Executive Summary

If 2021 was the big breakout year for mining, then 2022 can easily be thought of as the reversion to the mean as miners faced the perfect storm of headwinds. A backdrop of eroding economics, rising energy prices, and constrained access to capital markets--with already high volumes of debt--have resulted in miners finding themselves in a precarious position for the second half of 2022. Survival is now the name of the game, and growth is secondary. Many miners have been here before--trying to build in a bear market-- but what they have not faced are the broader macro trends in crypto affecting their growth. We witnessed a spectacular failure of several venture-backed crypto startups, declining cryptoasset prices, and a macro and monetary policy environment that is unprecedented for Bitcoin miners. In this report, we examine the major events and trends that impacted the Bitcoin mining industry in 2022 and provide our perspective on the current state and future state of the industry.

Key Takeaways for 2023

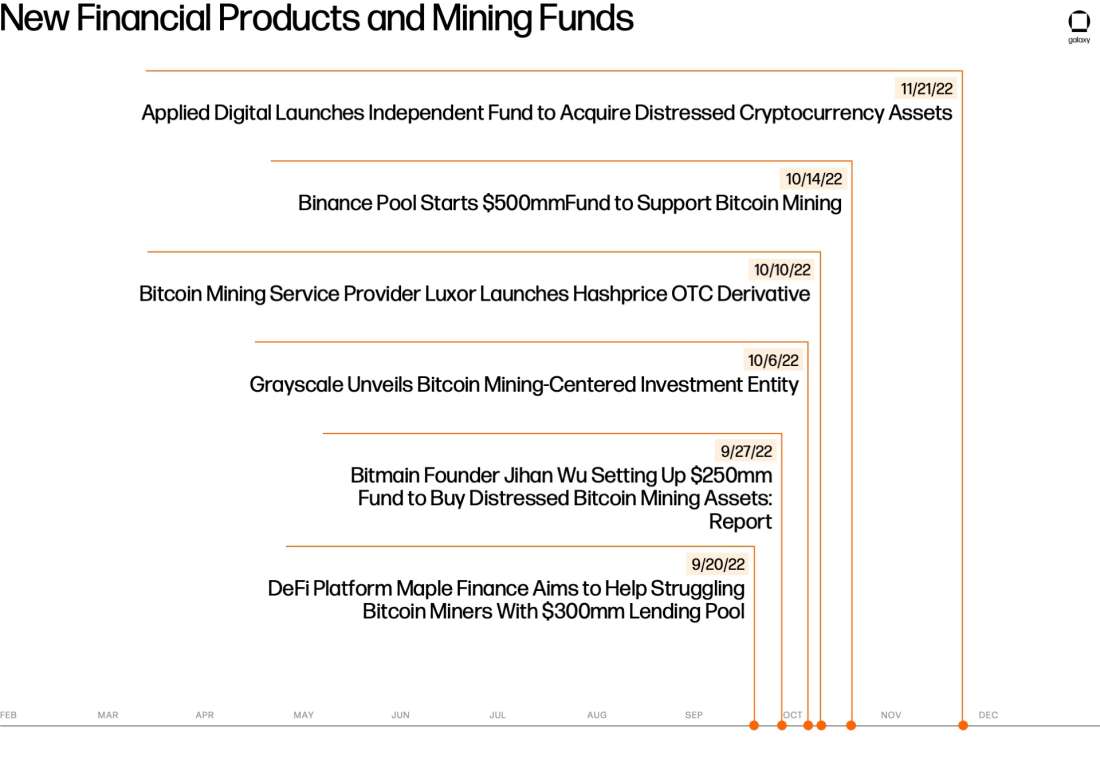

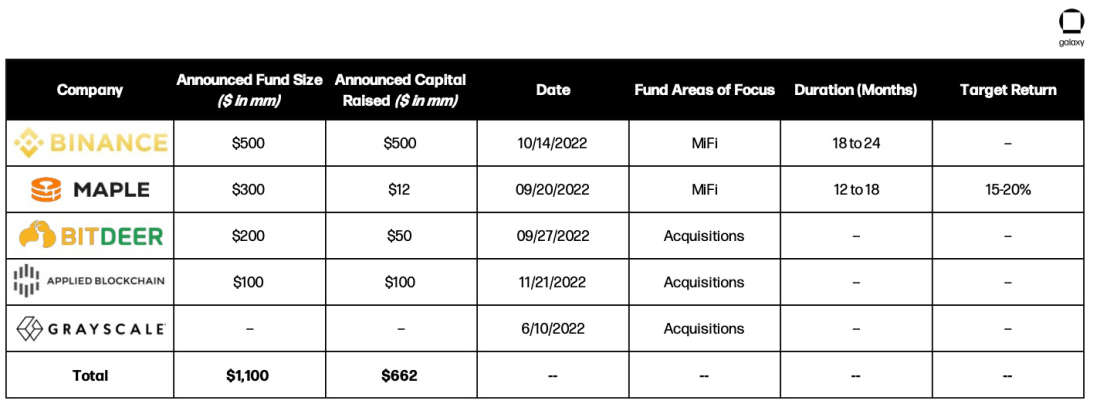

With $1.1bn of capital raised in distressed mining funds, investors are looking to opportunistically deploy capital into the mining space. The jury is still out on how exactly this capital will be utilized, whether it will be used to acquire ASICs or to provide lender of last resort financing to struggling miners.

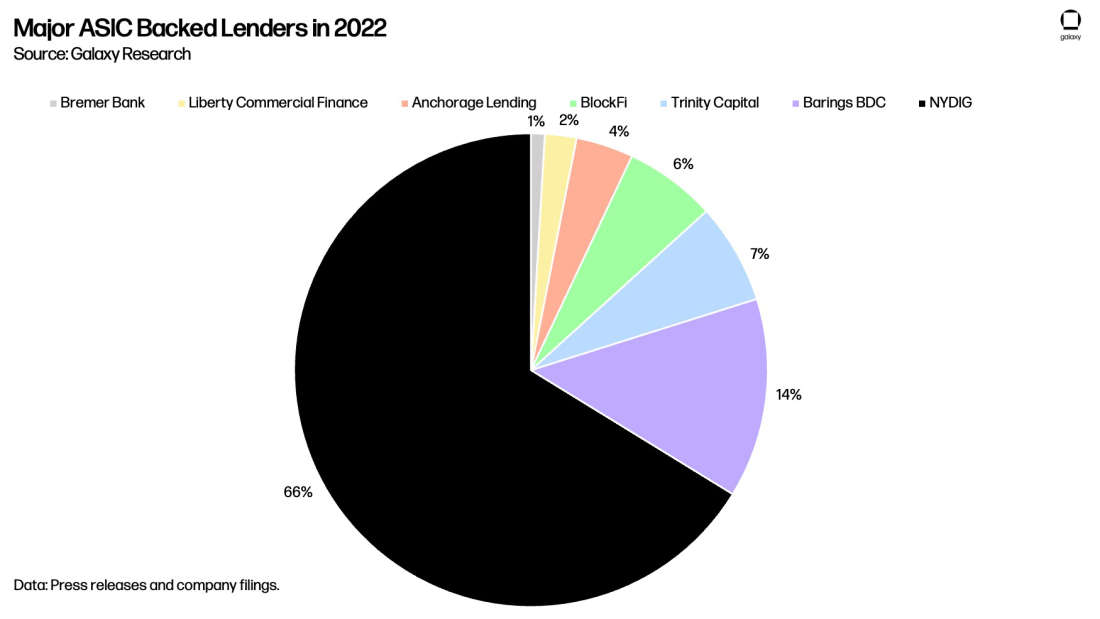

In 2022, publicly traded miners defaulted on 11.59 EH of hashrate through ASIC-backed loans. The financing structures lenders utilized during the bear market proved to be flawed on a number of fronts. ASIC-backed loans will need entirely new structures in order to be viable from a risk management perspective to lenders and from a feasibility perspective to miners. it will be interesting to see how ASIC-backed finance evolves over time and how lenders provide additional protections to learn from previous mistakes.

A 41-year high in power prices put a massive strain on hosting providers that offered fixed-rate contracts while being exposed to variable rate power prices. This caused more than 1 GW of hosting capacity to enter bankruptcy. We expect that the hosting landscape will undergo numerous changes in 2023, leaving fixed-rate contracts in the past. We may see hosting providers push for pass through power contracts plus a spread, while also offering clients certain revenue curtailment benefits.

2022 saw the continued convergence of the mining and energy industries and we expect this trend to continue in 2023. ERCOT established the large flexible load task force (LFLTF) which recognized miners as a flexible load resource and key contributors to grid stability. In winter storm Elliot that occurred on December 24th, bitcoin miners curtailed as much as 100 EH of hashrate representing 40% of network hashrate to help stabilize the grid.

As miners continue to look for ways to earn additional yield on their bitcoin holdings, they could consider the Lightning Network as it presents the opportunity to generate bitcoin denominated yield in a counterparty risk minimized way while also helping to support the broader bitcoin ecosystem. Lightning node operators are earning as much as a 5% APY by leasing channel liquidity albeit on smaller volumes. Lightning can also present new opportunities and benefits to miners if Lightning payouts become supported by mining pools.

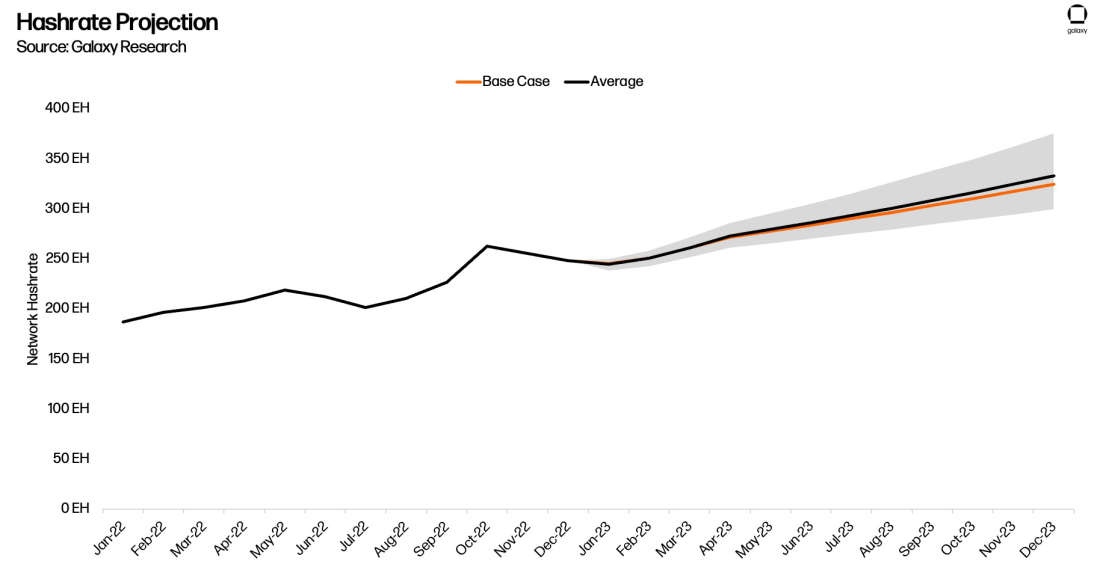

Unlike 2022, where hashrate continued to climb during the bear market, we expect 2023 to be a different year as the mining cycle comes to an end and much of the infrastructure and ASIC orders have been filled. In addition, we are of the view that bitcoin price appreciation will be relatively flat, and the 2024 halving will also dissuade miners from investing heavily in hashrate growth. Therefore, we expect end of year 2023 network hashrate to be at 325 EH. This reflects a 22.5% increase in network hashrate YoY.

