Bitcoin Holders Undeterred Amid Short-Term Leverage Wipeout

Introduction

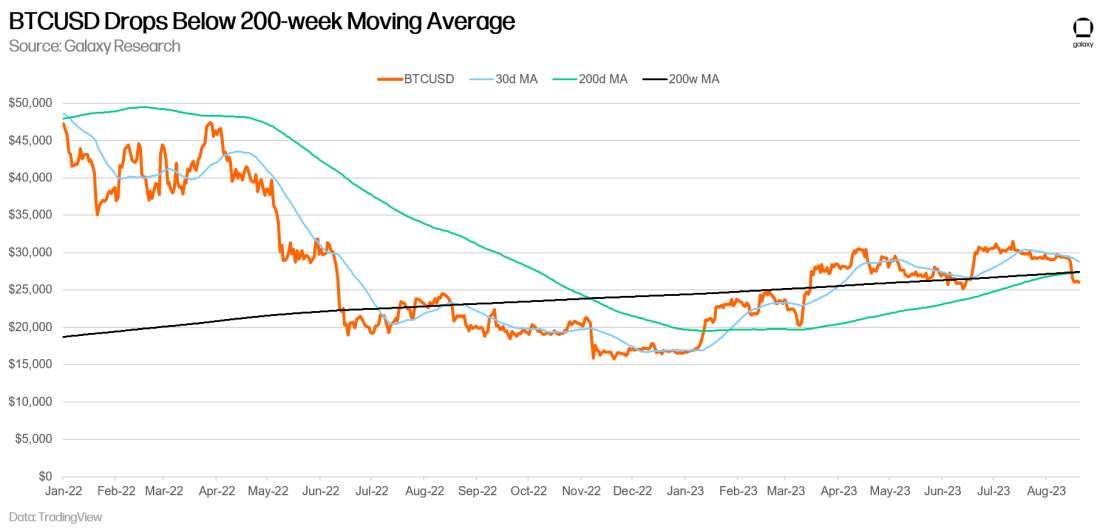

On Thursday, August 17, Bitcoin experienced a major deleveraging event that saw BTCUSD drop more than 10% in a 2-hour period. The downward move awakened BTC out of a low volatility period of historic levels.

Key Takeways

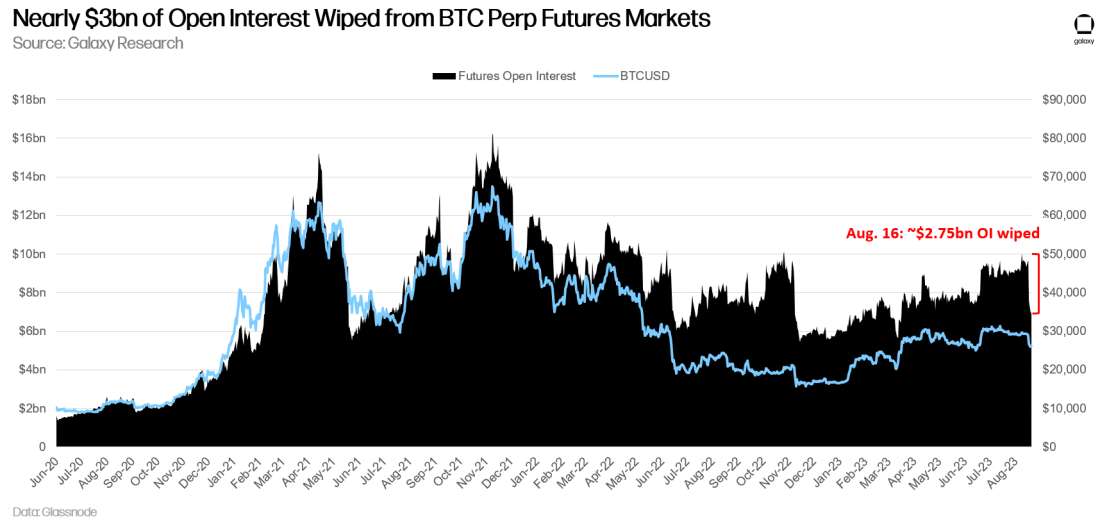

Futures open interest declined by the most since the collapse of FTX in Nov. 2022, wiping out more than $2.75bn of open interest on Bitcoin futures markets

