Bitcoin Data Shows Bullish Foundation

This note was sent to Galaxy clients and counterparties on Monday, March 20, 2023.

Bitcoin has risen dramatically since the onset of the banking crisis, up more than 45% since the closure of Silicon Valley Bank on March 10. While further gains will be boosted or impaired by macro conditions – with the Federal Reserve set to announce its latest rate decision this week –an examination of performance, on-chain, and supply-side data shows reason for continued optimism for Bitcoin bulls.

In this note, we refresh several key on-chain metrics, examine Bitcoin’s performance vs. other asset classes, and describe several upcoming catalysts that suggest the best is yet to come for the world’s largest cryptocurrency.

Key Takeaways

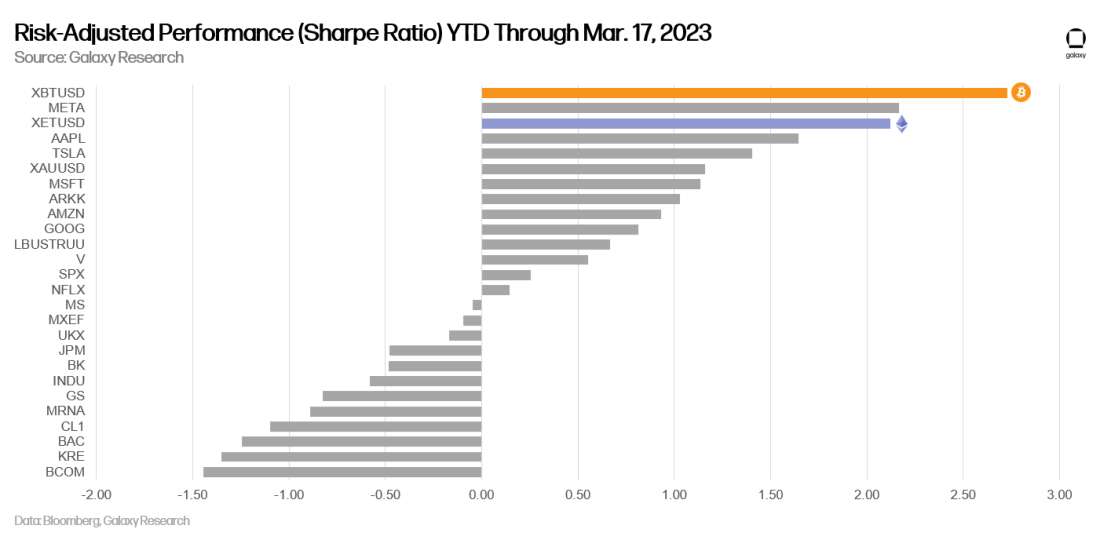

On a risk adjusted basis, Bitcoin is the best performer of the year compared to a range of securities (both equities and fixed income), indices, and commodities.