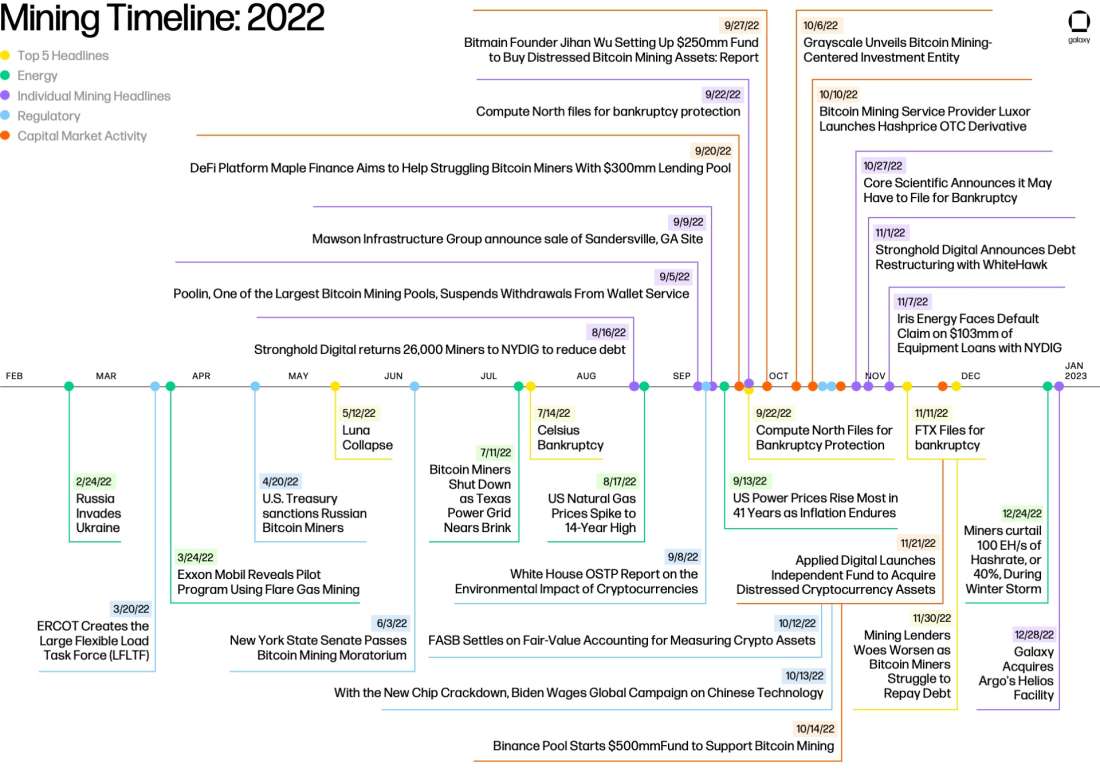

The Bitcoin Mining 2022 Timeline of Events

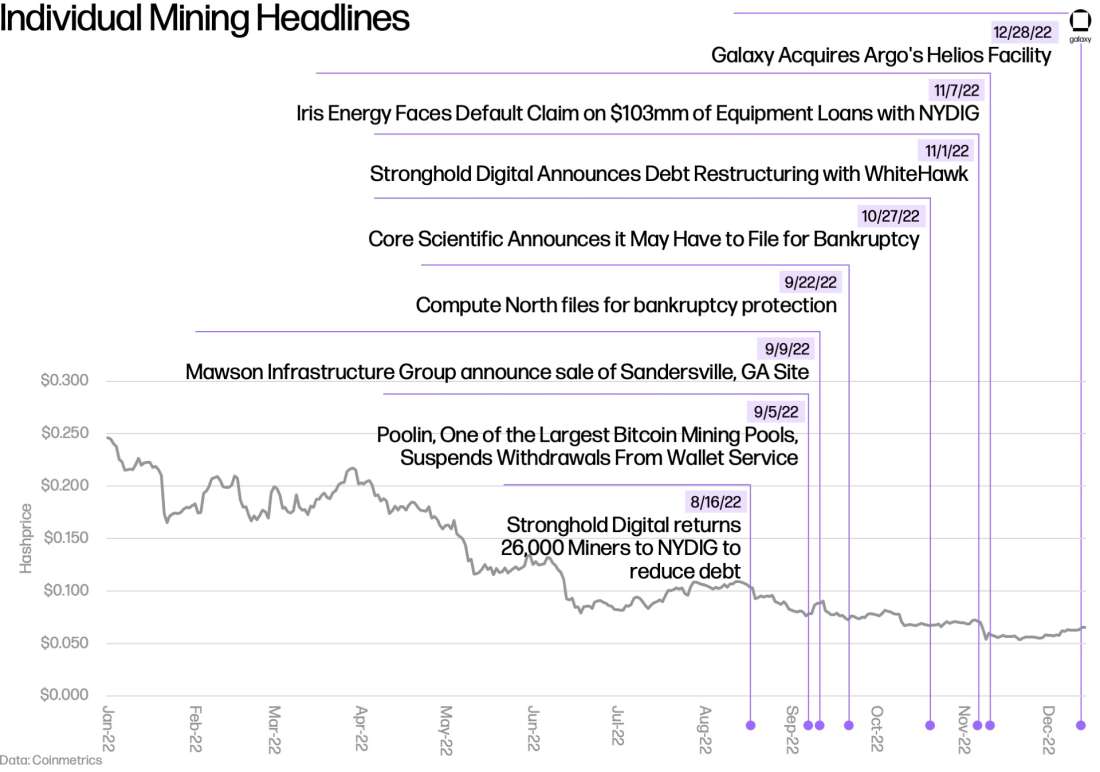

2022 was a turbulent year for the Bitcoin mining industry. In our timeline below, we highlight some of the major events that impacted the Bitcoin mining industry across topics such as energy, policy, and macro events.

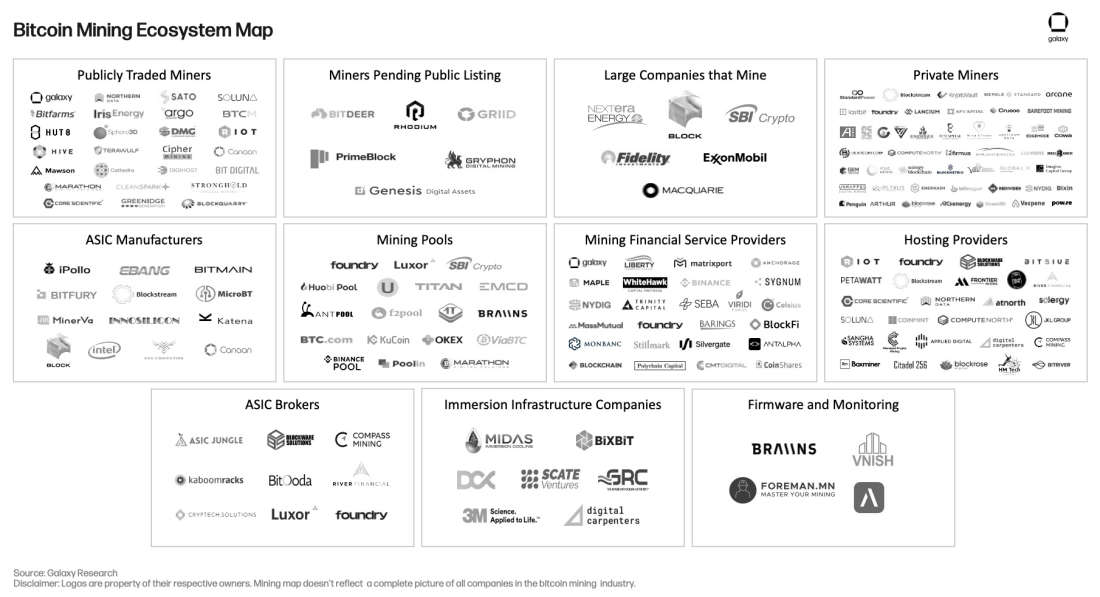

Industry Mining Ecosystem Map

The Bitcoin mining ecosystem has expanded dramatically over the years. Each niche within mining has seen growth with a series of new entrants. The most notable areas for growth are the mining financial service providers and the companies supporting the buildout of immersion infrastructure. Despite the hardships companies faced in 2022, competition and innovation in mining continues to push the space forward.

The Decline of Mining Economics

Bitcoin Price and Network Hashrate

There are two inputs that dictate the dollar revenue generated by a miner: bitcoin price and hashrate. These can be succinctly combined into one metric called hashprice, which shows the dollar value of Bitcoin mining rewards generated per unit of hashrate (TH/s) per day. As we describe in detail below, both bitcoin price and hashrate moved against miners, which made 2022 one of the toughest periods in Bitcoin mining history.

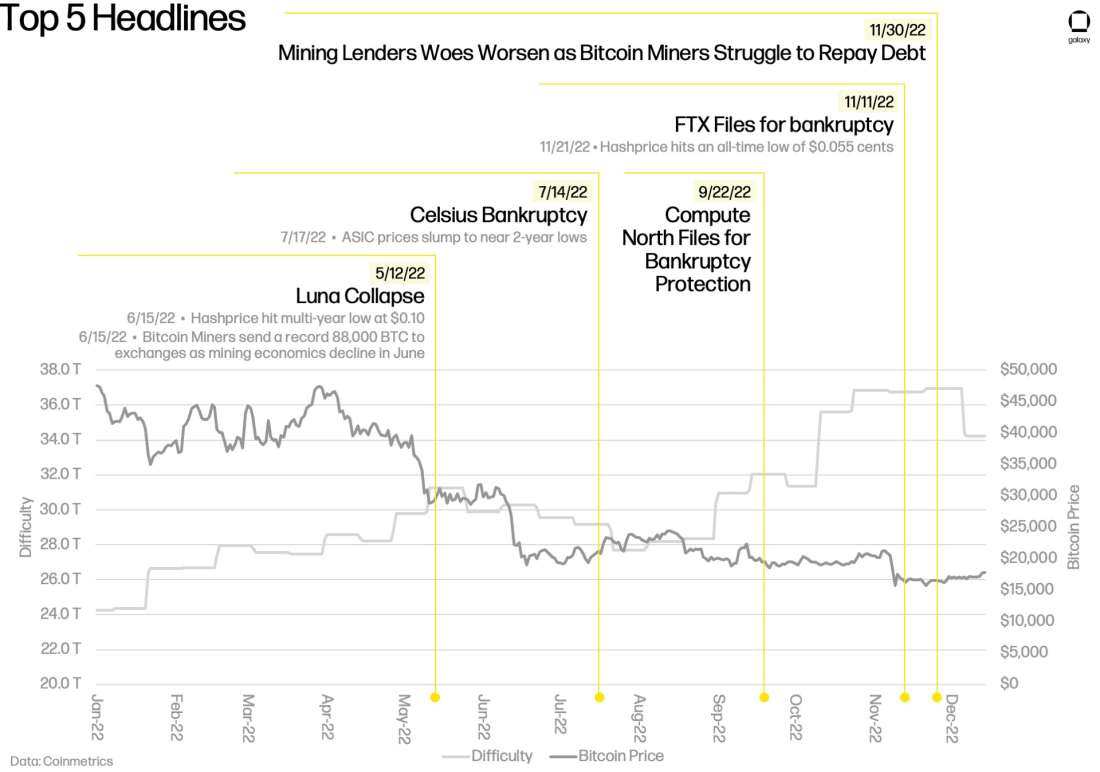

The first major component of the perfect storm that miners encountered was a declining bitcoin price, which finished 2022 down 75% from its November 2021 all-time high. Rising inflation forced global central banks to begin raising interest rates in Q4 2021, with the hikes continuing throughout 2022. As the cost of money increased, investor risk appetite waned, leading to contractions across equities, private venture markets, and bitcoin. Bitcoin price then stabilized in Q1 between $35,000-$45,000, with hashprice averaging $0.19 during Q1 2022 compared to $0.27 in Q1 of 2021. In Q2, the collapse of major crypto projects, hedge funds, and venture-backed startups sent bitcoin price to new cycle lows below $20,000. Hashprice averaged $0.14 during Q2 2022 down 26% from Q1 2022. As the Federal Reserve continued with rate hikes and investors continued to deleverage and rotate out of risk assets, hashprice continued its decline in Q3 averaging $0.09. During Q4 2022, the demise of FTX sent bitcoin price to yet another low, establishing a range between $15,000 - $18,000. Hashprice ended 2022 at $0.06, representing a 76% decline from the beginning of the year.

The second major factor imposing headwinds on Bitcoin miners was the increase in network hashrate and difficulty. While bitcoin price suffered from a major decline over the course of 2022, network hashrate continued to rise. Network difficulty grew 42.8% despite the bear market conditions persisting throughout the year. This compares to 27.3% growth in difficulty that occurred over the course of 2021. Network difficulty peaked on November 20th, 2022, at 37.0 T, implying a network hashrate of 264.5 EH before ending the year at 35.4 T, 4% below the high.

The growth in network hashrate—despite poor market conditions—was largely fueled by futures-based mining machine (ASIC) purchase orders that were made in 2021 with deliveries scheduled in 2022. At the conclusion of 2021, there were over 100 EH of machines contracted for by publicly traded Bitcoin miners alone with anticipated delivery dates throughout 2022. Of the hashrate that was contracted, we estimate that roughly 33% was actually installed. This is based on public miner hashrate of 30.9 EH at the start of the year and ending of the year hashrate of 71.0 EH. Even as mining economic conditions declined over the course of 2022, ASICs such as the S19 series and M30 series, which accounted for a significant percentage of delivered hashrate, were still profitable above $75 per MWh leading miners to continue to ramp-up hashrate.

As mining economic conditions severely declined after Q2 2022, many miners were forced to either sell machines or suspend payment on existing orders, which we believe largely contributed to the large variance between contracted and installed hashrate. Other contributing factors include ASIC manufacturers such as MinerVa, Intel, and Bitfury’s inability to deliver and delays in infrastructure buildout.