Short term holders are sitting on significant unrealized losses which could lead to further downside movement in the near term

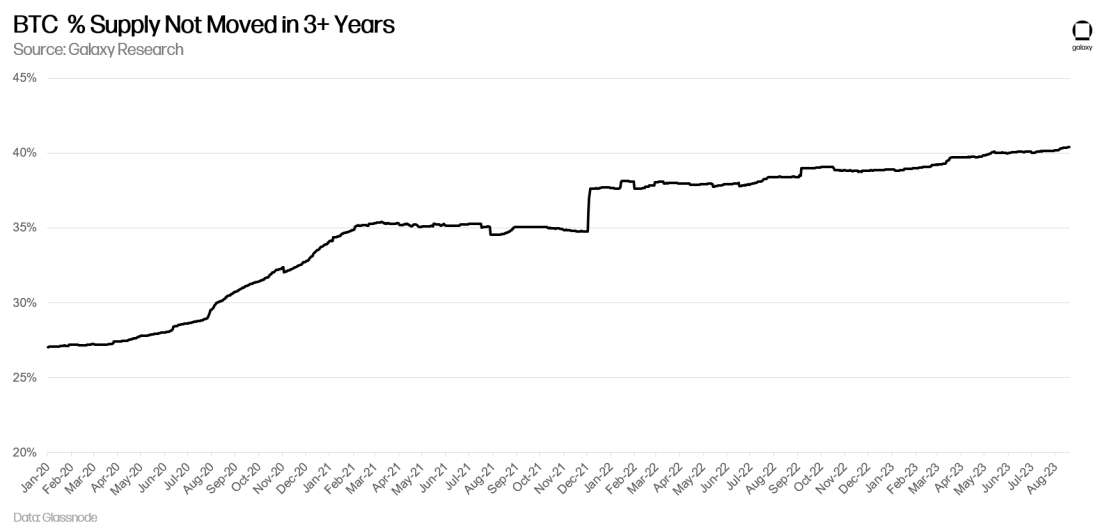

Long-term holders continue to accumulate, with more than 40% of BTC supply on-chain for 3+ years, an all-time high for that metric

Smaller holders (<=10 BTC) continue to accumulate, but not yet at levels seen during other price dips in 2023

$25k is key level to watch based on technical and onchain fundamental indicators

Anatomy of a Crash

Bitcoin experienced a significant repricing on Thursday Aug. 17, dropping ~10% in the hours between 4pm and 6pm ET.

The move sent BTCUSD below its 200-day and 200-week moving averages.

Open interest on perpetual futures markets dropped by about $2.75bn during and following the event. This was the largest single BTC deleveraging event since the collapse of FTX in early November 2022, with long liquidations resulting in forced selling as amplification for the move lower.

