Top Stories of the Week - 12/22

This week in the newsletter, we talk about Solana’s mobile phone, stablecoin ratings, and Ethereum’s next upgrade. Christine Kim has notes on the latest Ethereum dev call.

Subscribe here and receive Galaxy's Weekly Top Stories, and more, directly to your inbox.

Solana Mobile’s Saga Sells Out, Boosted by Bonk Airdrop

Solana's debut smartphone, the Saga, sold out its initial 20,000-unit stock last week. The surge in demand was driven by an included airdrop of BONK, the leading Solana memecoin by market cap, which at the time was valued higher than the phone itself. This prompted speculators to buy the phone, aiming to profit from then selling the airdropped Bonk.

The Saga, launched in May 2023, and faced challenges gaining traction. Less than 3,000 units were sold in the six months following its launch, even after Solana Mobile reduced the Saga price by nearly 40%, and highly influential tech Youtuber Marque Brownlee rated it poorly. As highlighted in our Solana report, Solana’s founder, Anatoly Yakovenko, previously worked at Qualcomm and has experience with mobile systems.

Bonk was launched in December 2022 when the Solana ecosystem was still reeling from the collapse of FTX. 50% of the supply was air-dropped to 40+ Solana NFT collections, with additional supply allocated to Solana developers, traders, and artists. It quickly became Solana’s leading memecoin, revitalizing the chain during a period when many had abandoned it. This status was further cemented during Solana’s recent resurgence. Today, BONK has over 600k holders and 118 application integrations and is available on 10 blockchains.

OUR TAKE:

Bonk’s meteoric rise, for the second time since its launch, has completely reframed the narrative surrounding Solana, this time reviving interest in Solana’s foray into mobile. Just a few weeks ago, Anatoly admitted that Saga had struggled to gain adoption, pointing toward the use of progressive web apps and passkeys as making it unnecessary for device integrated with crypto-native functionality.

There were two primary motivations behind launching Saga and SMS. Over 90% of the world accesses the internet via their mobile device and Solana wants to be at the forefront of providing those users with a secure and accessible crypto experience. Additionally, crypto mobile developers face an onerous and extractive process when using traditional app stores like Apple’s App Store and Google Play. Each enacts content moderation that sometimes prohibits certain types of crypto applications and each extracts significant portions of revenue that could otherwise go to application developers (Apple takes 30% while Google takes 15-30%).

Sales alone, however, are not a perfect measure of success. Saga’s real objective is to disrupt the mobile phone industry and force other original equipment manufacturers such as Samsung, Google, and Apple to introduce their own phones with crypto-native functionalities. Selling out the Saga is a good initial step, but the focus now shifts toward cultivating a sticky and involved user base that makes it viable for developers to launch mobile products with real traction.

Following the sellout, Anatoly tweeted, ‘Once developers start releasing crypto-incentivized apps to all Saga users, it should kickstart the flywheel. Users interested in crypto incentives will adopt the phone, giving developers a concentrated distribution channel filled with users seeking those incentives, and all without any app fees.” Events over the past week appear to have validated this thesis, with users already anticipating what future applications, and incentives, holders might benefit from. – Lucas Tcheyan

Credit rating agencies look to grade stablecoins

S&P Global Ratings launches Stablecoin Stability Assessment. Credit rating agency S&P Global introduced its stablecoin stability assessment, an analytical risk framework to evaluate a stablecoin's ability to maintain its dollar peg. The assessment grades eight of the leading fiat-backed and crypto-collateralized stablecoins on a 1 to 5 scale with 1 being 'very strong' and 5 being 'weak'. Quality of the backing assets is the primary scoring factor in the assessment, which also factors in other qualitative assessments on: governance, legal & regulatory, redeemability, 3rd party dependencies, and track record.