Energy Market

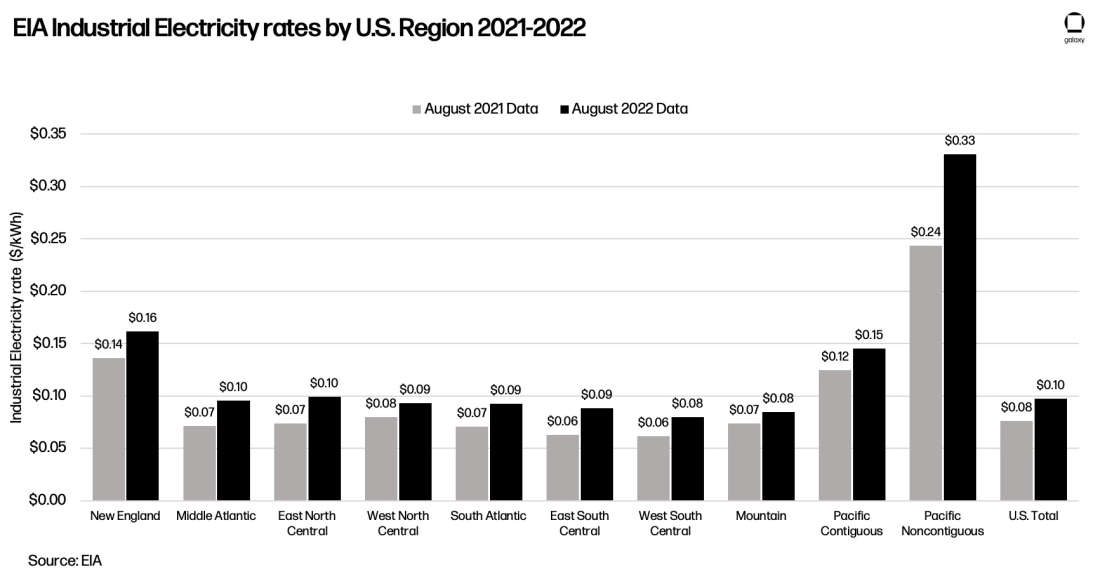

A significant increase in energy prices driven by macro factors such as Russia’s war in Ukraine, inflationary pressures, central bank tightening, and supply chain disruptions caused significant pressure on Bitcoin miners. These macro factors led to a spike in natural gas prices, which in power markets like ERCOT serve as the marginal price-setter and have an outsized effect on real-time forward contract pricing of energy. As a result, energy prices rose to some of the highest levels since 1981, increasing 25% from August 2021 to August 2022 according to data from the EIA, although they declined slightly in Q4.

The sharp rise in energy prices during the first three quarters of 2022, along with sharply declining mining economics, caused miners to become more serious about energy. However, one of the requirements to being able to participate in certain demand response programs and ancillary services directly is having a forward hedge on power. Securing a forward hedge on power has been a challenge for miners due to the margin requirement, which can be as much as 30% of the notional value of the forward hedge. During the bull market of 2021, miners prioritized growth, choosing to invest in ASICs and capacity expansion rather than in an energy strategy. With the significant downturn in market conditions, most of the miners do not have the cash to post as margin, causing many to take on variable price exposure. Towards the second half of 2022, we did observe some miners announce their ability to negotiate new PPAs or hosting contracts that would enable them to curtail their mining operations during peak demand periods and share in ancillary service revenue to some degree.

Miner Capitulation – Fighting to Survive

Capital Markets Activity

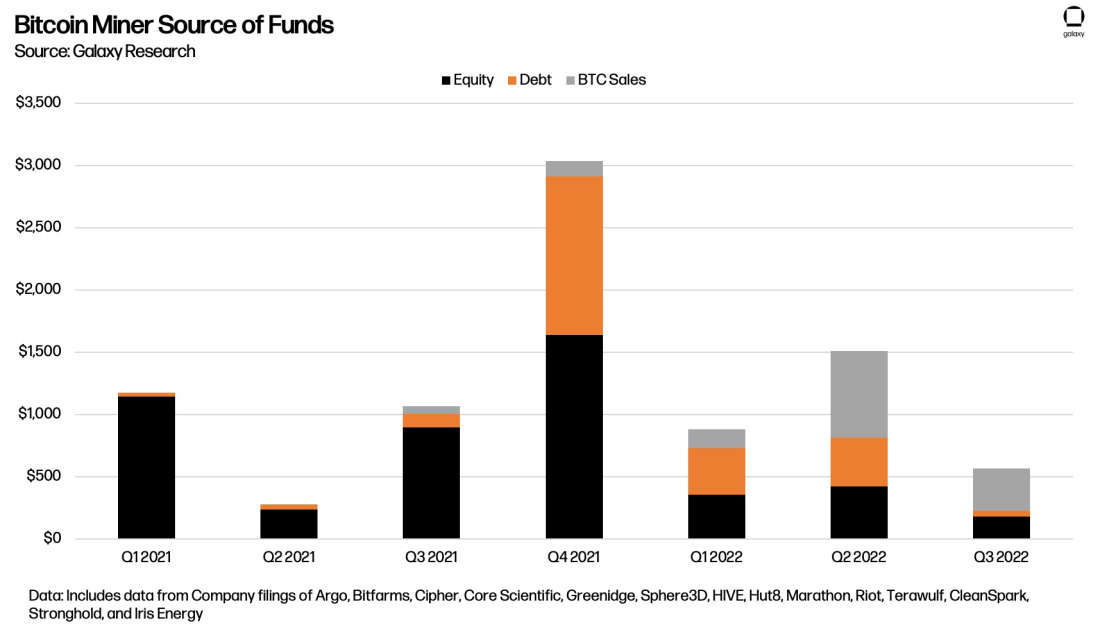

As result of the declining mining economics and macro conditions, capital markets turned out to be one of the hardest hit areas for miners. In 2021, miners had been heavily reliant on capital markets for raising the necessary cash to fund growth in the areas of infrastructure buildout and ASIC procurement, while also allowing them to be able to hold their bitcoin production for additional upside.

In the bull market of 2021, equity markets rewarded miners that announced lofty hashrate targets and ambitious growth strategies. Equity proceeds through public offerings and private placements were done at extreme valuations without any substantial operations online for most companies. Miners also took advantage of the abundance of cheap financings available, as lenders and investors were on the hunt for yield, specifically in Q4 2021. Although public miners only comprise a portion of network hashrate, they have easier access to capital markets and allow us to extrapolate overall trends observed across all miners.

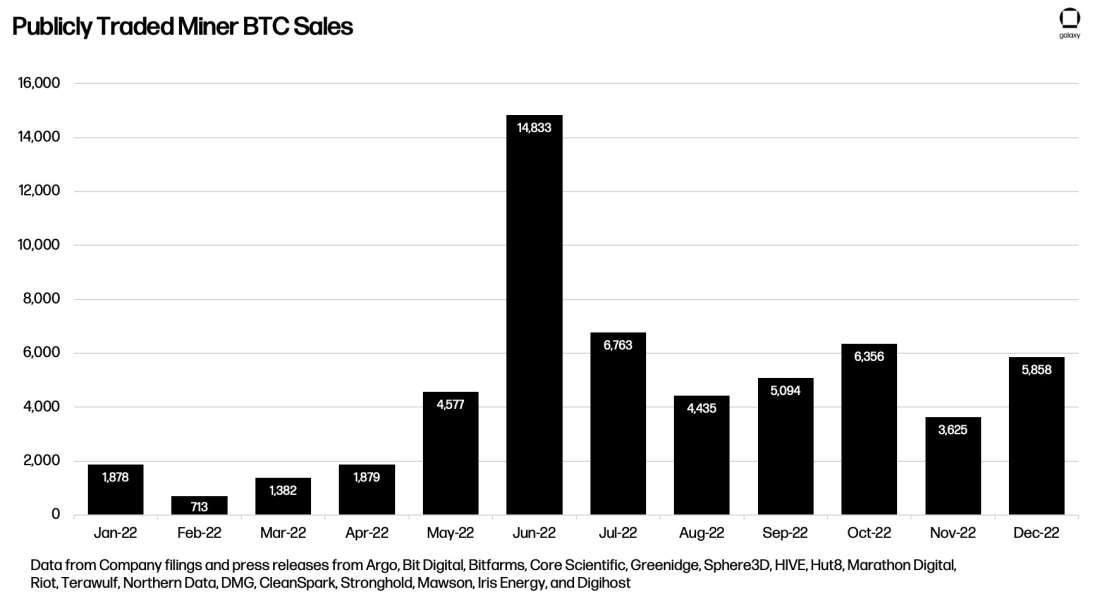

Through the first nine months of 2022, total capital markets activity for public miners was roughly 33% of 2021’s total. In 2022, equity issuances totaled $953mm (down 75% from the $3.9bn raised in 2021) and debt issuances totaled $813mm (down 45% from the $1.5bn raised in 2021). With capital markets access declining, miners had to solve for insufficient funds by selling their bitcoin reserves in order to make payments on ASIC and infrastructure contracts, as well as other operating expenses. Public Bitcoin miners sold roughly 58,773 bitcoins in 2022, compared to 3,500 the year before, with 36% of sales coming in Q2 2022. The slowdown in capital markets activity intensified in Q3, where less than $250mm was raised. Looking ahead to 2023, miners will likely need to continue to sell production to stay solvent.

Liquidity concerns stemming from faltering network economics caused several miners to default on existing loans. As ASIC prices dropped rapidly, Loan-to-Value ratios increased beyond comfortable levels for lenders, to the point where most loans have an LTV that surpasses 100%, meaning that the value of the collateral is worth less than the outstanding debt. Subsequently, an already small pool of Miner Finance lenders became unwilling to underwrite ASIC-backed loans.

Miners also attempted to tap equity markets by announcing “At-The-Market” offerings (ATMs) with varied results. Those that were able to sell shares ultimately raised funds at the expense of diluting shareholders as stock prices were 80%-90% off of all-time highs. For the miners that were unable to leverage equity ATM’s as effectively, selling bitcoin or ASICs at a discount for quick cash became an effective way to raise capital until the market became oversaturated. In the worst-case scenarios, miners then had to either take on additional leverage at unfavorable terms, default on ASIC-backed loans, default on machine purchase orders, or sell infrastructure to survive.

Capital available for miners is largely out of their control as it naturally follows movements in bitcoin price and broader macro conditions. What miners can control is how they manage their cash and bitcoin balance. Going forward, it is essential that miners develop a treasury management strategy that aligns with their future cash needs.

Treasury Management Strategies

During the bull market in 2021 and early in 2022, miners could use easily accessible external funds for working capital needs, allowing them to HODL bitcoin balances. As the bear market deepened in 2022 and capital markets closed, miners relied on selling bitcoin mined and held in treasury to build a cash balance. Unfortunately, the selling compounded as bitcoin continued to hit new lows. As a result, miners have had to adjust their treasury management strategies to be more aligned with projected near-term cash needs. Some of the approaches miners have taken to managing their bitcoin treasury are outlined below.

100% HODL: As previously mentioned, while many public miners adopted this strategy throughout the bull market, this is a difficult and risky strategy to maintain in a bear market. However, some miners managed to keep this strategy in 2022 and even grew their bitcoin balances YoY. Going forward, if bitcoin price rebounds to previous levels, we can expect these miners to have a significant capital advantage compared to others. Still, questions remain on the long-term sustainability of this strategy as the company generally needs to offset the missing liquidity from liquidating production by either diluting shareholders and/or using debt. This strategy was popular with traditional investors in 2021 that sought to find easy exposure to the bitcoin price by investing into the high-beta equities of miners. Now that demand has subsided, only a few companies still have an incentive to follow this strategy.

Sell 100% of Production: Before financial difficulties started for most, a few miners had already made the choice to constantly liquidate their bitcoin production, either daily or monthly. While this strategy removes any potential for price upside, it has the benefit of creating more stable and predictable cash-flows for the company.

Hybrid Approach: This strategy has been slowly emerging over the course of 2022, with some miners taking a more balanced and pragmatic approach to treasury management. This strategy oftentimes entails maintaining or targeting a specific bitcoin balance and reverting to sales when it’s met or exceeded. This method has the advantage of allowing miners to get the benefit of both bitcoin price upside and predictable cash-flows.

Yield Strategies: Throughout 2022, some miners made announcement regarding how they intend to get more granular when it comes to treasury management. Some chose to hire derivatives experts to generate additional cash-flows from their bitcoin balances while others chose to trust specialized companies, outsourcing their treasury management.

Having an effective treasury management strategy will be essential for long-term survival. Whether it be through systematic liquidations of mining rewards, locking in proceeds through bitcoin derivatives, or entering into hashrate derivatives contracts, miners must pay careful attention on how they manage their liquidity profile.

Bitcoin Miner Sell Pressure

The capitulation narrative assisted in the downward bitcoin price spiral in 2022. Looking at public miners as an indication of the broader space, selling of treasury holdings was amplified in Q2 as miners took emergency measures to bolster cash balances. Coupled with the deteriorating liquidity conditions, the 21,290 bitcoins that public miners sold in Q2 certainly played a role in the relentless headwinds that bitcoin was hit with.

In 2023, we do not anticipate the same level of sell pressure coming from miners. On a 30-day basis, miners across the network produce on average 27,000 bitcoins. A large percentage of this is likely liquidated soon after production to fund ongoing electricity costs and other operating expenses. Specifically for public miners, on average they have sold 5,739 bitcoins per month over the past 3 months. Since public miners make up about 28% of the network, if we assume similar behavior across the network, that implies about 20,496 bitcoins sold each month are attributable to all miners. Multiple data sources try to aggregate daily bitcoin trading volume, but using CoinMetrics’ trusted spot daily volume data for the second half of 2022 shows average monthly bitcoin trading volumes of roughly 13,800,000 bitcoins, much larger than the monthly selling trend from miners. This data is aggregated from a number of exchanges and doesn’t take into account OTC trades.

