Top Stories of the Week - 11/24

This week in the newsletter, we write about Binance, Argentina, and CoinDesk’s acquisition.

Subscribe here and receive Galaxy's Weekly Top Stories, and more, directly to your inbox.

Binance Settles with DOJ, Treasury, and CFTC; CZ to Step Down as CEO

On Tuesday, the Department of Justice, Treasury Department, and Commodities Futures Trading Commission announced a settlement of charges against Binance and its CEO, Chanpeng Zhao (CZ). Binance, the entity, pleaded guilty to felony charges for willfully violating the Bank Secrecy Act, knowingly failing to register as a money transmitting business, and willfully violating the International Emergency Economic Powers Act. Binance must pay $4.3 billion in fines as part of the settlement, review past transactions and report suspicious activity to federal authorities, and also provide Treasury access to its systems and records for five years as part of an ongoing monitoring regime. As part of the settlement, CZ also pleaded guilty to a felony charge for willfully violating the Bank Secrecy Act and stepped down as Binance’s CEO. CZ appeared in the United States District Court for the Western District of Washington on Tuesday to enter his plea. According to Bloomberg, CZ faces a maximum of 10 years in prison and up to $500,000 in fines in addition to profits earned.

Rumors of the settlement first emerged on Monday from Bloomberg, which reported that the U.S. Justice Department was seeking more than $4 billion in fines and some jail time for CZ to settle charges for money laundering, bank fraud, and sanctions violations. On Tuesday morning, crypto news aggregator Tier10k tweeted, "DOJ to announce significant action at 3 PM ET," with additional reporting highlighting that Treasury Secretary Yellen, Attorney General Garland, Assistant Attorney General Monaco, and CFTC Chair Benham would all be present.

In a post made on X immediately after the press conference began, CZ announced he had stepped down as CEO and would be replaced by Richard Teng, who previously oversaw Binance’s markets outside the US. Prior to that Teng served as Binance's CEO in Singapore and he also has prior experience working as a financial regulator in Abu Dhabi. There had been speculation that he would succeed CZ for months prior to the announcement. Teng also posted on X, saying that his focus would be reassuring “Binance’s 150m users,” collaborating with regulators, and driving adoption of Web3. CZ also highlighted that the settlement with the US included no allegation that Binance misappropriated any user funds nor engaged in any market manipulation.

Binance has suffered a number of regulatory setbacks over the past year. US operations were shuttered in June, and in October, Binance stopped accepting new customers in the UK. In Europe, Binance halted operations in Belgium, failed to obtain a license to operate in the Netherlands, and withdrew applications for licenses in Austria and Germany. At least 16 executives have departed, including the head of its US and UK operations. The company is also dealing with a variety of regulatory issues in countries like France, Brazil, Canada, and Japan. Even in the wake of the the settlement today, Binance still faces outstanding civil charges filed by the SEC in June for offering unregistered securities and commingling customer funds.

OUR TAKE:

A settlement of longstanding charges against Binance resolves one of the largest remaining regulatory overhangs in crypto.

After launching in 2017, Binance quickly rose to prominence, becoming the largest crypto exchange by market share in 2018. That dominance has faded over the past year, falling to just below 50% in October after reaching as high as 74% in December 2022. Continuous regulatory woes coupled with a more competitive exchange market have hampered the exchange's growth. Competitors like OKX, Bybit, and Bitget have picked up market share abroad while Coinbase has benefitted from Binance’s departure from the US. Additionally, new regulatory-friendly exchanges like Backpack and Cube are launching, hoping to fill the void FTX left for many emerging markets.

More marketplaces, especially more compliant and transparent ones, are needed for this industry to grow. They remove centralization risks, increase competition/lower costs for consumers, and expand consumer access to crypto. They also help reduce risks for institutions eager to participate in the space but unable to do so due to uncertain regulatory environments.

Repeatedly throughout their remarks and in the ensuing Q&A, officials made a point to warn crypto companies that failure to follow US laws, as was the case with Binance, will result in prosecution. Binance's facilitation of payments for terrorist financing and darknet websites, among other charges, are clear violations of US law.