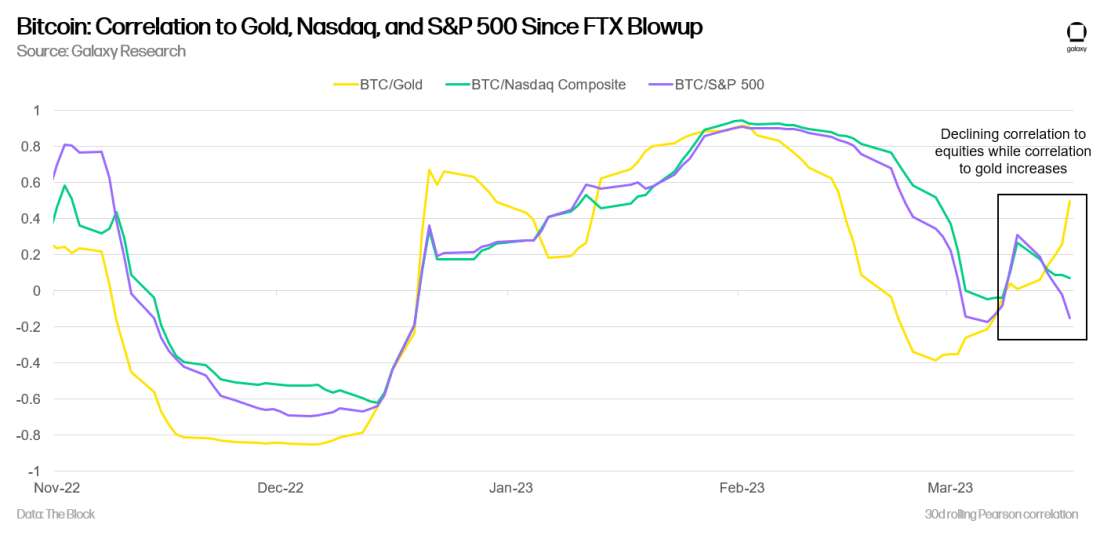

Bitcoin’s correlation to gold is increasing while its correlation to equities is decreasing, to the lowest levels in years. Bitcoin volatility continues a multi-year downward trend, although spikes of high volatility remain common.

Futures open interest and perpetual swap funding rates also suggest the rally is spot-based rather than built upon a purely speculative foundation.

On-chain data suggests ongoing accumulation, growing dispersion of ownership, and longer holding times. Certain metrics, such as SOPR and % in profit, show that holders are feeling better than they have in more than a year.

Bitcoin’s 4th halving is about 1 year away, which has typically preceded longer term bullish advances. At the same time, supply overhang fears from the pending Mt. Gox bankruptcy distributions appear, for now, to be overblown.

Exchange and miner supplies are down, and miner selling appears to have leveled off.

Bitcoin Performance

On a risk adjusted basis (Sharpe ratio), Bitcoin is the best performing asset of 2023 compared to a range of equities, fixed-income securities, indices, and commodities. Bitcoin is the best or among the best performers across a range of timeframes (except 1y), and it only looks better over longer time frames.

Correlations

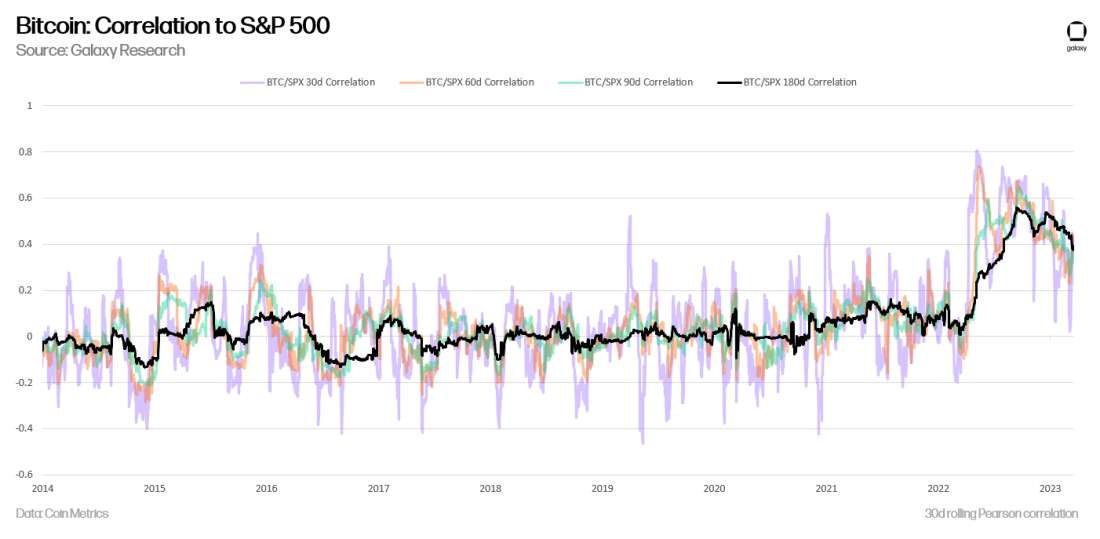

Over the last several months, Bitcoin’s correlation to equities has finally been moving lower after spending the last 18 months extremely elevated.