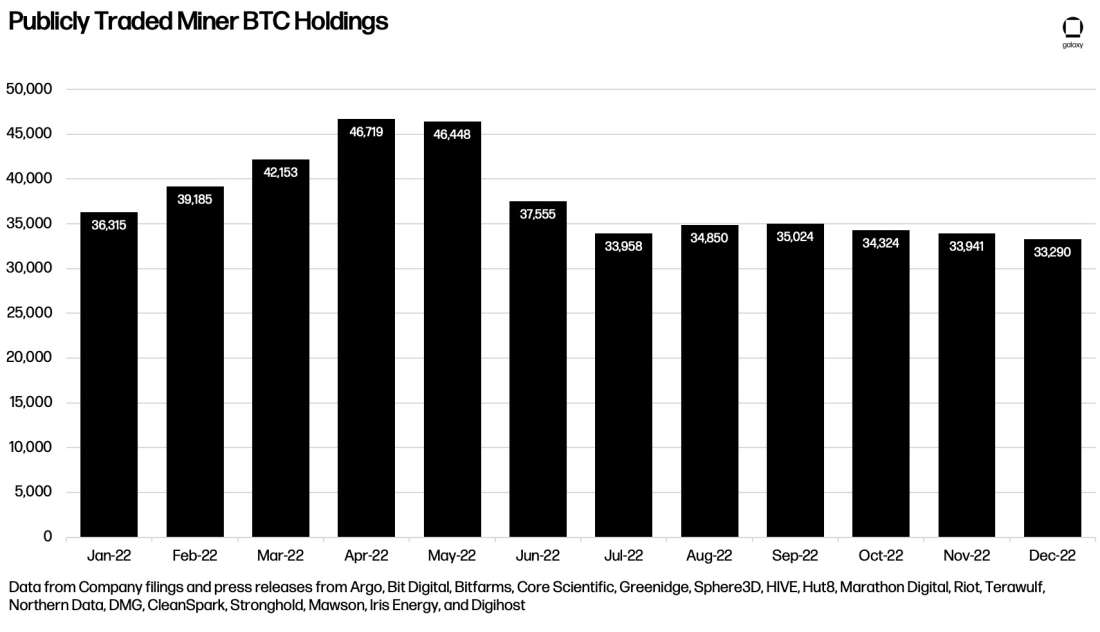

Where sell pressure could be reinvigorated is from larger scale bitcoin sales of treasury holdings, similar to Q2 2022. Below, we illustrate current aggregate public miner bitcoin treasury holdings. Public miners ended 2022 with roughly 33,290 bitcoins in treasury. A mass liquidation of these holdings, plus the unknown amount that private miners hold, in addition to their monthly production would not be trivial. However, we see this as an extremely low probability scenario because the miners that do have larger treasuries have already taken measures to strengthen their balance sheets, and immediate cash needs are not as urgent for them as it was in mid-2022.

ASIC Liquidations and Market Dynamics

The market for ASICs was significantly affected by the broader downturn in 2022. Worsening economics squeezed operating cash flow for miners and after layering in other operating expenses, debt obligations, and capex payments, cash balances were depleted rapidly. Miners that could neither raise capital nor had enough cash or bitcoin on hand were forced to sell ASICs and re-evaluate expansion plans to stay solvent.

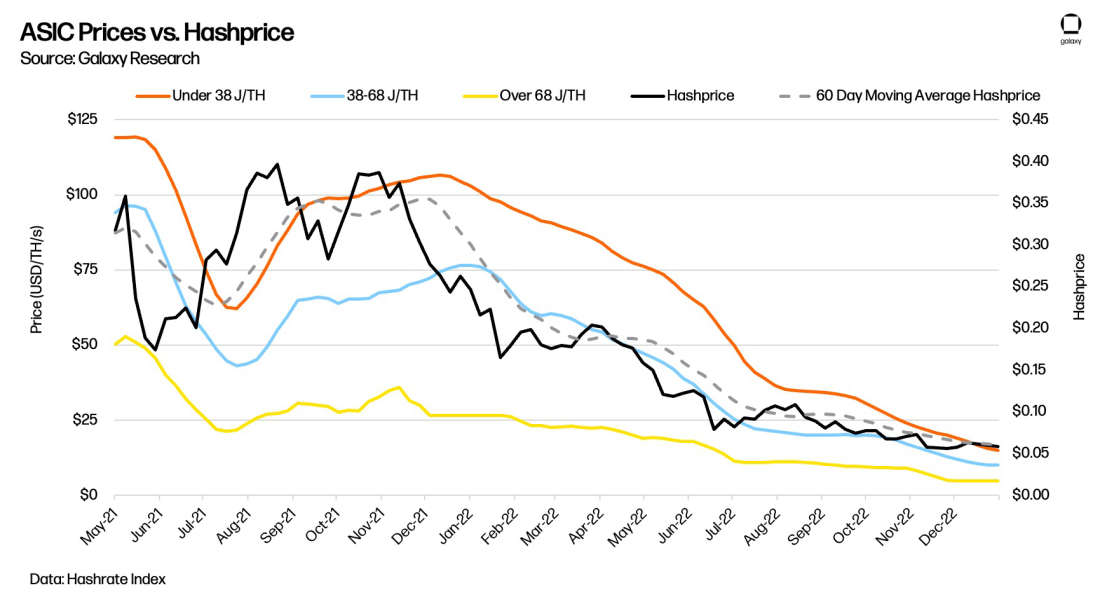

The ensuing influx of supply on the secondary market drove ASIC prices to as low as $15 per TH, as observed on Luxor’s ASIC Index, and forced Bitmain, MicroBT, and Canaan to also decrease prices for direct purchases. The ASIC Index measures an average of observable ASIC prices from multiple sources, and the reality is that OTC deals have been executed even lower than this level.

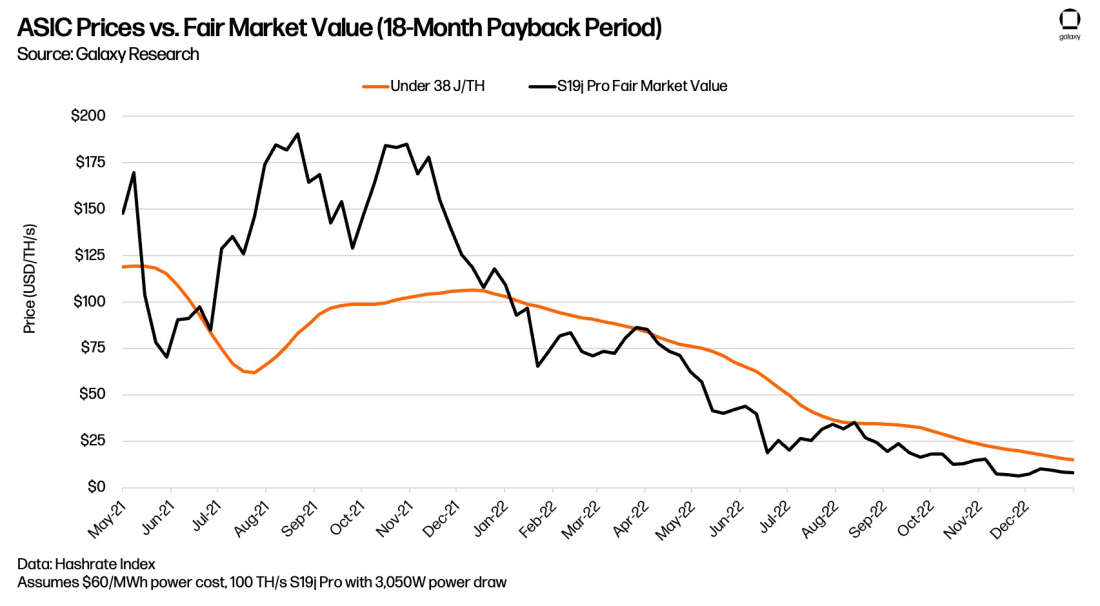

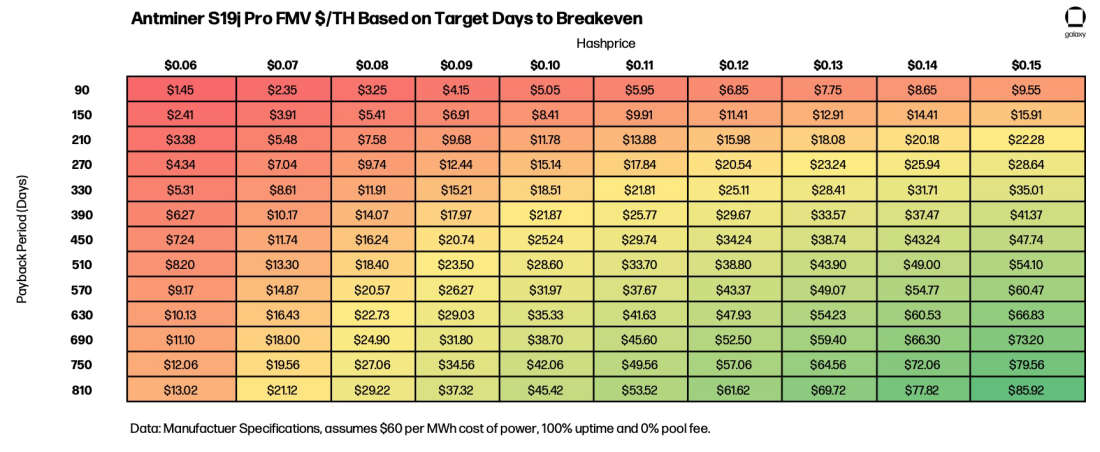

Not only was the supply glut a factor that contributed to ASIC price declines, but the actual return on investment potential of ASICs declined meaningfully, pushing the fair market value (FMV) down much more quickly than the prices sellers were willing to sell at, causing bid-ask spreads to widen. ASICs’ fair market value are commonly assessed using a payback period, which is the amount of time it takes to recoup the initial capex investment on the ASICs. As profitability declined from lower hashprice and higher energy cost, payback periods extended, and demand dried up. At the same time, there was excess supply hitting the market due to miners selling machines for liquidity, infrastructure delays, or just no longer being able to operate them profitability as result of increases in energy prices. All of these factors contributed to the large decline in the FMV of ASICs over the course of 2022. In the chart below, we compare the implied FMV of ASICs using an 18-month payback period against Luxor’s ASIC Index data.

The path forward for bitcoin price, hashrate, and energy prices is very difficult to predict. Until there is clear line of sight on improving economics that prompt the supply glut to be reined in, it is difficult to see ASIC prices rising materially in the near-term.

Summarizing Miners’ Survival Tactics

Looking at the current state of the mining landscape at the conclusion of 2022, miners are in survival mode and will likely have to be until the next halving cycle. In 2022, we saw miners default on $277mm of ASIC-backed loans, handing back over 11.59 EH of machines to lenders. We observed miners sell a total of 8 mining sites for a total volume of $249.8mm, which represents 538 MW of capacity. Public miners used a variety of strategies to try and extend their operational runway and avoid bankruptcy:

Delaying machine purchase orders: Miners that had made large ASIC futures orders in 2021 at peak ASIC pricing levels that were running out of cash pushed to negotiate pauses in payments with ASIC manufacturers. ASIC manufacturers were willing to work with miners on delaying payment as demand and pricing power for ASICs declined, making a restructuring of the contract duration and terms a better outcome than an outright default.

ASIC discounts with manufacturers: As ASIC prices declined, manufacturers began offering miners options such as credits that could be used towards future orders, or modifications to current orders by offering more machines for the same contract price or more efficient ASICs. According to Luxor's ASIC Index, at the peak, newer generation machines were priced at nearly $120/TH. ASIC manufacturers typically require deposits that are calculated off of spot prices soon after the order is placed. Therefore, at peak 2021 ASIC prices, miners had to pay large deposits upfront, well before they would actually receive the ASICs. Now that many do not have cash to make outstanding prepayments, they are trying to monetize their existing deposits that have been already paid to ASIC manufacturers by reducing order sizes and paying for ASICs by drawing down on the deposits.

Hashrate swaps: While this only occurred once in 2022 (for publicly traded miners), hashrate swaps allow a miner to switch a current batch of orders for a different renegotiated batch of machines, at no additional price. Miners can either choose more efficient machines or choose to get more less-efficient machines in exchange.

Selling sites and mining infrastructure: In more draconian situations, some miners explored sales of entire mining sites because operating costs were too high, the costs to expand the site were prohibitive, or just because the company needed an immediate injection of cash.

Restructuring debt: Because miners took on so much debt in 2021, it was not uncommon to see lenders and miners come to bilateral restructuring agreements to either reduce principal repayment amounts and/or increase the duration of the loans.

Underclocking machines: Towards the end of 2022, we saw miners decide to optimize for efficiency instead of hashrate in an effort to preserve mining margins and cash-flow. Underclocking machines is the process by which miners can reduce the hashrate of a machine with the aim of increasing efficiency (lowering J/TH). In one instance, a miner managed to improve its efficiency by over 36% from 35 J/TH to 23 J/TH, thus lowering their breakeven hashcost. Underclocking machines allows miners to continue to operate in a bear market as opposed to turning off machines. We expect this trend to intensify in 2023 if mining conditions worsen and energy prices remain elevated.

