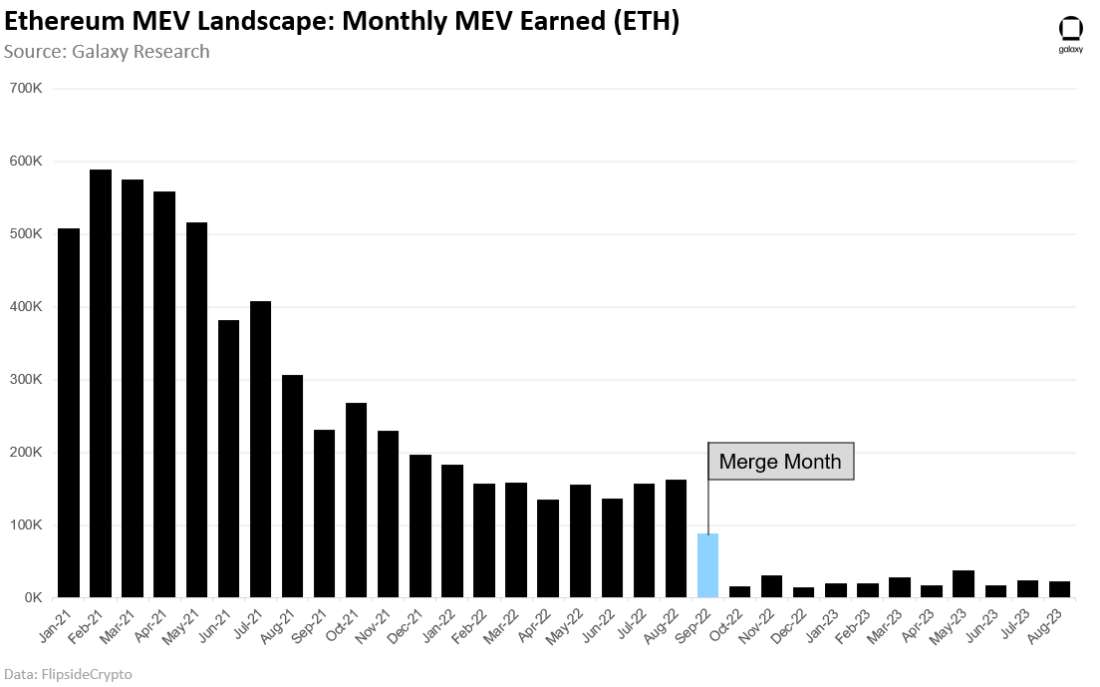

Broadening the view, we can observe the impact of the merge on the MEV rewards earned by validators. On average, validators earned 481k ETH per month in the 8 months leading up to the merge. In the post-merge era, this value has dropped to 108k ETH (-63%). A lag in adoption of MEV boost, the software that allows validators to earn MEV, post-merge has contributed to the decline in rewards earned by validators. See this Dune dashboard to learn more on MEV boost in the post-merge regime.