More recently, since the banking crisis engulfed markets, Bitcoin’s correlation to equities has declined while its correlation to gold, the classic safe haven asset, has increased sharply.

These correlation data show that, at least recently, Bitcoin has indeed performed more like a safe-haven asset than a risk asset. Given the nature of the current crisis—in which the fractional reserve banking system’s core limitations are tested—Bitcoin’s fundamental characteristics genuinely distinguish it and, when custody or self-custody is done correctly, can offer a safe port in a storm.

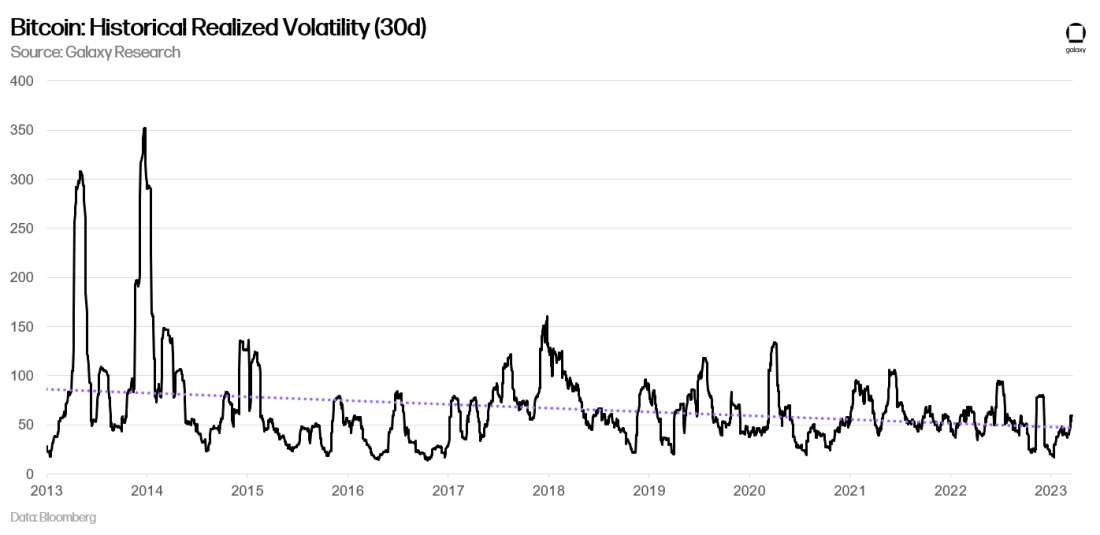

Volatility

Bitcoin remains a volatile asset, but its volatility has been slowly declining over time.