Other Trends in Mining

Regulatory

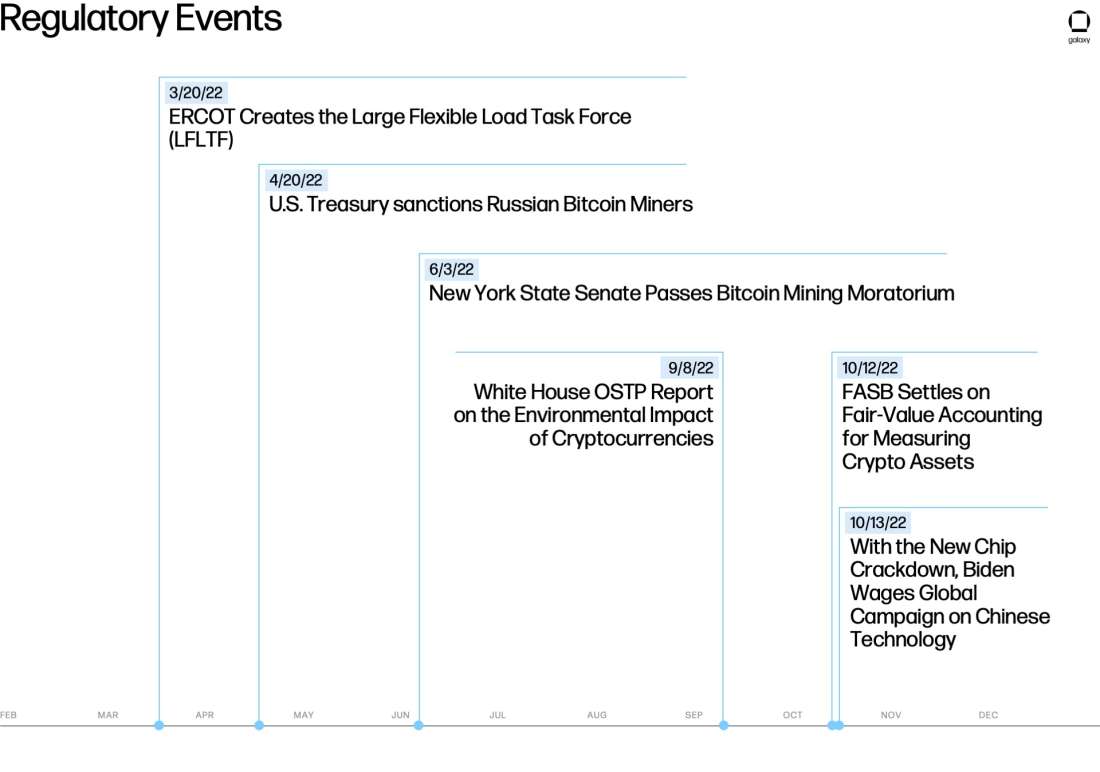

In 2022, the mining industry faced regulatory pressure at both the federal and state levels. While the mining industry has faced criticism in the past, 2022 saw the emergence of more coordinated and structured attacks against Bitcoin, Proof-of-Work (PoW), and its electricity consumption from policy makers and well-funded organizations such as Greenpeace.

Throughout 2022, multiple states attempted to stifle the growth of the mining industry by implementing policies that would effectively ban any new mining company from operating in their respective region. The state of New York enacted a two-year ban on operations using non-renewable energy sources and requires that miners use 100% of renewable energy in their mix. We also observed, the Canadian province of British Columbia enact an 18-month moratorium on requests to start new mining operations. While existing miners in both British Columbia and New York were not impacted, it sets an easy precedent for other provinces in Canada and states in the US to take a harsh approach to mining. As a result, some miners have announced their intent to diversify their geographic exposure outside of the US and Canada, but many are sticking to more friendly states in the US such as Texas.

At a federal-level in the US, the industry faced direct criticism from the White House in the second half of 2022 with the release of a long-awaited report mandated by President Biden’s March 9, 2022 Executive Order named “Climate and energy implications of cryptoassets in the United States.” The 46-page report painted a mostly grim picture of the industry and focused on the negative externalities of PoW in comparison to other “less energy intensive” mechanisms.

The report was authored by the White House’s Office of Science and Technology Policy (OSTP) and did acknowledge the potential of “Flared-Gas” mitigation technologies (read more about that here) and the positive impact that mining could have in order to achieve the U.S. climate goals. The report primarily focused on the potential negative effects of Bitcoin mining without accounting for the positive effects or the efforts the industry has made to be more transparent and use cleaner forms of energy. The report fell short on 3 specific areas that will become paramount to discuss with policy makers in 2023: the purpose of Bitcoin and the importance of decentralization, the climate impact of the mining industry, and the complex relationship between mining and the broader U.S. grid infrastructure.

2022 was also marked by a push from activists at Greenpeace and executives of Ripple (currently engaged in a securities violation suit with the SEC) to “Change the code” of Bitcoin and make it switch from PoW to Proof-of-Stake (PoS). This campaign was choreographed with Ethereum’s transition to PoS and touted the supposed environmental benefits of the move. The campaign received very little attention from the community because it is a widely accepted fact that PoW and PoS have different trade-offs (scalability and decentralization) that each asset has to optimize for, with Bitcoin choosing to optimize for decentralization.

Despite negative criticism regarding Bitcoin mining’s electricity usage and energy mix, there were some positive developments in the industry that have helped to address these criticisms. Throughout 2022, multiple House and Senate members of Congress became advocates for the Bitcoin mining industry. Additionally, the Electric Reliability Council of Texas (ERCOT) made statements that explicitly argued in favor of mining’s impact on the grid after seven lawmakers led by Sen. Elizabeth Warren, D-Mass., asked ERCOT for data on the energy consumption of Bitcoin miners, including about the impact the mining industry has on energy costs to local families and businesses.

In a report discussing resource adequacy for the Texas region published in December, ERCOT directly states that Bitcoin mining operations are flexible loads that can be beneficial to the grid during the upcoming winter and peak load times:

“Due to the anticipated interconnection of an increasing number of large flexible Loads in the ERCOT Region, ERCOT is establishing an interim, voluntary curtailment program that would allow these Loads to assist ERCOT in ensuring reliability during periods of high system demand.”

In total, the report estimates that over 1.7 GW of energy could be curtailed thanks to miners, making them instrumental in load response programs. Looking ahead to 2023, ERCOT’s recognition of Bitcoin mining’s usefulness as a large flexible load resource for the grid should help governmental agencies and policymakers see Bitcoin mining as constructive for the US’ energy transformation.

Stratum V2, Decentralization, and Innovation in the Mining Space

In light of the increased regulatory pressures and political attempts to disrupt Proof-of-Work mining, ensuring that the Bitcoin network remains decentralized is more important than ever. Over the course of 2022, tremendous progress was made towards the development of Stratum V2 (Sv2), an overhaul of the messaging protocol used for communication between miners and pools that organizes the creation of blocks and submission of hashes by miners. Stratum V2 is an improvement over Stratum V1 in regards to flexibility, communication efficiency, and security and enables miners to construct their own block templates to submit to the pool operator (Galaxy’s report on StratumV2). In 2022, developers released a reference implementation of Sv2 that provides a robust set of primitives for anyone to expand on the protocol and test-out some of the most important use cases for mining pool operators. The Sv1<->Sv2 miner proxy does not support all the features of Sv2 today but works as a temporary measure before upgrading completely to Sv2-compatible firmware.

On the firmware side, Braiins continued to be at the forefront of innovation by releasing the long awaited Braiins OS+ upgrade, allowing miners to optimize the efficiency and hashrate of the S19-series of miners from Bitmain. Custom firmware solutions such as Braiins OS+ are critical for miners that are struggling to keep afloat due to the current mining conditions. Using Braiins OS+ can improve the efficiency of an S19j Pro by as much as 25%, which can improve the machines breakeven dollars per MWh from $82 to $109 based on a hashprice of $0.06.

On the hardware side of the industry, several new ASICs were released and announced:

S19 XP by Bitmain: The 5nm chip technology, which all major manufacturers have announced using for their new ASIC models, will usher a new efficiency era for mining but will also bring its own set of challenges when it comes to price and competition for space at the foundry. The chips used in the S19 XP will be highly sought after by a wide range of large companies across a multitude of industries with bigger bargaining power than Bitmain.

S19j Pro+ by Bitmain: Clocking in at 122 TH/s for an efficiency of 27.5 J/TH (3,355W), this improved version of the S19j Pro will be released in Q1 2023 and is specifically designed for a wider range of American style data center infrastructures.

MicroBT US Assembly and new M50 series: The classic air-cooled M50S is expected to deliver over 126 TH/s for an efficiency of 26 J/TH. According to a statement by the company, MicroBT is focusing on the emerging North American market and would be able to satisfy demand for up to 30,000 machines per month from its production site located in Southeast Asia. MicroBT has also announced that it is beginning to assemble ASICs inside the US, which will be a huge improvement for US based miners, allowing them to save on customs, shipping, and tariffs.

A13-series miners by Canaan: With both new models respectively achieving 110 TH/s for an efficiency of 30 J/TH for the A1346 and 130 TH/s for an efficiency of 25 J/TH for the A1366 model, this makes the A13-series miners slightly more efficient than MicroBT’s M50S. Because Canaan is the only publicly listed ASIC manufacturer, we have some degree of insight into their operations and all signs point to a significant reduction in production volume going forward with a stronger focus on the production of next generation ASICs.

Entrance of Intel in the ASIC business: Early in 2022, Intel officially announced the launch of its own mining chip called “Blockscale,” boasting an efficiencyof 26 J/TH, in line with other newer generation ASICs. Despite these announcements and the flexible nature of their white-labeled offering focused exclusively on the chips instead of the form factor, there is no clarity on how these machines effectively behave in real-world conditions, although pricing will likely be cheaper compared to competitors. It’s also unclear if machines will be eligible for resale, or if miners will have to work directly with Intel in order to procure them.

2023 Outlook

Creative Financing Solutions

Miners won’t have the same access to funding through capital markets in 2023 as they did in 2021 and early 2022. Several companies still need new sources of capital in order to finance the construction of infrastructure or procurement of ASICs and one such way they can solve for this is through partnerships with distressed mining funds.

As shown in the timeline, distressed mining funds emerged throughout the second half of 2022. Mining operators could potentially strike joint venture agreements with these funds who can provide upfront capital to finance capex expansion in exchange for hosting capacity or a profit share. Importantly, these funds can provide a means for existing operators to grow and expand their mining facilities in a capital minimizing way. However, it’s unclear what progress or impact has been made since the initial announcements of many of these funds.

The emergence of these distressed mining funds shows that there is a level of demand for exposure to the mining industry as these investors begin to view Bitcoin mining very similarly to other commodity-based markets.

Five different funds representing more than $1.1bn of potential capital have announced their intentions to provide funds as a lender of last resort and invest in mining infrastructure and ASICs.

It will be interesting to see if these distressed funds have a significant impact on miners and the broader ASIC secondary market or if they will even issue any capital to a miner. As the bear market continues and miners are forced to sell and/or default on machine loans and purchases, these funds could serve as the buyers of last resort creating a “floor price” for ASICs. However, this would not likely change the ASIC markets from being oversupplied.

Primary and Secondary ASIC Markets

In 2021, the bull market stimulated immense interest in Bitcoin mining. Capital flooded into the industry and miners did everything in their power to buy ASICs from Bitmain, MicroBT, and other ASIC manufacturers. These purchase orders had long lead times but provided for better pricing than the ASIC spot market. In order to produce the ASICs, manufacturers had to place orders at chip foundries such as Samsung and TSMC months in advance to receive their allocation. With the skyrocketing demand for ASICs, Bitmain and MicroBT placed large orders at foundries for chips and ramped up production to fulfill ASIC purchase orders.

Today, ASIC manufacturers are flush with inventory and secondary market supply has grown tremendously. In the US, secondary supply has ballooned, which will likely result in miners pivoting away from entering into ASIC futures orders in the near-term. The ease by which miners can now procure ASICs in the US allows them to prioritize their time and capital towards building out infrastructure as opposed to procuring ASICs. While demand has fallen significantly, we have yet to see any indication of major shifts in chip allocation from the foundries to manufacturers like Bitmain and MicroBT. Bitmain has attempted to reinvigorate demand through machine firmware upgrades that improve miner efficiency, but geopolitical uncertainty, as well as strong margins on machine sales, will likely continue to keep primary market supply at high levels.

The oversupply of ASICs and emphasis on mining ROI will keep ASIC prices suppressed going forward. As mentioned earlier, 18-month payback period targets very closely track actual ASIC prices observed. However, with the next halving approaching (currently expected in March 2024), miners may demand even shorter payback periods to reduce their exposure to volatility around the halving. Targeting a 15-month payback period today based on the current block subsidy would imply that the fair market value of an S19j Pro is just over $7/TH, assuming $0.06 hashprice and power cost of $60 per MWh.

For the reasons outlined above, we anticipate that the primary and secondary market will remain saturated in the months to come. While the entry of capital from distressed funds and other investors may provide some support going forward, the surplus of ASICs on the secondary market and the continued production of new ASICs from manufacturers will put strong deflationary pressures on ASIC prices.