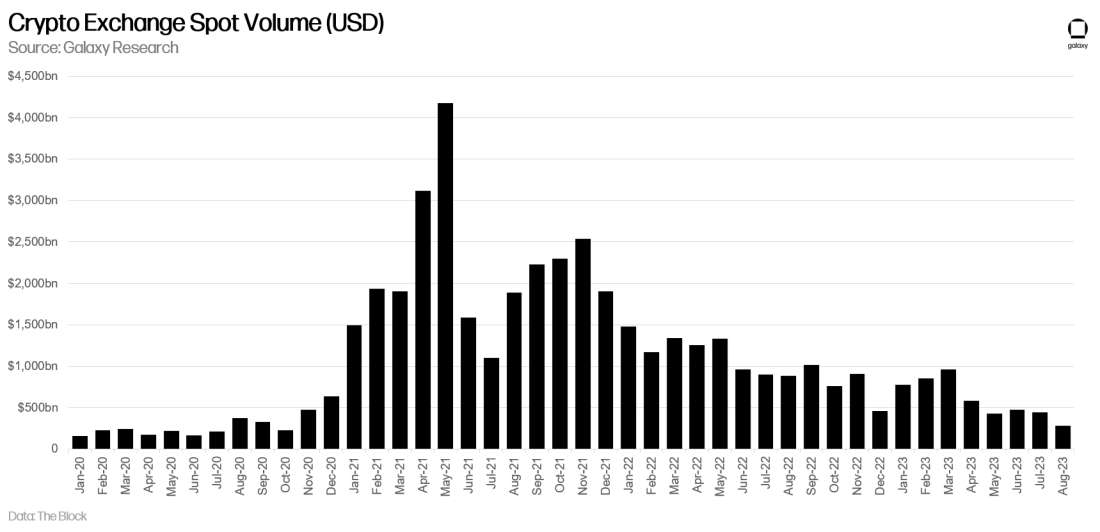

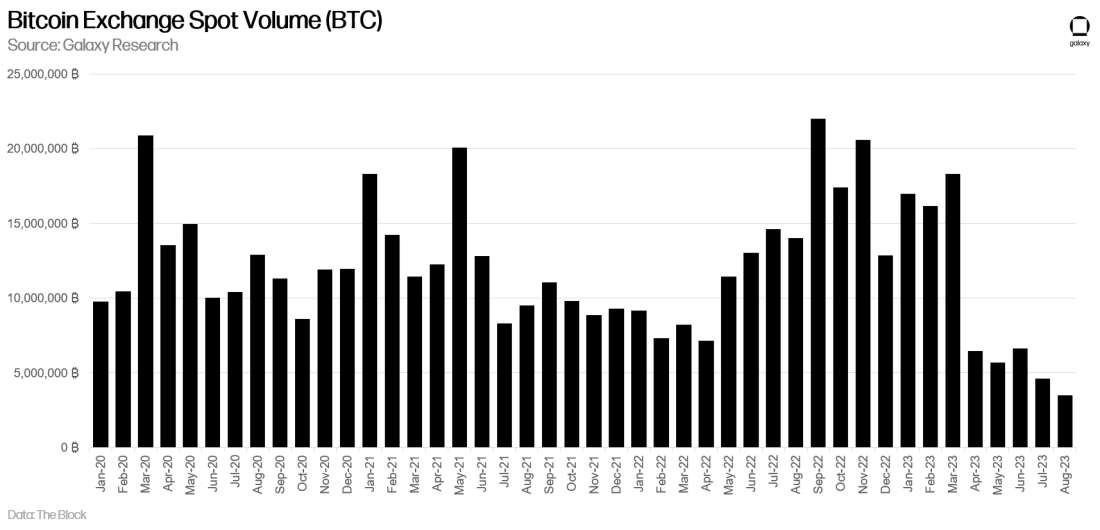

The move was exacerbated by low volume on exchanges. Across all coins and major exchanges, dollar-denominated monthly trading volumes are at their lowest point since October 2020, right before the start of the last bull cycle.

Looking at bitcoin volumes on exchanges denominated in BTC, the recent low volatility environment has sent monthly BTC trading volume to its lowest level in at least 2.5 years. Indeed, since the elevated volumes in March following the collapse of Silicon Valley Bank, bitcoin exchange volume has consistently declined month-over-month (with a minor exception of June when BlackRock announced its ETF filing).