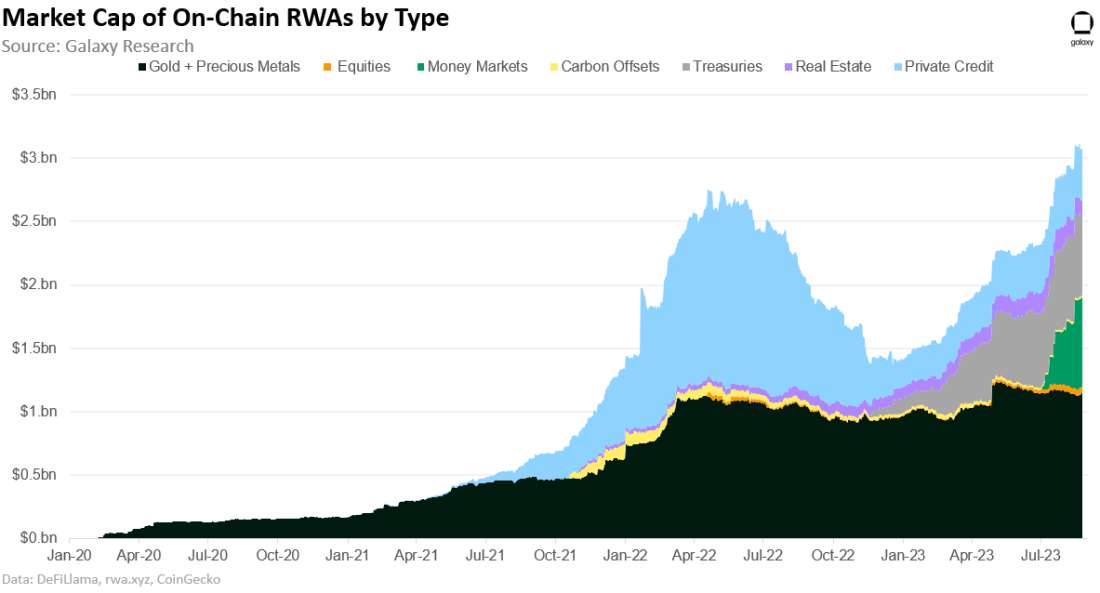

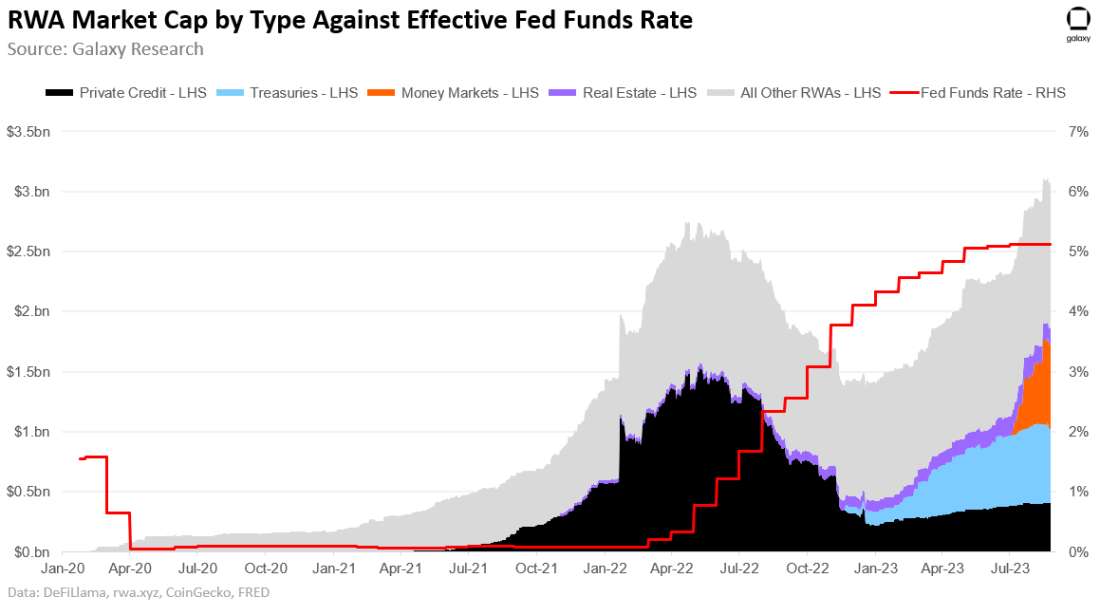

The value of real world assets (RWAs) on-chain crossed the $3 billion mark on August 14 (now at $3.1 billion). This exceeds the value of their previous all-time high of $2.75 billion (set in April 2022) by 13%. The value is comprised of 37.3% gold and precious metals; 1.63% equities; 0.41% carbon offsets; 22.98% money markets; 20.04% treasuries; 4.38% real estate; and 13.27% private credit. As it currently stands, inherently yield-bearing RWAs capture 61% of the cumulative RWA market cap.

The recent expansion of RWAs has been fueled by on-chain demand for off-chain sources of yield. In the wake of aggressive rate hikes, yield-bearing RWAs (i.e. treasuries, money markets, real estate, and private credit) have grown by $1.44 billion; accounting for 87% of the $1.66 billion in value added to RWAs this year.

Other News

Binance Pool launches Ordinals Inscription Service for Bitcoin

Swift says interoperability experiment with Chainlink’s CCIP was successful

Uniswap founder Hayden Adams hails 'based' scam tokens ruling

Coinbase set to list PayPal stablecoin PYUSD

Crypto bank SEBA obtains approval-in-principle in Hong Kong for crypto-related services

Polygon Labs unveils Chain Development Kit to develop and connect Ethereum L2s

Base set to receive 118M OP tokens over six years in governance agreement

Binance to 'gradually' end support for BUSD products

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2023. All rights reserved.