While US Attorney General Merrick Garland said that the action demonstrated their “whole of government approach,” one government entity was conspicuously absent: the Securities & Exchange Commission. Chair Gensler’s absence from a dais that included the Secretary of the Treasury, the Attorney General, and the Chair of sister-regulator CFTC suggests some internal divergence between the SEC and the other regulators, or at least some lack of coordination. Indeed, the SEC announced a new civil suit against cryptocurrency exchange Kraken just the day before. While this settlement with Binance highlights the government’s clear focus on AML/KYC compliance and preventing illicit finance, the SEC remains focused on forcing cryptocurrency issuers and exchanges into the existing securities law frameworks something Coinbase is vigorously opposing in court and which Kraken is signaling it will also fight. (Note, while the CFTC settled its case with Binance, the SEC’s case against Binance.US continues). If it wasn’t already, it is now abundantly clear that these are the two primary regulatory vectors in the US: issues relating to the securities laws, and issues relating to AML/KYC and illicit finance. – Lucas Tcheyan

Argentinians vote for bold economic reform

Argentina elects Bitcoin-aligned Javier Milei as next president. On November 19, libertarian Javier Milei won the Argentinian presidential election by a wider-than-expected margin as he secured 56% of the vote, nearly 2.8m votes ahead of his opponent Sergio Massa. The president-elect is set to take office on December 10. In his victory speech, Milei acknowledged the economic challenges that his country faces including "inflation, lack of work, and poverty," adding that "the situation is critical and there is no place for tepid half-measures."

Milei, a proponent of the Austrian school of economics, campaigned on making radical economic changes including abolishing the country's central bank and moving from the Argentine peso as the national currency to the US dollar as a fix to the country's long-standing inflationary challenges. Milei has also advocated for steep public spending cuts and privatizing state-owned companies like oil company YPF as he aims to lower the budget deficit and build up reserves. Milei also sees Bitcoin as a monetary tool to combat harmful hyperinflationary Central Bank policy, though he has not explicitly advocated for Argentina to adopt Bitcoin as legal tender or to hold BTC as a reserve asset.

In addition to the difficulty of addressing economic challenges that have plagued Argentina for decades, Milei will likely face pushback to some of his plans from a divided Congress – his Liberty Advances block only holds 7 out of 72 seats in the Senate and just 38 out of 257 seats in the lower Chamber of Deputies. Still, Argentinian markets have reacted positively since re-opening after Milei's election win – the local S&P Merval stock index was up 23% on Tuesday, led by a 39% increase in YPF shares, while bond markets also rallied. The official exchange rate for the Argentine peso held at ~356 per USD as it is maintained by capital controls, but the unofficial black market peso slid on dollarization concerns to 1,045 per USD, implying a 66% devaluation to the local currency.

OUR TAKE:

The Argentinian people have spoken: they have grown weary of decades of economic and financial mismanagement and want bold economic reform. More than two in five Argentinians currently live in poverty. The country's economy has battled hyperinflation for decades as they've financed deficit spending with money printing. Argentina's annual inflation estimates topped 140% in October as the Central Bank of Argentina increased the benchmark policy rate by 15-ppt to 133% (nearly 4x the level since the start of 2022 when it was at 38%). With these poor economic conditions driving declining trust in institutions, it makes sense that the general population would be more receptive to an alternative financial system.

Even though Milei has not explicitly stated any plans to join El Salvador in adopting Bitcoin as legal tender, his economic vision closely aligns with the ideology of Bitcoin as a monetary system outside the corruption of banks and governments. Milei's plans to cut spending and to dollarize the economy should help in reducing the deficit and in slowing inflation in the long-term, though it's still unclear whether Milei can deliver on all of his promises given the political roadblocks in front of him. Any economic fixes are unlikely to be quick or easy and Argentinian markets will likely face short-term volatility. But if Milei does find support from legislators to implement his stabilization plan AND it proves successful in solving Argentina's economic woes over a longer period, then he can possibly accelerate the global adoption of crypto in politics and society.

Crypto is a social and political revolution just as much as it is a monetary revolution and the first step to its adoption is replacing failing old-world institutions and points of control. Argentina is just one of many economies dealing with runaway inflation and a growing population of disenfranchised citizens. In the coming years, we expect to see crypto play a larger role in elections as more people start to recognize the economic opportunities and social benefits of the new financial paradigm. - Charles Yu

Crypto Exchange Bullish Acquires CoinDesk

Cayman Islands-based cryptocurrency exchange Bullish has bought CoinDesk, one of the oldest and most prolific crypto-focused media companies. CoinDesk was founded in 2013 by entrepreneur and angel investor Shakil Khan. In 2016, Khan sold CoinDesk for $500,000 to crypto venture capital firm Digital Currency Group (DCG). At the time, CoinDesk was still a relatively small company, with 10 full time employees and roughly 700,000 monthly readers. However, as interest and adoption for cryptocurrencies and blockchain technology grew, so too did CoinDesk’s readership and audience.