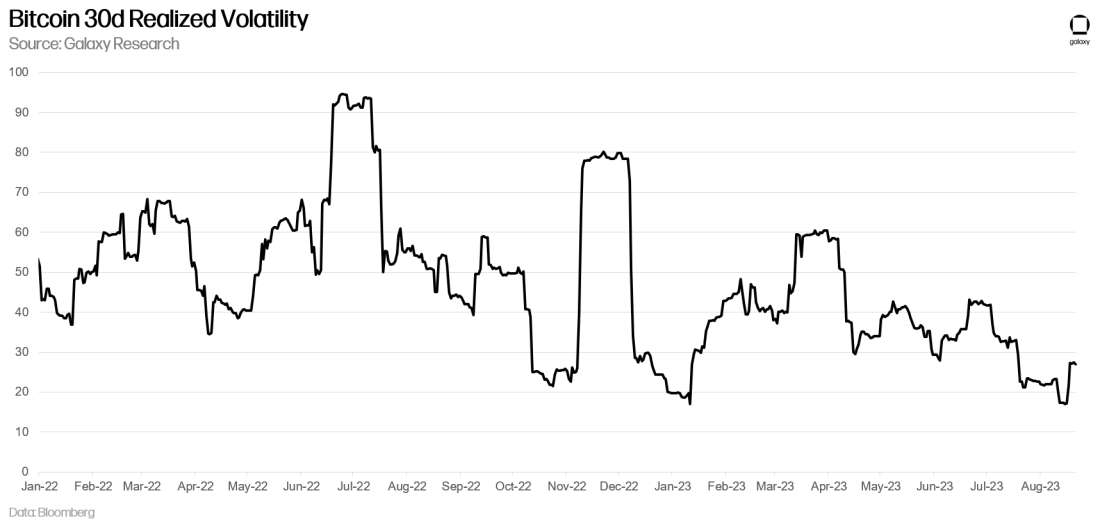

Realized volatility has ticked up slightly on a 30d basis, though Bitcoin remains in a depressed volatility environment relative to historical norms.