USDC was graded at a 2 overall with the asset quality behind the stablecoin graded as 'very strong' but S&P noted that the "stablecoin stability assessment is 2 (strong) to reflect our view of insufficient precedent on whether assets would be protected in the event of bankruptcy of Circle." Meanwhile, Tether received a 4 (weak) rating, which reflects several weaknesses including: (i) 'lack of information on entities that are custodians, counterparties, or bank account providers of USDT's reserves', (ii) 'significant exposure to higher-risk assets with limited disclosure', and (iii) 'limited transparency on reserve management and risk appetite, lack of a regulatory framework, no asset segregation to protect against the issuer's insolvency, and limitations to USDT's primary redeemability.' S&P's final summary scorecard ratings:

2 (strong): Gemini Dollar (GUSD), Pax Dollar (USDP), USD Coin (USDC)

4 (constrained): Dai (DAI), First Digital USD (FDUSD), Tether (USDT)

5 (weak): Frax (FRAX)

OUR TAKE:

Major depegs and failures of stablecoins in recent years have demonstrated that many crypto users were unaware of many of the risks associated with stablecoin products. S&P is looking to extend its credit rating experience into the stablecoin market to help uncover some of the inherent risks of using various stablecoins in a simple 1-5 scoring system for prospective non-technical users to understand. While this is an important gap that S&P is aiming to fill to help bridge between real-world assets and crypto, we see several structural flaws in their methodology.

Stablecoin asset quality is rightly the key driving factor for scores, but the other qualifying factors around the governance, operational setup, redeemability and third-party dependencies deserve more structured considerations. As noted in some of our pastresearch, stablecoin holders typically exit their positions by swapping for other assets on DEXes rather than directly redeeming through the issuers, leading to increased reliance on third-parties to maintain price stability. Even if collateralized entirely by T-bills and overnight reverse repos, a stablecoin still faces risk of depeg from duration mismatch or insufficient liquidity. And while we appreciate S&P's decision to include crypto-collateralized stablecoins DAI and FRAX alongside the graded fiat-backed stablecoins, grouping all of these products together under the same framework abstracts the different primary use cases of these stablecoins (e.g., payments, DeFi, trading, debt, yield, etc.) - all of which deserve different rating frameworks. In our view, given the short yet incident-filled histories of stablecoins, it would not be prudent for S&P to grade USDC or any other stablecoin as a 2 (strong) as it currently stands today.

Aside from these reasons, S&P's primary expertise in rating corporate bonds and sovereign debt to inform investor decisions does not directly translate to stablecoins since none of the graded products are inherently yield-bearing debt instruments. Also, recall that the credit rating agencies had improperly rated many debt instruments as AAA-rated and investment-grade during the Great Financial Crisis and many criticize credit rating agencies for conflicts of interest and slow re-ratings in response to new developments – flaws that would not fit with the rapidly evolving, transparent nature of crypto markets. S&P's assessment framework can serve as a starting point, but there are many improvements needed to better understand and represent the risks for all future prospective users of stablecoins. – Charles Yu

Ethereum Devs Carve Out Timeline for Cancun/Deneb Testnet Upgrades

On Thursday, December 21, Ethereum core developers agreed on a tentative timeline for the activation of the Cancun/Deneb upgrade on public testnets. Developers plan on upgrading three public testnets before activating the upgrade on Ethereum mainnet. The tentative dates for Cancun/Deneb testnet upgrades are as follows:

Goerli fork on January 17

Sepolia fork on January 31

Holesky fork on February 7

The above timeline is subject to change as developers may need to push back these dates in the event of unexpected bugs in code. As indicated by Ansgar Dietrichs, one of the developers on Thursday’s All Core Developers (ACD) call, there is a sense of urgency to ship the Cancun/Deneb upgrade as soon as possible for the cost-savings that it would bring to Layer-2 rollups (L2s). For this reason, developers are planning on bundling client releases for both Sepolia and Holesky hard forks in one single release such that node operators on both networks only have to upgrade their machines once and the turnaround time between these two hard forks can be shorter, one week instead of two.

For more information about the main code change being implemented in Cancun/Deneb, proto-danksharding, read this Galaxy Research report. For the full call summary from Thursday, read this Galaxy Research writeup.