Axios reports that CoinDesk’s revenue grew tenfold from 2016 to 2018. At present, CoinDesk boasts 5.7 million average monthly viewers and a team of over 50 crypto journalists. CoinDesk’s journalists have received major awards for their work covering the crypto industry. This year, they won the prestigious Gerald Loeb Award and the George Polk Award for their coverage of FTX and breaking the scoop on the hole in FTX’s balance sheet in November 2022. CoinDesk has also expanded its business over the years beyond news reporting to also support events, podcasts, newsletters, TV & video, as well as indices and research.

DCG was reportedly close to closing a deal for the sale of CoinDesk to crypto investment firm Tally Capital back in July 2023 for a price tag of $125 million. The financial terms of the acquisition of CoinDesk by Bullish, announced on Monday, were not disclosed. However, the press release did state that CoinDesk will continue to operate under the same management team and as an independent subsidiary of Bullish. The press release also stated that CoinDesk has appointed Matt Murray, former Editor-in-Chief of the Wall Street Journal, as the Chair of a new editorial committee overseeing CoinDesk and its journalistic independence under a new owner.

Bullish is headed by former New York Stock Exchange President Tom Farley. Bullish is itself a subsidiary of Block.one, the company that created EOS and led one of the largest initial coin offerings of all time. Launched in 2021, Bullish operates in over 50 jurisdictions, excluding the U.S., Canada, China, Japan, Israel, and Russia.

<strong>OUR TAKE: </strong>

One of crypto’s most reputable and longstanding media companies has secured a new buyer to support its growing business. The future of CoinDesk was unclear ever since its previous owner, DCG, became encumbered with the fallout from FTX’s collapse, impacting DCG itself as well as its subsidiaries. The unclear runway for CoinDesk leading up to its acquisition motivated several layoffs at CoinDesk, the most recent of which led to a 45% reduction of CoinDesk’s editorial staff. Monday’s announcement is welcome news affirming that CoinDesk will continue to do what it does best, produce award-winning crypto news, education, and data as an independent subsidiary of Bullish.

However, Monday’s news was not taken positively by all. The founder of crypto media site Blockworks Jason Yanowitz said the news was “bad for our industry” because the acquisition “crushes the editorial integrity of the [CoinDesk] brand.” This type of criticism and skepticism over CoinDesk’s editorial integrity is nothing new and, frankly, based on the quality of news reporting by CoinDesk journalists, appears ill-founded. Since 2016, critics of CoinDesk have voiced the same concerns of conflicts of interest due to their ownership by DCG. However, DCG’s ownership of CoinDesk has not hindered the organization’s transparent coverage of DCG subsidiaries or business interests, even if at times the coverage required revealing internal debates between CoinDesk and DCG itself. Having operated under one of crypto’s most prolific conglomerates for seven years, CoinDesk appears to be well-versed in navigating conflicts of interest due to its ownership. The establishment of a new editorial committee under the new ownership of Bullish also highlights continued commitment by CoinDesk’s leadership and editorial staff to operate independently from the business interests of its new owner.

Nevertheless, it will be important to closely monitor CoinDesk’s coverage of the crypto industry in the months and years ahead. Though the ownership of Bullish is unlikely to sully the editorial integrity of CoinDesk over time, the ownership of CoinDesk by a company whose business and revenues continue to be impacted by the volatility of the crypto markets does mean that CoinDesk’s future, though secure now, could change again. As mainstream media companies like the New York Times, Bloomberg, and the Wall Street Journal grow their crypto coverage as the industry grows, a stable source of funding for CoinDesk would help the media business compete against larger competitors and dedicate resources towards long-term growth. – Christine Kim