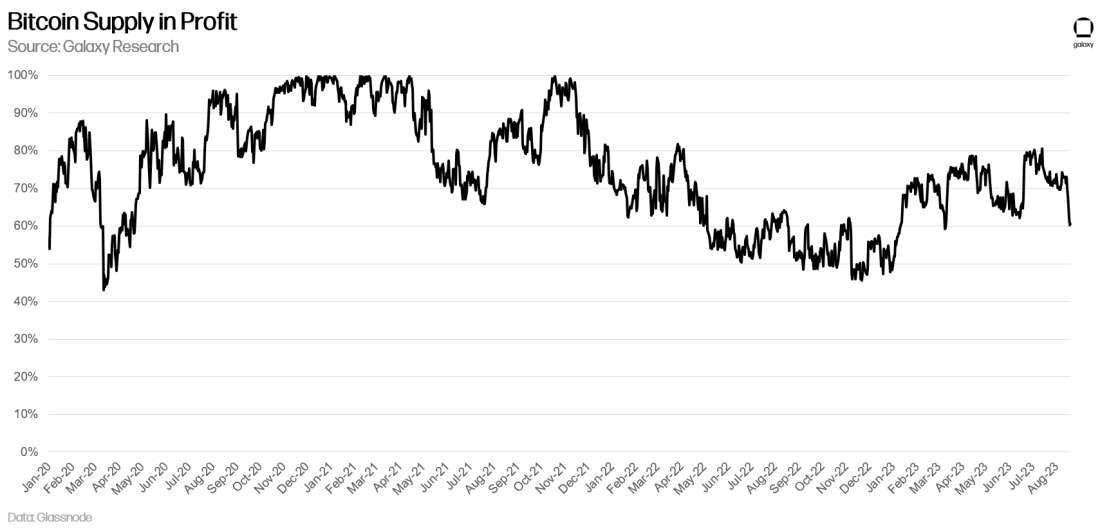

Looking at Bitcoin Supply

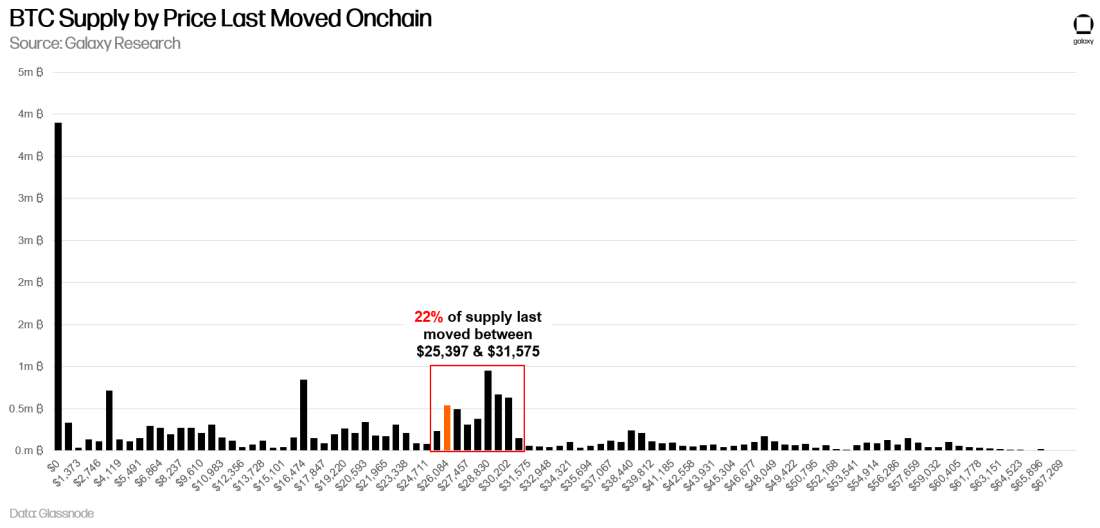

At the time of writing, BTC is trading right around $26,000. $25,000 is a key level to watch, as it has served as technical support and resistance several times as far back as May 2022, and it’s where Thursday’s flash crash found support. When looking onchain at bitcoin supply, the level also stands out. 22% of all BTC supply has changed hands between $25,300 and $31,575.

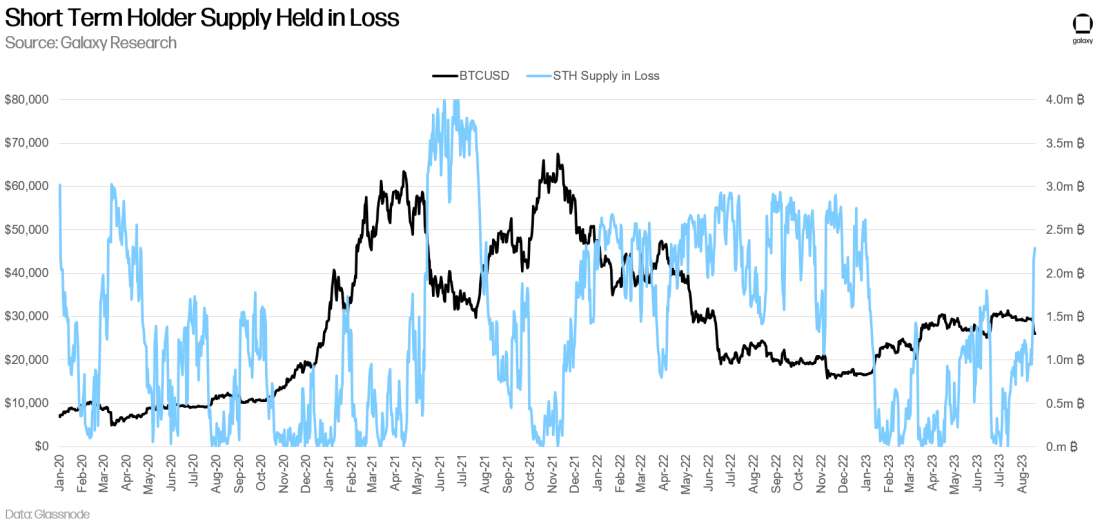

Indeed, the amount of Bitcoin supply held by short-term holders at a loss – that is, below the levels that it last moved onchain – is at its highest level since January. (Short term holders are entities who have held coins for fewer than 155 days).