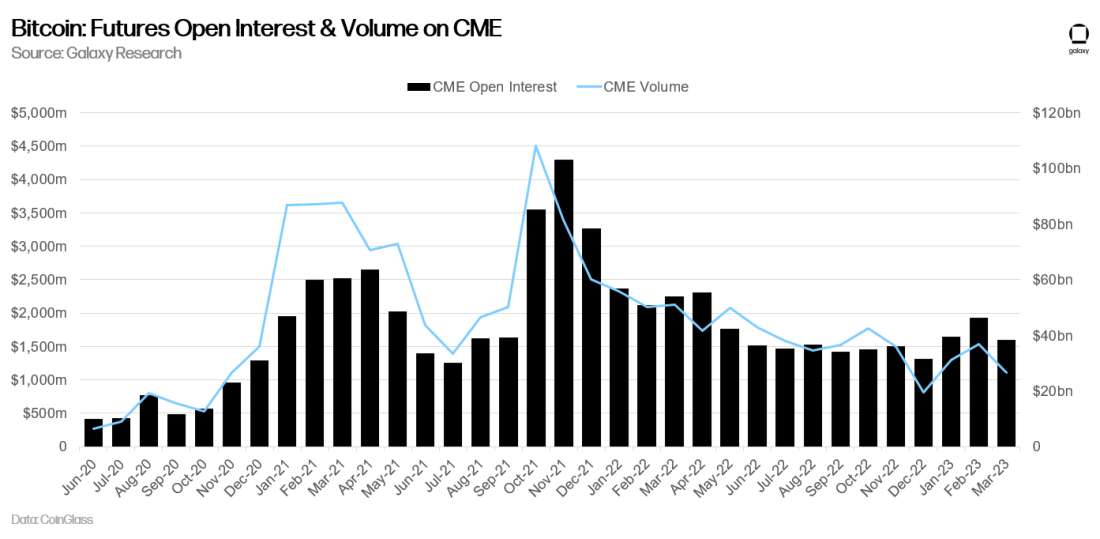

Market Dynamics

Several market indicators suggest the Bitcoin rally is driven by spot accumulation rather than levered speculation via futures. Over the course of a 60% spot rally year to date, futures funding and basis both remain flat. Aggregate open interest across futures exchanges has risen but still remains well below levels of other rallies of similar magnitudes.

Volume and open interest on the CME remains relatively flat, suggesting that those institutional investors who have been accumulating have mostly done so via spot rather than futures, or have yet to enter at all.

Perpetual swap funding has risen from negative levels but is still mostly flat, suggesting that the market is approximately net-neutral in terms of speculative positioning.

Bitcoin Supply

Thanks to the transparent nature of Bitcoin’s blockchain, we can visualize the state of its supply across a range of metrics to derive insights.

The percentage of Bitcoin’s total supply that is currently held in profit (i.e., last moved on-chain when the BTCUSD exchange rate was lower than today) is 75%, the highest since April 2022).

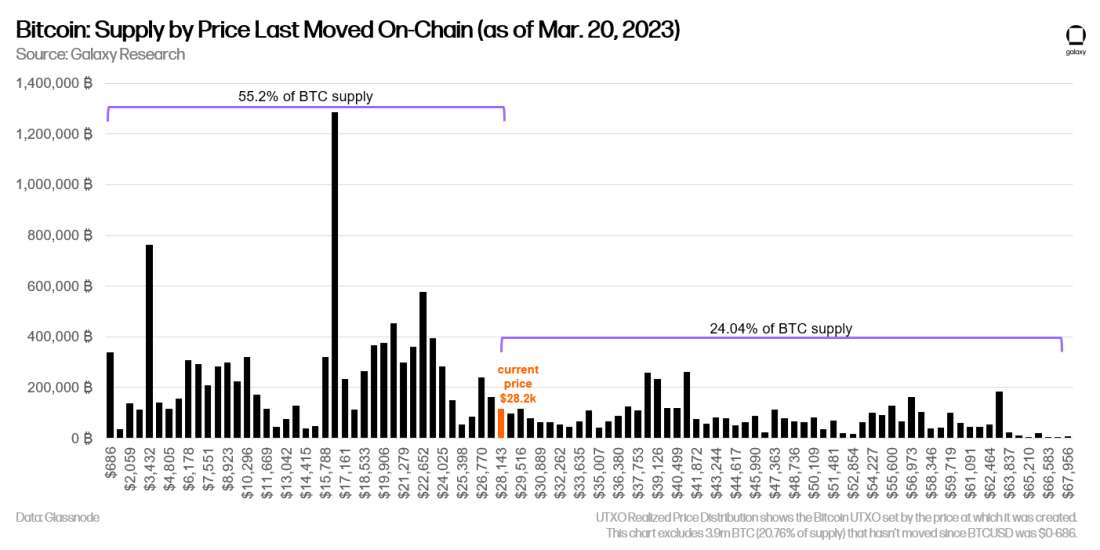

Supply in Profit

If we remove coins that haven’t moved since BTCUSD traded between $0-$686 (nearly 21% of all supply), and examine the UTXO set (current Bitcoin supply topography), we can clearly see the opportunistic accumulators from the recent bottom of $15.5-17k. A significant portion of supply was also acquired in the $18-25k range.