ASIC-Backed Lending

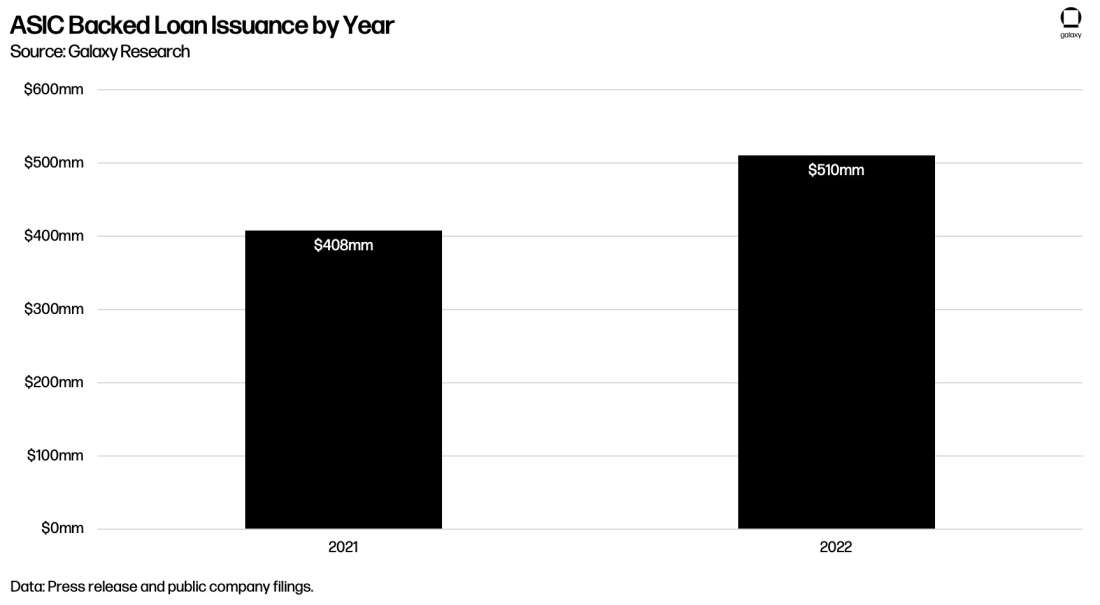

Despite bear market conditions experienced throughout 2022, there was still $510mm of new ASIC-backed loan issuance, which reflects a 25% increase over total 2021 issuance, although the entirety of ASIC-backed loan issuances for 2022 took place in the first half of the year. As hashprice made new all-time lows in the second half of 2022, several large publicly traded miners defaulted on these loans or had to restructure their agreements. Overall, the existing structures for ASIC-backed loans have failed both miners and lenders. From lenders’ perspectives, poor underwriting frameworks failed to fully account for how these loans would perform in downside scenarios, and a lack of margin call covenants caused lenders to end up in undercollateralized positions. In some cases, lenders opportunistically entered the space chasing yield without fully understanding the nature and nuances of the industry. From miners’ perspective, the loans failed to provide flexibility of payments due to market conditions, durations that didn’t match the economic useful life of machines, and failures to enact proper treasury and risk management strategies.

Based on public announcements, miners defaulted on loans backed by more than 11.59 EH of hashrate. Given that ASIC prices are already very depressed, and there aren’t many buyers in the market for the level of volume lenders now possess, lenders were forced to explore creative solutions to try and avoid taking a loss. Many ASIC-backed loans have already been restructured, and we expect further restructurings to involve lenders eliminating debt in exchange for favorable hosting rates or equitizing the debt.

Looking ahead, lenders must revamp ASIC-backed loan structures to remain a viable product for miners. With more careful structures, ASIC-backed loans will remain an attractive option for miners to grow and scale their operations, particularly as capital markets continue to remain constrained for public miners. From a structuring perspective, these loans must include a better mechanism for determining monthly payment amounts based on market conditions, something that can be accomplished by setting payment parameters based on hashprice levels. Furthermore, lenders will likely need to include a margin call covenant based on weekly or monthly marks to market for ASIC collateral value. We also expect to see tougher evaluation criteria from lenders and a stronger emphasis on companies having a fixed power purchase agreement or hedge on power.

High interest expense has been a major criticism of ASIC-backed loans, which had been driven primarily by lenders’ cost of capital, the fact that the collateral is not very liquid, and larger compensation demanded for higher risk taken. Because most lenders in the space are crypto native and younger companies, their borrowing rates are higher, which has to be baked into the interest rates lenders passed on to borrowers. As the cost of borrowing for lenders declines, interest rates should decline as well. Once mining economic conditions improve and capital markets loosen, public miners may opt for other forms of debt, particularly unsecured debt if they can obtain it. At this point, we expect that most of the volume and interest for new ASIC-backed loans will come from private miners in smaller issuance sizes.

Another challenge ASIC-backed lenders have faced is determining how to underwrite new ASICs from manufacturers outside of Bitmain and MicroBT, where there is a lack of data on performance and secondary market sales. Additionally, lenders have struggled to determine how to underwrite the residual value of ASICs that were placed in immersion tanks, or that use custom firmware, or are simply of a niche variety, like hydro variant ASICs. With respect to ASICs that are being operated in immersion tanks or hydro machines, lenders may require that both the ASICs and immersion cooling infrastructure are collateralized together such that the lender can step in and operate the equipment in an event of default.

Hosting

A lesson from 2022 is that hosting poses a lot more challenges and risks than many miners may have originally thought. Hosting providers were the hardest hit actors within the space, with the Compute North bankruptcy representing one of the biggest events in Bitcoin mining last year. Hosting providers offered customers fixed power cost contracts while taking on real-time power prices, a source of problems for many traditional miners. This inevitably led to higher costs for hosting providers than they were earning from their customers as energy prices started to rise in the second half of the year. Hosting is already a high volume/low margin business, so every marginal increase in energy prices disproportionally impacted hosting providers. Problems at hosting providers led to inert machines, harming miners’ bitcoin production.

Going forward, we expect the hosting landscape to radically change. First, hosting prices are likely to remain elevated throughout 2023 as hosting providers continue to face infrastructure constraints and energy prices remain volatile. Second, the contractual nature of hosting is likely to dramatically change as customers seek greater transparency on power cost structure and the financial health of hosting providers. Contracts with pass-through power costs plus a spread will likely become the norm, and a clear repartition of curtailment revenues will have to be agreed upon as more players fine-tune their energy strategies. Given what happened with Compute North, it is also likely that the nature of large hosting prepayments change. We may begin to see more traditional offerings to protect deposits, such as escrow accounts, or collateral could be required to reduce credit risk to a hosting provider.

Furthermore, the very nature of the hosting business might change. In 2021, because of heavy demand, hosts were able to demand large upfront deposits, limited terms and miners were beholden to their hosting providers. Depending on the miner’s business model, hosting is either a dedicated business or a secondary revenue stream that can allow a miner to grow in a capex minimized way.

While lower likelihood, it is also not unconceivable to imagine a scenario in which hosting providers become “ASIC holders of last resort” if mining conditions continue to worsen and clients default on their contracts depending upon how they’re structured. Such a situation could allow for hosting providers to increase their ratio of self-mining to hosting quite rapidly.

Over the course of 2022, we have identified over 1,990 MW of announced capacity by companies proposing hosting services, with an additional 1,400 MW of capacity that is being considered for expansion opportunities. As a result, the battle for differentiation between hosting providers will lead to interesting new contract structures and product offerings. For example, more providers might decide to follow the path chosen by Binance, which announced “cloud mining” services in November 2022. While the economics of cloud mining for customers are generally extremely unfavorable, hosting providers might decide to target more retail focused clients who are less price sensitive going forward.

Hashrate Outlook

Given that the next halving will take place in 2024, network hashprice is currently hovering near all-time lows, and tough conditions will likely persist throughout much of 2023, we expect 2023 end of year hashrate to range from 300 EH – 375 EH, with a baseline estimate of 325 EH. The wide range is largely the result of various potential outcomes with respect to bitcoin price and hashprice. Overall, given that miners are operating very close to breakeven and there is uncertainty looming around the next halving, we believe that 2023 will ultimately show smaller growth for hashrate.

Bull Case: Our bull case scenario assumes end of year network hashrate of 375 EH (+41.5% YoY). In order for this target to be met, we would expect that bitcoin price would need to average a level above $30,000 for the duration of 2023 and this would also assume an improvement in the average machine efficiency on the network to a range of 28 j/TH to 31 j/TH.

To hit this target roughly 7.5 EH of hashrate would need to come online per month representing roughly 91,667 ASICs and equating to 210 MW of monthly energization assuming average ASIC efficiency of 28 j/TH.

Base Case: In our base case scenario, we assume an average bitcoin price for 2023 of $25,000 and have network hashrate reaching 325 EH (+22.5% YoY) by the end of 2023. This would imply that miners are able to plug-in 5 EH of machines per month (50,000 ASICs), representing over 165 MW of capacity being energized monthly.

Bear Case: We assume bitcoin price remains depressed in a range between $18,000 - $20,000, with power prices trending higher. Based on these assumptions we arrived at end of year network hashrate of 300 EH (+13.1% YoY). This would imply around 3 EH of machines coming online each month (29,167 ASICs), or 80 MW of capacity being energized monthly.

Additional Discussion & Analysis

Miners and Energy Innovation

Bitcoin mining can lead innovation in the energy sector. Very few other mechanisms can ramp up/down in a short period of time and capture value from various energy sources. Bitcoin mining can help streamline cashflow and improve ROI for different energy projects.

Some interesting examples of miners utilizing excess energy or other unique energy sources from 2022 include:

OceanBit’s ocean thermal energy conversion (OTEC) project

Vespene’s menthane reduction efforts in landfills

Gridless’ support of renewable energy projects in Africa

Tokyo Electric Power Grid’s (TEPCO) collaboration with ASIC manufacturer TRIPLE-1 to direct excess energy to mine bitcoin

We expect the integration of Bitcoin miners and energy projects to continue in 2023 as a larger audience begins to understand how Bitcoin mining can support broader energy goals. As we discussed earlier, miners are putting greater emphasis on refining energy strategies due to the low margin mining environment that is amplified by energy price volatility.

In particular, the partnership between Bitcoin miners and electricity providers will continue to expand. There are tangible benefits for both miners and energy providers to work together to build out operations. Miners can secure lower energy prices and energy providers can have a guaranteed off-taker of energy to monetize excess energy.

Since the energy industry, like Bitcoin mining, requires heavy upfront capital expenditure, the ability to streamline cashflow through mining can help secure much needed external funding. Going forward, whether it be an energy company looking to build out a mining operation itself or to partner with an existing bitcoin mining company, an attractive option could be to procure and mine with cheap older generation machines. These machines would still be profitable if, for example, curtailed energy could be purchased for $10 per MWh, and given the low upfront capital required, payback periods would be improved.

In 2022, we continued to see more of a convergence between Bitcoin miners and energy generators. Growth in Bitcoin mining and growth in energy generation has traditionally been mutually exclusive. As more people begin to recognize the synergies between Bitcoin mining and energy production, we anticipate that growth in these two sectors can move in conjunction with each other, to the point where Bitcoin miners become key players in power markets.

The Convergence of Mining and Lightning

2022 exposed the levels of systemic counterparty risk inherent in depositing bitcoin and other digital assets in certain interest or yield-bearing investment accounts. Despite several of the blow-ups that occurred in 2022, there is still very good reason for miners to seek opportunities to generate yield on their bitcoin holdings. Providing channel capacity and other Lightning-based services could be a consideration for miners because they can earn yield in a counterparty risk minimized way while helping to support and grow the Bitcoin ecosystem. It isn’t unfathomable that miners may one day become the largest Lightning node operators in the network due to the fact that they are generating bitcoin income daily at the lowest cost of procurement.