Still, more than 60% of Bitcoin’s supply is “in profit” onchain – meaning it last moved onchain at a price that was lower than today’s price.

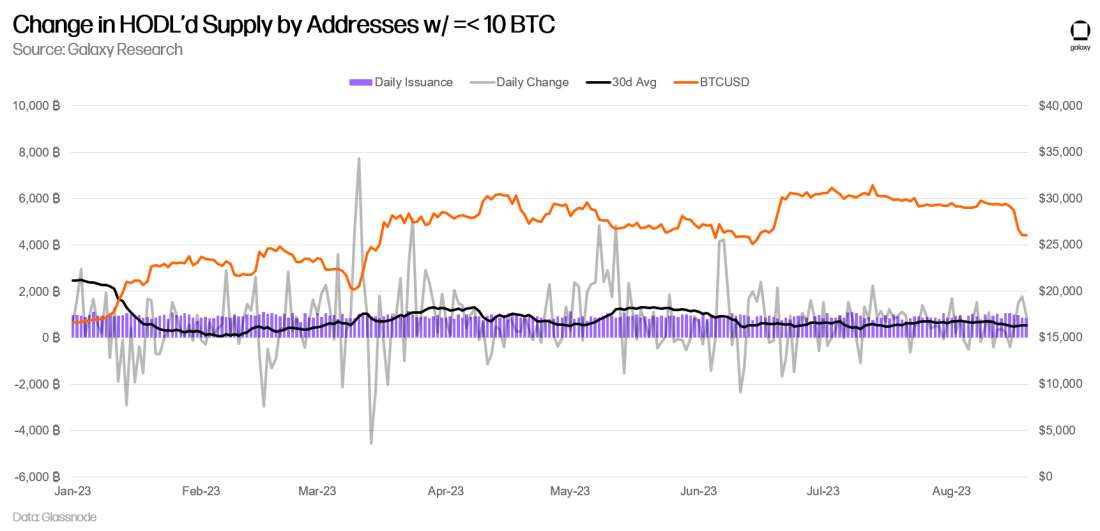

Holders Still Stacking

Following the August 17 event, small addresses were seen adding to their bitcoin holdings. Bitcoin emits ~900 newly minted BTC per day, and addresses with balances equal or less than 10 BTC were seen onchain accumulating above that level in the days since Thursday. On a 30d rolling basis, this cohort has tended to accumulate during times of stress, with big spikes during the collapse of Silicon Valley Bank and during the dip to $25k seen in early June.