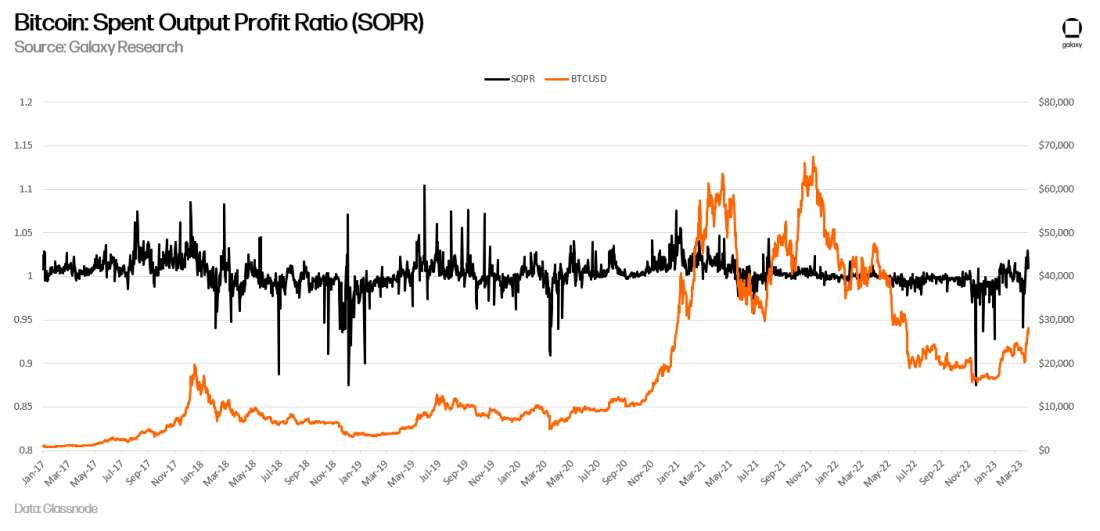

Another metric that helps understand the profitability of Bitcoin’s supply is the spent output profit ratio (SOPR), which divides the realized value in USD of spent coins by the value at which the coins were created. Essentially, this ratio can inform us as to whether, on a net basis, Bitcoin spenders are realizing profits or losses. That SOPR is above 1 for the first time shows that users are spending coins they acquired for lower, something that logically occurs when prices are rising, but which can also signal a bull market.