OUR TAKE:

The timeline for Ethereum testnet upgrades shared on this Thursday’s ACD call is ambitious and will likely be delayed by a few weeks. Prysm, which is the most popular consensus layer (CL) client run by Ethereum node operators, has yet to resolve all bugs in their latest client release. If the Prysm client is not ready with an updated release by January 8 or 9, developers will have push back the date for the Goerli hard fork. Among the three sets of public testnet upgrades, the Goerli fork is likely to be the most informative for developers and may highlight additional concerns about the Cancun/Deneb upgrade that causes developers to delay the Sepolia and Holesky forks and/or decouple them. For these reasons, a mainnet activation for the Cancun/Deneb upgrade sometime in March 2024 still appears likely.

Looking ahead to the mainnet activation for Cancun/Deneb, it is unlikely that the changes introduced to the network will benefit the value of ETH in the short-term as the main code change in the upgrade, proto-danksharding, reduces fee revenue to Ethereum from L2s. Though adoption for L2s is expected to increase the value of Ethereum block space in the long run, technical challenges in the near-term to L2 decentralization, security, interoperability, and user experience is likely to hinder the migration of end-users on Ethereum to L2s. Without meaningful adoption for L2s in the months leading up to and following the Cancun/Deneb upgrade, Ethereum will continue to face scalability issues, fee volatility, and increased competition from alternative Layer-1 blockchains such as Solana and Celestia. For more information about the impact of the Cancun/Deneb upgrade on the value of ETH, read this Galaxy Research report. - Christine Kim