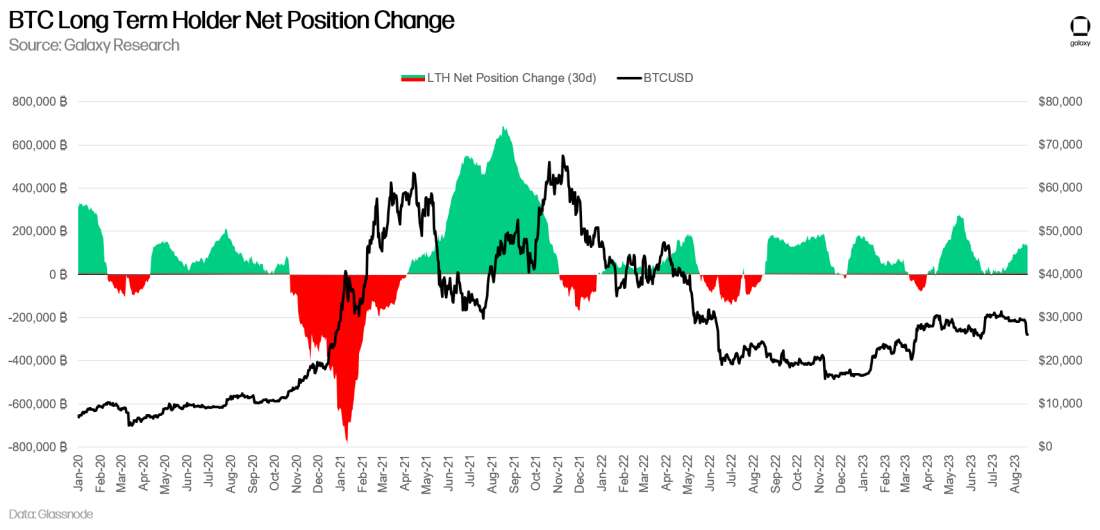

Long-term holders have been net accumulating (on a rolling 30d basis) since March.

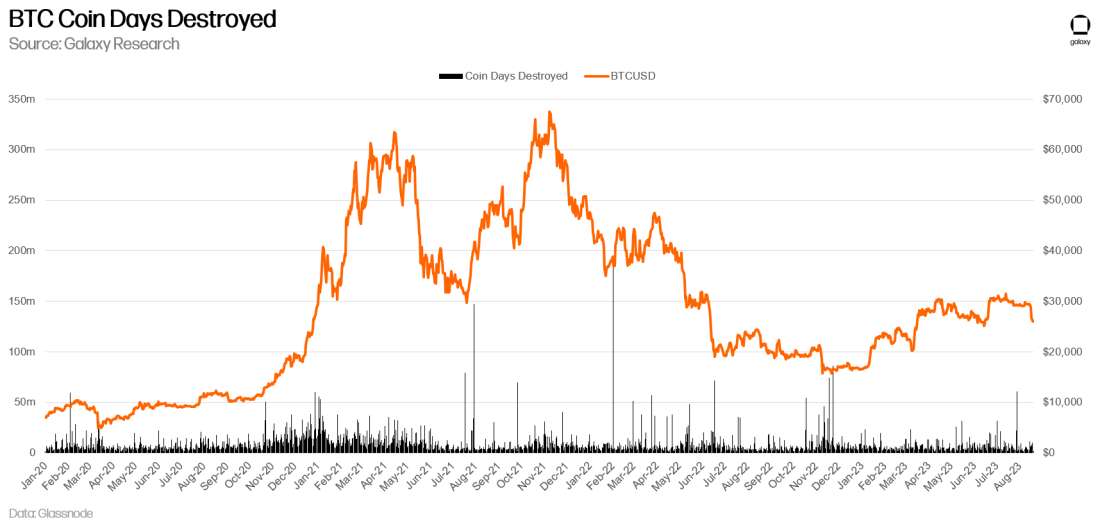

Since the deleveraging, there has also not been a significant amount of Coin Days Destroyed, indicating very few old coins coming online and moving onchain – a further sign that long-term holders are not exiting long-held positions.

Finally, the percentage of Bitcoin’s supply that hasn’t moved in 3+ years is making new all-time highs at over 40%. Long-term holders continue to accumulate and hold for longer.

Catalysts for the Rest of 2023

Looking ahead to the rest of 2023, there are relatively few known catalysts, but they mostly fall into a few buckets: court cases, legislation, and macro.

Court cases. Market observers generally view the impending ruling in Grayscale vs. SEC as the most imminent potential catalyst. In that case, Grayscale is seeking review of the SEC’s 2022 denial of GBTC’s conversion to an ETF, with court watchers mostly expecting a win for Grayscale due to the judges’ reception to the SEC’s case during oral arguments in March. A win for Grayscale is unlikely to result in the approval of GBTC’s conversion to an ETF, but could require the SEC to reconsider Grayscale’s application. Rulings on motions to dismiss in the SEC’s case against Coinbase and developments in a variety of cases against Binance could also move the market.