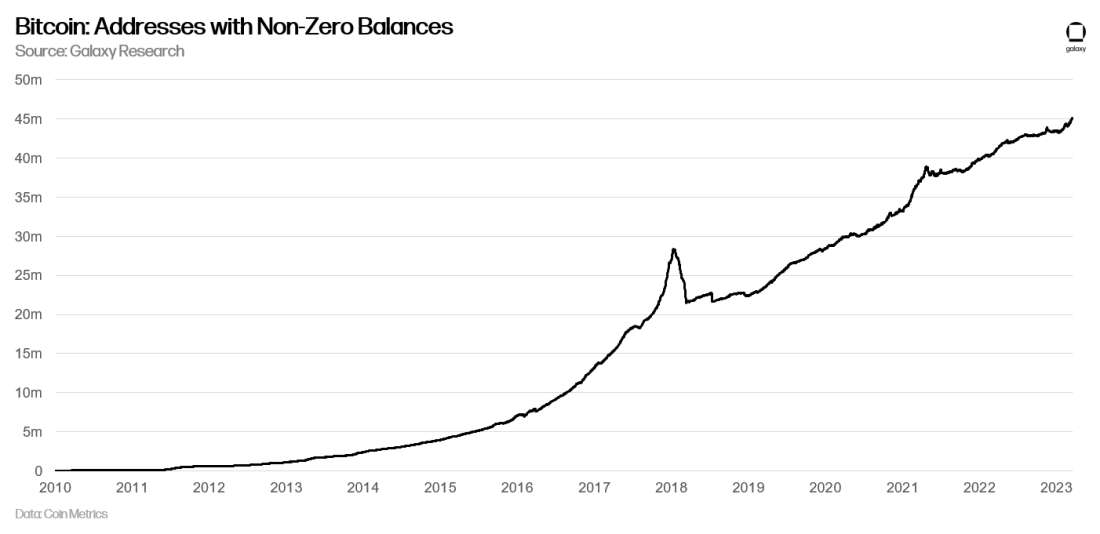

Accumulation

On-chain data suggests on-going accumulation of Bitcoin. The total number of addresses with a non-zero balance continues to rocket higher. More than 45m addresses hold BTC.

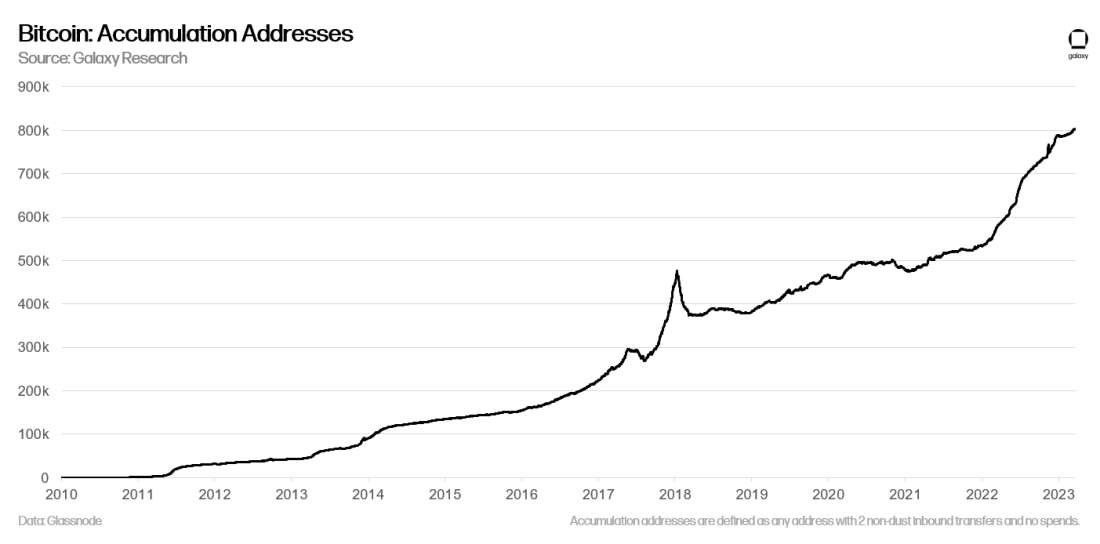

A large number of addresses have exclusively received Bitcoin – they have never spent. The number of so-called “accumulation addresses” has spiked in the last month.

Supply Age & Distribution

Long-term holders are holding longer, as evidenced by evaluating Bitcoin’s supply by age distribution. About 7% of Bitcoin’s supply moved in the last month (near all-time low), while more than 66% of Bitcoin’s supply hasn’t moved in over a year (all-time high).