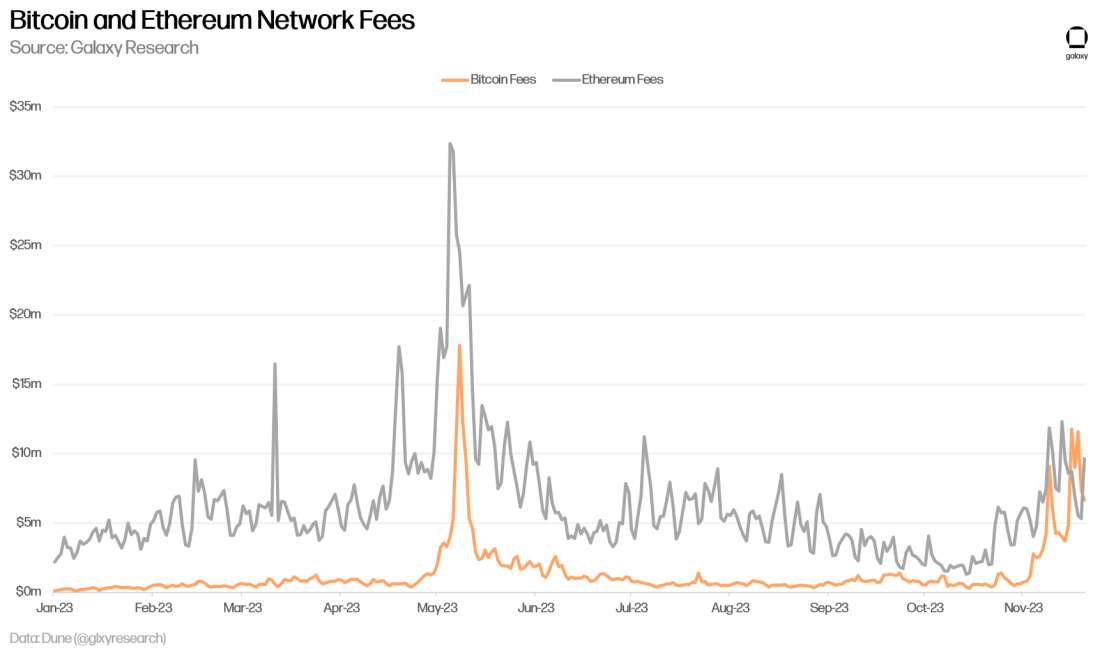

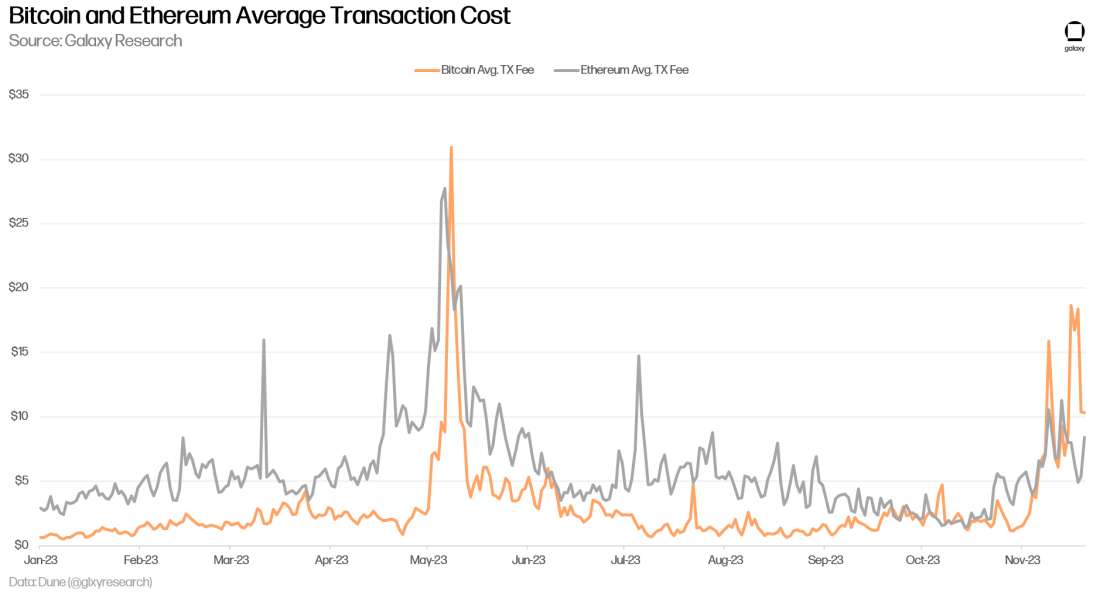

Charts of the Week

Bitcoin daily fee revenue exceeded that of Ethereum for the first time in more than 1,060 days on November 16. The last time this occurred was December 18, 2020. November 16 through November 19 marked the longest daily streak where Bitcoin generated more fees than Ethereum since November 10, 2020.

The growth in fee revenue was bolstered by 6-month highs in average transaction costs. Bitcoin’s average network fee reached $18.68 on November 16. Fees have since cooled off and average $10.35 as of November 20.

Other News

Ethereum Layer 2 Kinto migrates to the Arbitrum ecosystem

SEC files new lawsuit against Kraken for allegedly operating online trading platform without registering

Tether freezes $225 million worth of stolen USDT after DOJ investigation

Blur founder's Ethereum Layer 2 Blast goes live

A DAO is funding a lawsuit against its own founding team

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2023. All rights reserved.