Legislation. The US House is currently considering bills that would formalize rules for both crypto market structure and stablecoin issuance. Crypto markets are likely to respond positively if these bills pass the house with sufficient support to force Senate action.

Macro conditions. A further breakdown in the bond markets would enforce a headwind for risk assets, including Bitcoin, as could further rate increases from global central banks. However, certain macro outcomes, such as further problems in the banking system or downgrades from ratings agencies, could provide tailwinds for Bitcoin as they did in March following the collapse of Silicon Valley Bank. Lastly, were global central banks to signal an end to rate hikes, or even the beginning of an easing cycle, Bitcoin could see improved performance.

These catalysts are likely to result in heightened volatility as we enter a more active Fall trading environment.

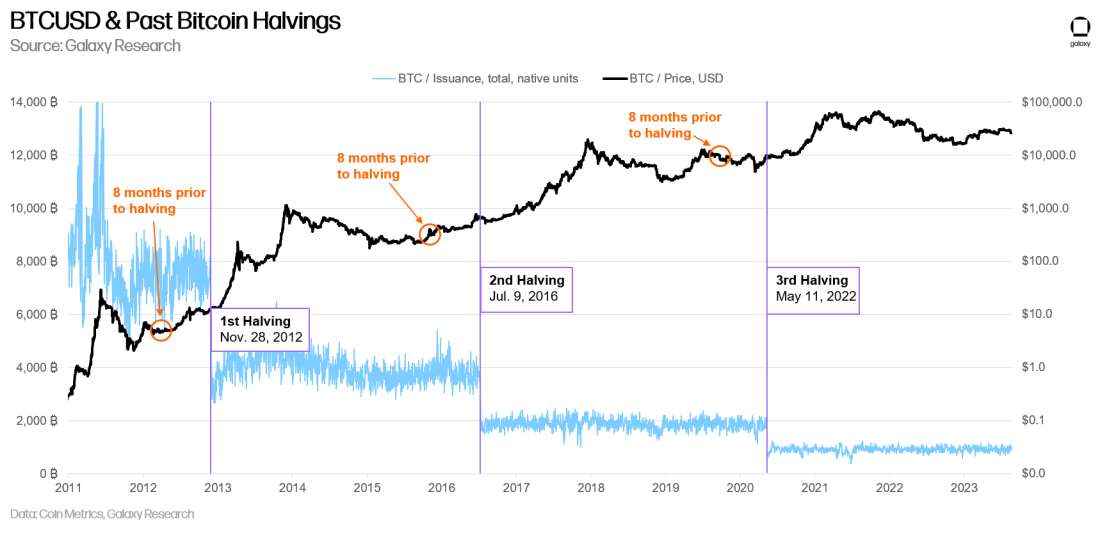

Bitcoin observers are also beginning to anticipate the network’s 4th halving, the quadrennial event when Bitcoin’s new issuance halves, expected sometime in April 2024, approximately 8 months from now. Each of the first two halvings saw the beginning of a bull market around 8 months prior to the halving event. The months leading into the third halving were a bit more ambivalent for bitcoin price, and then the shock of the March 12, 2020 COVID crash reset any momentum gained. Regardless, bitcoin halving events, though their absolute impact on supply dynamics has reduced over time (and is objectively low at this point), have historically led to rejuvenated interest in bitcoin and preceded major bull markets. Talk of the halving and its purported impact on Bitcoin markets will increase throughout the rest of the year leading into next Spring, potentially impacting positioning.

Conclusion

The quick move down liquidated significant leverage in the market, resulting in a reset not seen since the collapse of FTX. In the absence of powerful narrative catalysts, the near-term risk remains mostly to the downside, with $24k and $25k seen as key support levels that could be tested in coming weeks. The fact that nearly 90% of short-term held BTC is at a loss onchain presents additional downside risk if a recovery doesn’t happen quickly. There is little evidence that holders are concerned, with ongoing accumulation observed by both long-term holders and smaller addresses.

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2023. All rights reserved.