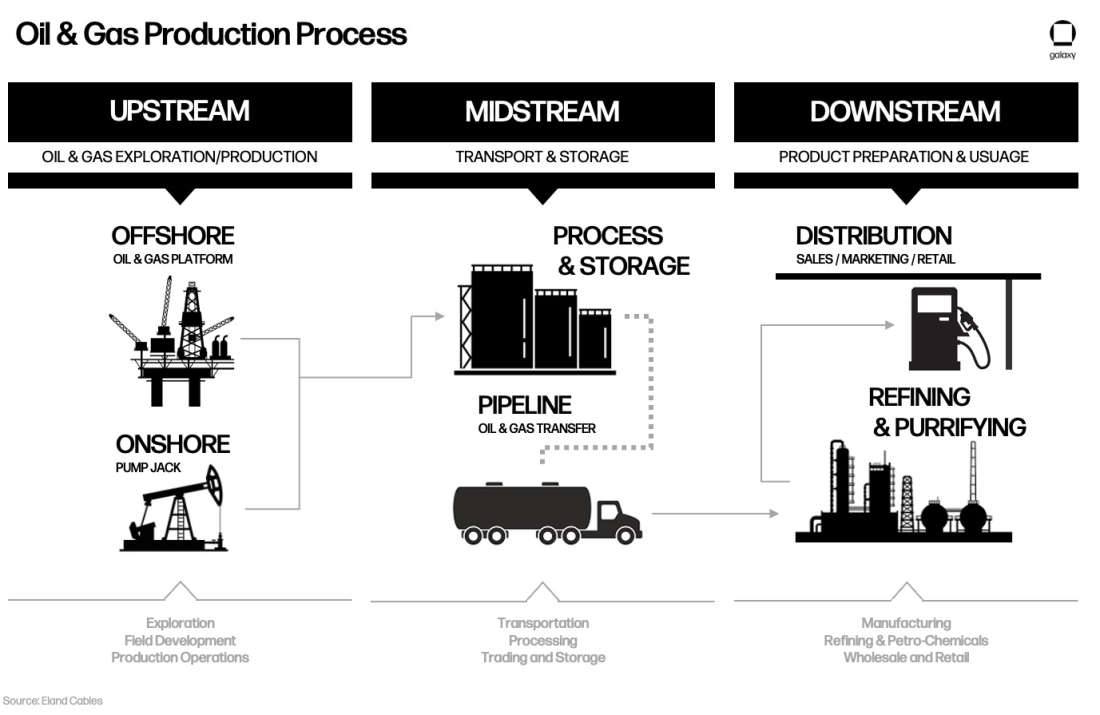

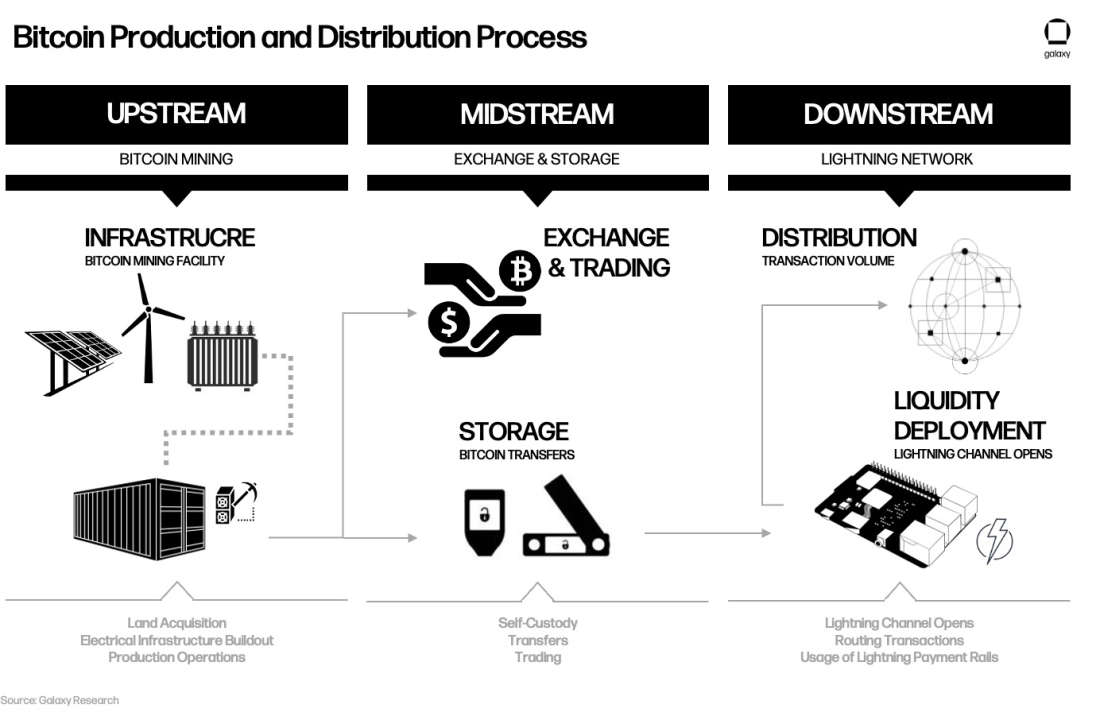

To help demonstrate how the Lightning Network can be a strategic fit for miners, we can analogize the Bitcoin mining industry with the oil & gas industry. The process of mining bitcoin is comparable to the upstream activities in the oil & gas business. Upstream activities in the oil & gas industry encompass the exploration process and involve acquiring land rights, conducting geological surveys, digging exploratory wells to look for reserves of oil and gas. Bitcoin miners go through a similar process by acquiring land, conducting load studies, and building out electrical infrastructure for MW capacity that can be used to power ASICs for generating bitcoins. After oil & gas is extracted, it is transported to refineries to be turned into products for end consumers. In this same fashion, the Lightning Network can be thought of as a refinery for bitcoin to provide additional utility to end consumers through various applications and services. To put it another way, users of Lightning Network services and applications can serve as the downstream consumers of Bitcoin miners’ upstream production.

Opportunities for Bitcoin Miners

Routing Fee Yield: In the same way that Bitcoin miners earn fees for processing transactions in the Bitcoin network, Lightning node runners earn routing fees for relaying transactions in the network to their end destination. River Financial, a bitcoin brokerage that runs the 4th largest Lightning node, reported that they are earning about a 1.15% APY on 420 bitcoin of total capacity. As activity on the Lightning Network grows, there is potential for these APYs to increase.

Channel Leasing & Liquidity Provision: Bitcoin miners could also earnyield by providing inbound channel capacity to other nodes in the network. Marketplaces, such as Amboss and Pool by Lightning Labs, allow for node operators to set terms for channel leases where users have been earning APYs ranging from 3% to 25% depending on the ranking of the node, the duration of the lease, and size of the lease. Relative to Defi lending, channel leases are far less risky because the lender is always in control of the funds and can terminate the agreement at any time by simply closing the channel. In addition, channel lease fees are paid upfront to the lender and while the channel is open, the lender can also earn routing fees, which can provide additional yield on top of lease fees.

Future Growth for Lightning: Taproot Asset Representation Overlay (Taro), a new protocol being designed by Lightning Labs, has the potential to create new utility and use cases for Lightning. The protocol will allow users to issue fungible assets, including stablecoins, and non-fungible tokens (NFT) like digital collectibles on Bitcoin. If Taro is successful and translates to additional activity on the Lightning Network, APYs for routing fees could see a meaningful increase. Use cases for Taro-based assets can be further strengthened with discreet log contracts (DLCs) and covenants if adopted the bitcoin community.

Lightning Mining Pool Payouts:

Impact for retail miners: If mining pools enable payouts over Lightning, it becomes more practical to produce affordable full-stack bitcoin infrastructure products for home or retail miners. We can imagine having a 1 – 5 TH plug-n-play ASIC that is about the size of a router that also includes Bitcoin and Lightning nodes. With payouts over Lightning, pool payout thresholds could be reduced such that it makes it feasible to run an ASIC that may only generate less than 5,000 Satoshis (sats) per day. These sats earned from mining could be paid directly to the Lightning node on the device, allowing for a daily income stream that could then be used for all sorts of other Lightning services such as social media, games, streaming sats, or shopping. This type of product could help to further decentralize the Bitcoin network and help to create a Bitcoin circular economy.

More frequent payments: If pools enabled payouts over Lightning, miners could get paid as reward shares arrive, enabling for payouts several times per minute. Additionally, smaller and more frequent payments can reduce counterparty risk miners take on with pool operators.

Potential to get paid in stablecoins with Taro: With the combination of Taro and mining pool payouts, miners could theoretically receive payment directly in a USD stablecoin over Lightning rails, with a payment frequency of several times per minute. Mining pools could accomplish this by serving as a broker or market maker in the stablecoin over Lightning. If retail electric providers (REPs) accepted this stablecoin over Lightning rails, then miners could have the ability to receive pool payouts and pay their REP in real-time as the meter spins for energy consumption. This could reduce margin requirements for miners, allow miners to save on exchange fees because miners’ costs are in USD, reduce counterparty risk for REPs, and allow REPs to accept payment over bitcoin rails without them having to take on bitcoin price volatility.

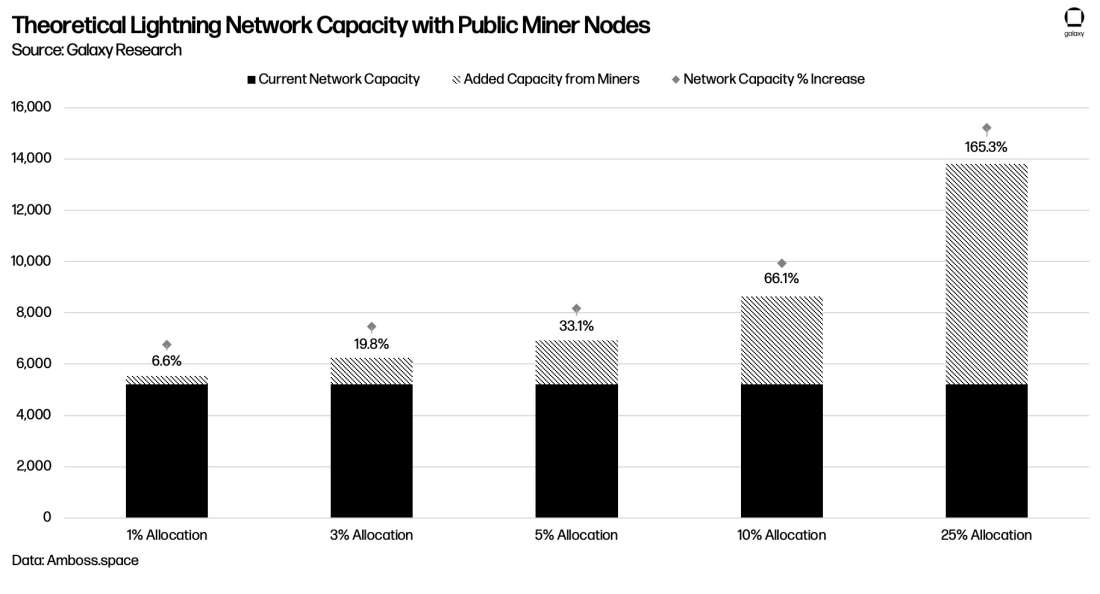

Public bitcoin miners could operate some of the largest nodes on the network: The chart below illustrates how much capacity could be added to the Lightning Network based on various increments of percentages of allocation from publicly traded Bitcoin miners’ total bitcoin holdings.

While the network is still in its infancy, Lightning continues to evolve under the radar, with 2022 representing a great year for growth even when the broader crypto industry struggled. Public capacity grew by 55.2% from 3,312 bitcoins to 5,142 bitcoins ($92.55mm), and the network now accounts for over 16,000 public nodes managing over 75,000 channels.

Learnings from the Gold Market

Although we flagged overleverage and ambitious growth targets throughout this report, it is important to highlight that this is not a unique phenomenon to Bitcoin mining. Several other industries have gone through the same experience. Put simply, this is part of the business cycle. During growth periods, businesses take on debt to build out operations as quickly as possible. Overexuberance causes many companies to issue more debt than they can handle, which catches them off guard when there is a downturn. Especially in a low interest rate regime, businesses have the opportunity to secure cheaper financing, which encourages them to take on even more debt.

Gold mining, for example, is one such industry. Ignoring the asset level debate between Bitcoin and gold, the industries have gone through similar business cycles. Gold experienced a dramatic price appreciation from 2000-2012, followed by a downturn. Analysts at McKinsey have written an excellent report on these trends. Using insights from McKinsey, we explore below the similarities between the boom/bust cycle in the gold mining market with bitcoin’s cycle, as well as identify lessons from the gold mining cycle that could play out in some fashion in Bitcoin mining.

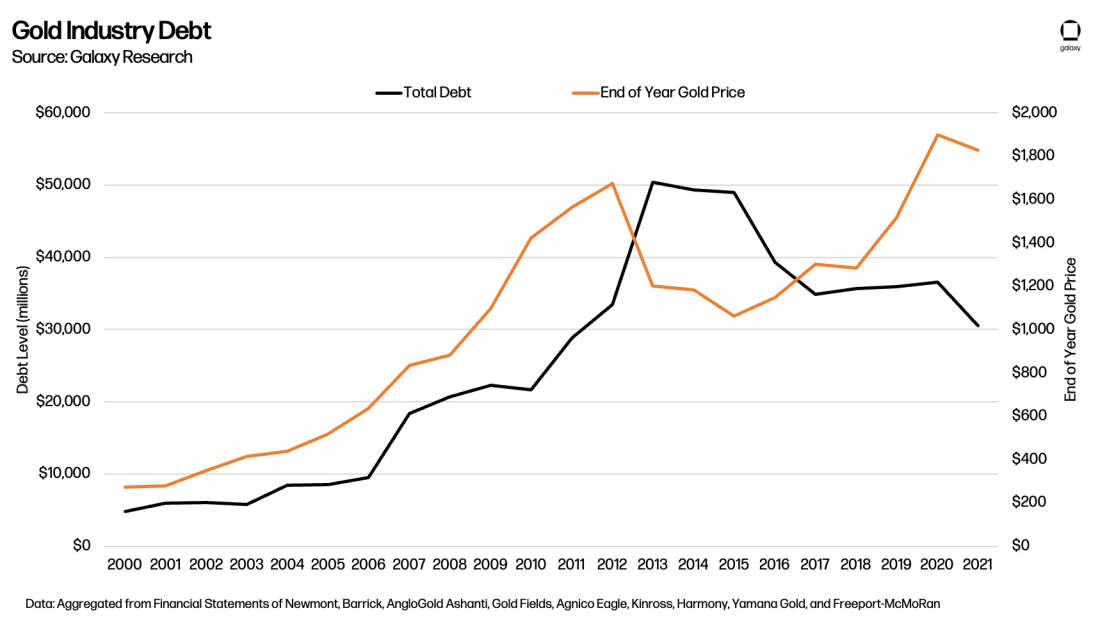

The run up in gold prices between 2000-2012 led to an influx of capital into the industry. Industry level debt grew from $5bn in 2000 to $50bn in 2013 to fund expansion strategies. In 2011, gold prices peaked at $1,900 and the several years that followed saw industry participants reducing leverage on their balance sheets to more manageable levels. Examples of deleveraging include Barrick selling off non-core assets to strengthen their balance sheet and Newmont divesting several mines.