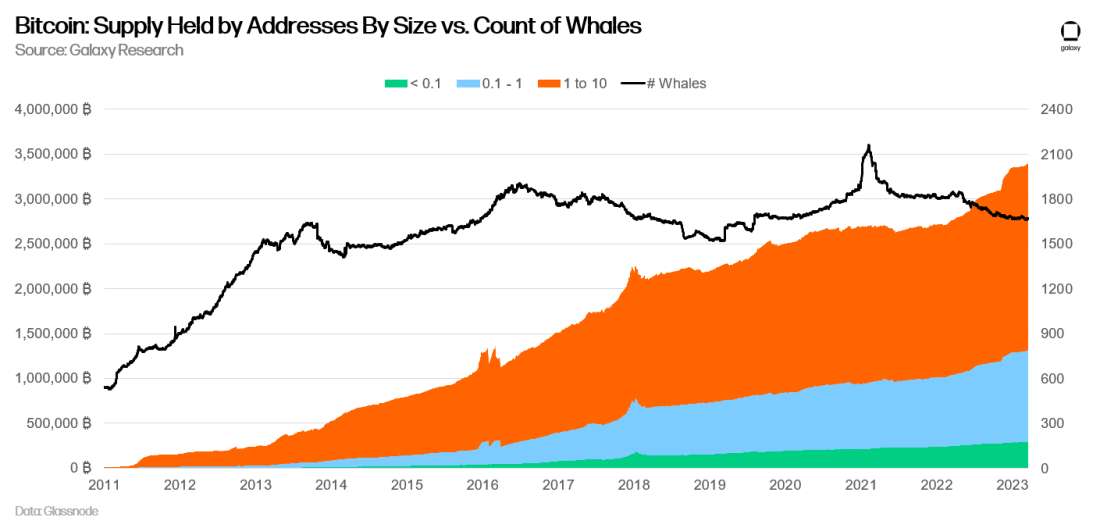

When we look at addresses by the amount of Bitcoin they hold, it’s clear that smaller holders have been accumulating while the count of whales has declined. Since the FTX collapse, the number of whales (>1k BTC) has fallen precipitously, suggesting a desire to diversify into multiple custodians and addresses, or out of bitcoin entirely. Meanwhile, wallets with <=10 BTC have been consistently accumulating 30k BTC per month, outstripping the network’s new issuance of ~900 BTC/day.

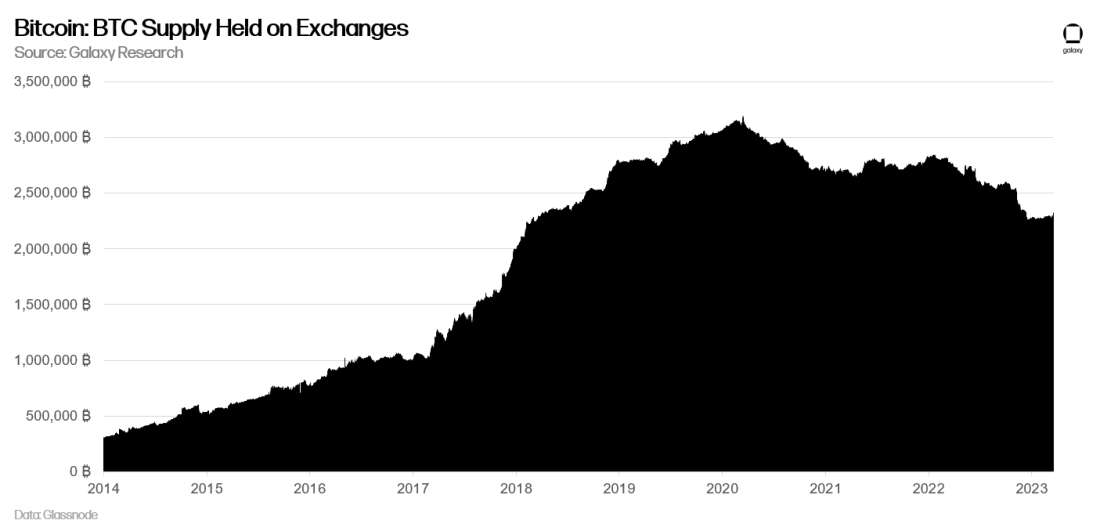

Supply on Exchanges

Exchanges are seeing their Bitcoin order books deplete since the early 2020 highs, with balances held in addresses attributed to exchanges (in this case by Glassnode) now at its lowest point since March 2018.