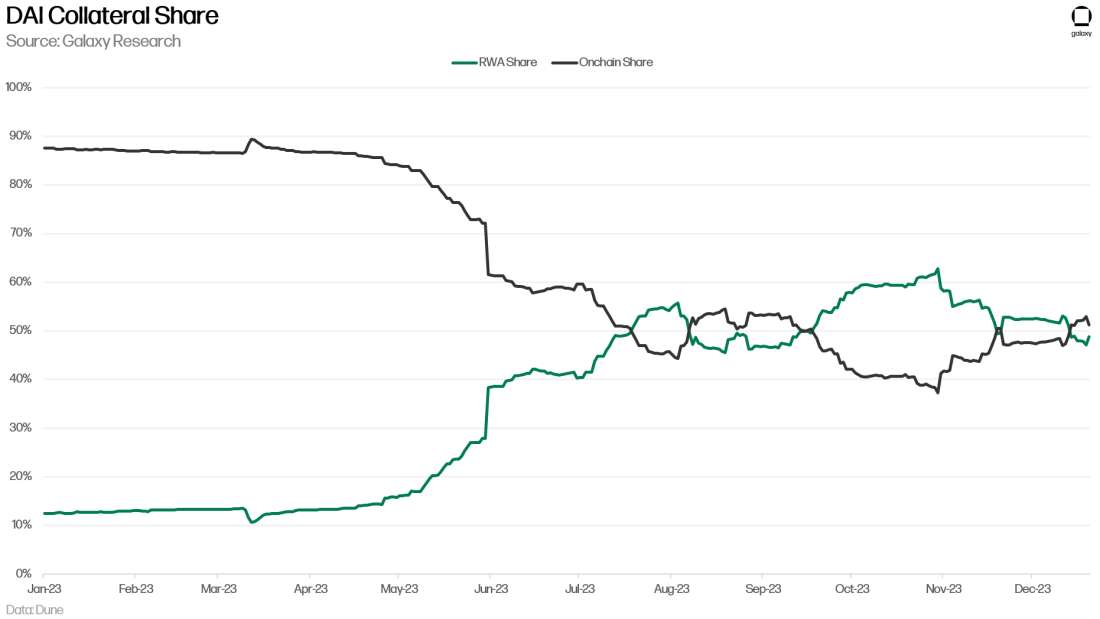

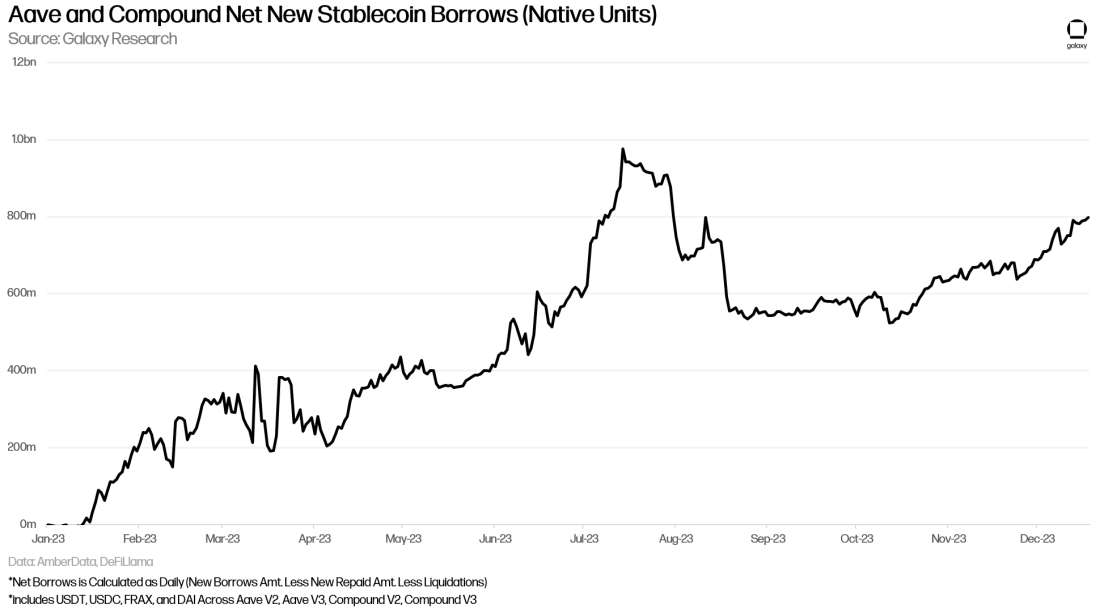

Charts of the Week

Real world assets (RWAs) and onchain assets are fighting for a majority share of DAI collateral. RWA collateral primarily includes offchain private credit and U.S. Treasury securities and related strategies; and onchain assets primarily include ETH, WBTC, stablecoins, liquidity provision (LP) tokens, and DAI issued through lending protocols. On December 15, 2023, onchain assets became the more popular collateral source for DAI and back 51.2% of supply as of December 21, 2023.

The growing onchain share is the result of an increasing number of DAI being collateralized by onchain assets, and not because the number of DAI collateralized by RWAs is decreasing. This is an important distinction because it highlights that the growing onchain share is partially the result of users depositing more onchain assets to mint DAI; and not solely from DAI collateralized by RWAs being taken out of circulation.

RWAs are at a pivotal moment with the Fed signaling for rate cuts and demand for cryptocurrencies gaining steam. As users have been coming back onchain demand for stablecoin liquidity has been rising. This is apparent in Aave and Compound stablecoin markets, which have seen 800m native units’ worth of new stablecoin loans in 2023. This trend accelerating can push a growing share of DAI collateral into onchain sources and away from RWAs as users demand liquidity against their onchain assets.

Other News

BVI court freezes Three Arrows Capital founders’ $1 billion in assets

Phantom adds support for Bitcoin, Ordinals and BRC-20 tokens

Ledger to change transaction signing process after exploit, promises to return funds

China pledges to boost NFT, decentralized application development despite crypto trading ban

Avalanche users pay $13.8 million in fees for inscriptions over 5 days

MilkyWay rolls out Celestia liquid staking protocol on Osmosis

OKX NFT marketplace volume surpasses Blur, OpenSea amid Bitcoin Ordinals frenzy

Ordinals-based Tap Protocol raises $4.2 million to develop on Bitcoin

From the Desk of Galaxy Digital Research

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2023. All rights reserved.