Future Supply Events

Two primary supply events loom in the future, one bullish and one potentially bearish.

The 4th Halving

Bitcoin’s next halving (projected to take place in April 2024) will bring the network’s

inflation rate below 1% with roughly 450 new bitcoin being mined per day. Historically, bitcoin’s three previous halvings (2012, 2016, 2020) have been pointed to as catalyzing subsequent bull-runs, as existent demand quickly outstripped lower levels of new supply.

Skeptics point out that on an absolute basis, the drop in new daily issuance in 2024 (~450 BTC) will be lower than previous halvings (~900 BTC in 2020). This marginal decrease in bitcoin’s inflation rate may prove less impactful than expected. Further, with ample historical data, rational actors are expected to have priced-in any impact of future halvings.

That being said, the 2024 halving should remain in focus for the simple reason that bitcoin’s inflation rate falling below 1% will place it among the hardest existing assets known to humanity, lower than historical store-of-value assets such as gold and silver.

Mt. Gox Payments

As result of the 2014 exchange hack, the Mt. Gox bankruptcy trustee holds 141,686 BTC plus cash and BCH according to September 2019 documents. Based on our research and conversations with Gox creditors, we do not expect there to be a material supply event for BTC as a result of distributions to creditors. The process for distribution of claims, while fluid, is as follows:

Holders were given the option to elect on March 10 whether they receive payouts in the following form:

Early payout in September 2023 on 90% of collectible funds, or

Wait for litigation to run course (timeline TBD) for a higher payout %

Headlines surfaced several weeks ago around the March 10 election date as the largest creditor, the Mt. Gox Investment Fund, opted to receive early payment, in approximately 70% BTC and 30% cash, and does not plan to sell the BTC it receives, according to reporting from Bloomberg. It’s also expected that BCH will be included in payouts.

While exact payouts and timelines are still unknown, we can expect a large portion of distributions to be paid out upon the early distribution date, slated for September 2023. Understanding the nature of Gox creditors as either very early BTC adopters with low cost bases or large claim investment funds, we expect most BTC will not be sold upon distribution. Selling of distributed BCH is more likely. Further, there will likely be second-order impacts in BTC lending markets if creditors look to lend their BTC either off-chain or on-chain via converting to WBTC.

Miner Holdings

Public bitcoin miners make up roughly 25% of bitcoin’s network hashrate, making their public updates on treasury management a good proxy for network-wide miner activity. In 2022, miners relied on selling down their bitcoin treasuries as the bear market deepened, resulting in an outsized amount of sell pressure. As noted in our recent End of Year Mining Report, we do not anticipate the same level of sell pressure coming from miners in 2023. Most public miners have now shifted away from a pure HODL strategy, opting for balanced approach by selling coin to meet operational expenses at a minimum. With that in mind, public miners appear to have established a run-rate of ~5500 BTC of selling per month.

Conclusion

It is clear that Bitcoin has been the best performer of the year, with BTCUSD seeing big legs up in both January and March. January’s increase can partially be explained by a reversion trade, with equities having already rallied on the back-half of 2022 but Bitcoin and other cryptocurrencies floundering post-FTX blowup. But March’s rally appears squarely on the back of a safe-haven narrative, with a bank crisis enveloping the globe and Bitcoin and gold rallying. Bitcoin dominance is increasing as it sucks value from within the cryptoasset ecosystem, but it’s performance is rightly garnering attention from the broader investment community. As we wrote on March 13, “markets are fleeing to the safety [Bitcoin] provides not only from within the cryptoasset ecosystem, but also perhaps from without.” The data suggests strength behind Bitcoin’s rally.

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2023. All rights reserved.