The Bitcoin mining industry is currently in the deleveraging phase of the business cycle. Public miners, including Stronghold Digital, Iris Energy, and Greenidge have all relinquished ASICs in efforts to reduce monthly debt payments and strengthen their balance sheets. Monthly debt service obligations and seismic capital expenditures have depleted cash balances and pushed miners into or near bankruptcy. These are the early innings in an industrywide effort to improve long-term business sustainability.

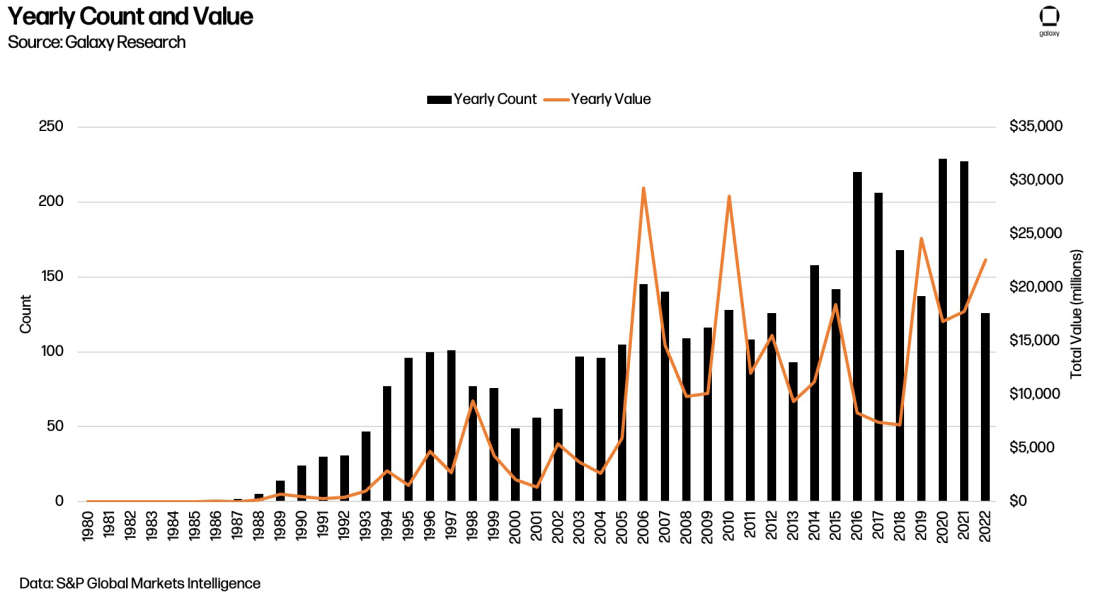

Alongside the growth in debt during the gold boom was an increase in the number and size of M&A transactions. Total industry deal size peaked in 2006 at $29bn and almost touched that level again 2010. Gold miners did all they could to expand operations without much regard to bringing shareholder value. They overpaid on transactions, only to be left with billions of dollars of impairments and losses in the following years. After 2012, M&A activity decreased substantially as gold miners pivoted to reducing debt and improving operating efficiency. There still was some M&A activity between 2013-2016, but as shown in the chart, deal sizes were much smaller. We are now once again seeing a resurgence in M&A activity as gold prices recover, improving cash flow that can be reinvested in the business.

This is an important trend to observe that has cross industry application. In 2021, Bitcoin miners pursued similar uneconomical growth strategies, without keen attention on ROI and value creation. In 2022, widespread dialogue in Bitcoin mining has centered around industry consolidation. While there has been some M&A activity between miners, such as CleanSpark’s acquisition of Mawson’s Georgia site, Galaxy’s purchase of Helios, and Crusoe's acquisition of GAM, M&A isn’t a primary focus for most miners right now due to capital constraints. The industry is under a lot of stress and miners don’t have sufficient cash at their disposal, which makes it difficult to justify large scale cash burn through acquisitions. An uptick in M&A activity could occur if some distressed mining funds begin tapping into the market or other external sources of capital make their way into the industry, but it will be difficult for miners themselves to drive acquisition efforts because of the current emphasis on preserving capital. As mining economics improve longer term, similar to what the gold industry is now experiencing, we could see Bitcoin miners lead M&A activity as they rebuild cash balances organically, but that is not a process that happens overnight.

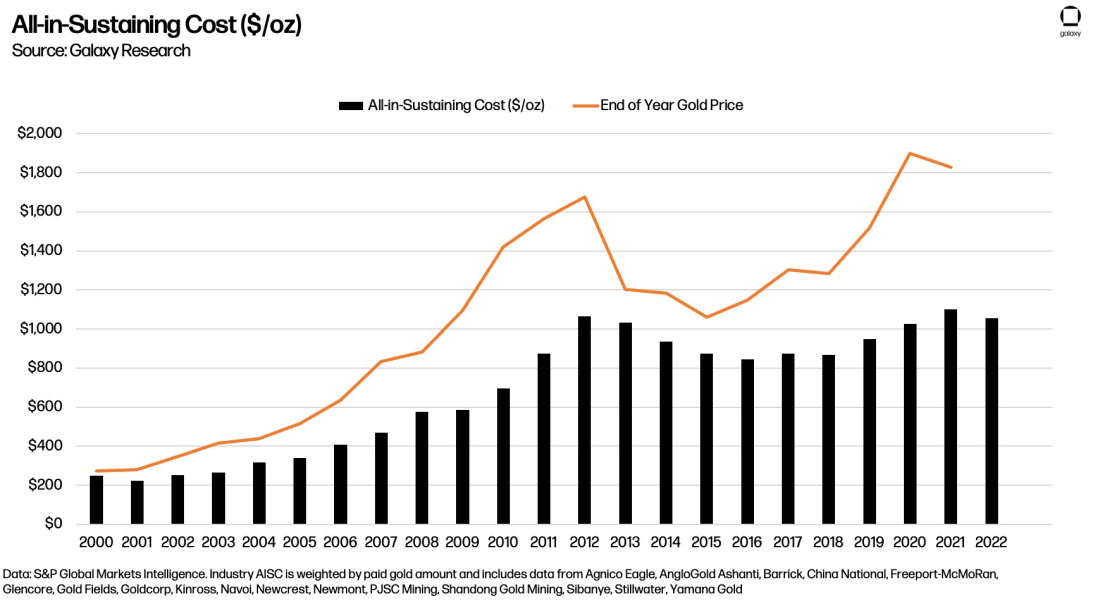

Once gold prices began to fall, gold miners tried reducing their costs. The chart below shows a metric commonly observed in gold mining, which is similar to the all-in cost to mine a bitcoin metric utilized in Bitcoin mining. This metric is called the All-In Sustaining Cost (AISC), which is the overall cost to mine an ounce of gold. It includes all operating expenses plus capital needed to sustain production levels over time. The chart below shows how closely AISC trended with gold prices, where miners really started to focus their attention on improving costs after 2012. These cost reduction plans were also assisted by declines in oil prices, which helped drive down All-In Sustaining Costs for gold miners.

Some of the cost cutting measures McKinsey notes include AngloGold’s 11% reduction through operational improvements and Newmont’s 24% reduction because of portfolio optimization. Gold miners also reduced capital expenditure including Kinross’ 50% capex reduction in 2013 and Goldcorp’s 40% and 60% reductions in 2014 and 2015, respectively. We’ve already seen some similar measures announced by Bitcoin miners including Core Scientific, Terawulf, and Greenidge, both on the operating expense and capital expenditure sides to preserve cash. Going forward, other ways Bitcoin miners can cut costs would be through machine efficiency swaps, which could provide incremental demand for newer generation machines. The combination of deleveraging and cost optimization in a difficult economic environment will create more nimble and leaner companies that are able to withstand longer term volatility.

Conclusion

The Bitcoin mining industry is going through a similar storyline that we have seen before. The nascency of the Bitcoin mining industry can make it an easy target of scrutiny amongst pundits for the miscalculated steps taken over the course of the past couple years, but it is hardly the first industry to experience boom and bust cycles. Bitcoin miners in 2021, like gold miners in the 2000s, took on more than they could handle. Only in the past couple of years, as gold prices rose, have gold miners begun to refocus their attention on growth and bringing accretive value to shareholders. It will take time for Bitcoin miners to deleverage and improve efficiency of operations, as it did for gold miners.

The survival strategies utilized by miners in 2022 were diverse and heterogenous depending on the liquidity situation of the company and included everything from liquidating their treasuries to selling ASICs, ASIC coupons, mining facilities, and equity, as well as restructuring debt. Despite these measures, there were still several bankruptcies and ASIC-backed loan defaults that affected some of the biggest miners and hosting providers in the space. The Bitcoin mining industry is currently going through a purge of all of the excess and misallocations of capital that supported weak business models during the bull market of 2021. Rough economic conditions forced miners to make tough choices in order to meet obligations related to ASIC purchases, infrastructure, and debt obligations. Miners ended 2022 in survival mode, setting the stage for more turbulent times ahead in 2023.

Glossary

Marginal Cost of Production - The marginal cost of production is representative of a miner’s cost of electricity and hosting to produce 1 bitcoin. It does not, however, capture the capital expenditure for the mining equipment itself. To calculate the marginal cost of production for a publicly traded bitcoin miner, simply divide the cost of revenues excluding depreciation expense by the number of bitcoins mined during that period.

Direct Cost of Production - The direct cost of production takes the marginal cost of production a step further by including depreciation expenses in the calculation. This gives a sense of how much a miner is spending on ASICs. When derived from filings, this figure may also include depreciation of hosting facilities for their machines, depending on the level of detail included in the filing. To calculate the direct cost of producing a bitcoin for a publicly traded bitcoin miner, simply add the cost of revenues and the depreciation expenses from the income statement and then divide by the number of bitcoins mined during that period.

Total Cost of Production - The total cost of production accounts for the overhead of running the business, including payroll of employees, by including SG&A in the equation. It is important to exclude any non-cash or one-time expenses from this equation, such as impairments to cryptocurrencies or any marketable or related securities, and employee-based stock compensation. While stock-based compensation is excluded from this calculation, it is important to note the level of stock-based compensation as it is dilutive to shareholders. To calculate the total direct and indirect cost of producing a bitcoin for a publicly traded bitcoin miner, simply add the cost of revenues, depreciation expenses, and selling, general and administrative expenses from the income statement, then divide by the number of bitcoins mined during that period.

Network Hashprice - Network hashprice, often simply referred to as hashprice, is a measure of dollar-denominated daily expected revenue from mining with a single terahash per second of hashrate on a daily basis given current conditions around bitcoin price, block rewards and network hashrate.

Sats per TH - Is a measure of bitcoin-denominated daily expected revenue from mining with a single terahash per second of hashrate on a daily basis given current conditions around block rewards and network hashrate. 1 satoshi represents one one-hundred millionth of a bitcoin.

Operational Breakeven Cost - Operational breakeven cost attempts to quantify all recurring expenditures that require a true cash outlay and includes cost of revenues, selling, general, and administrative (SG&A) expenses, and interest expenses, while excluding all non-cash expenses such as employee stock-based compensation and depreciation and amortization.

Network Hashrate - The network hashrate is the cumulative processing power of mining machines securing the network.

Block Subsidy - The block subsidy is the amount of new bitcoin minted in each block. The block subsidy halves every 210,000 blocks (roughly every 4 years) according to Bitcoin’s issuance schedule and is currently 6.25 BTC.

Transaction Fees - Blocks can contain many transactions with fees attached to incentivize their confirmation and prevent spam. In addition to the block subsidy, miners also receive the transaction fees for all of the transactions included in the block that they mine.

Block Reward -The block reward is the combination of the block subsidy and all transaction fees paid by transactions in a specific block.

Hashrate - Hashrate is a measure of the computational power per second used when mining.

Power Draw -Power draw is a measure of the amount of electricity consumed to operate an ASIC or mining machine per hour.

Mining Pool -A mining pool is a middleman that aggregates multiple miners’ hashpower. Mining pools aggregate pool members’ hashes, submit successful proofs of work to the network, and distribute rewards to contributing miners proportionately to the amount of work performed. Mining on a pool reduces payout variance for miners, who would otherwise have to deal with significant risk from finding blocks at unpredictable intervals.

Terahash - A terahash (TH) is one trillion hashes, which is equivalent to making one trillion guesses at solving the puzzle to add the next block to bitcoin’s blockchain. The hashrate of most mining rigs is measured in terahashes per second (TH/s).

Exahash - A exahash (EH) is one quintillion hashes, which is equivalent to making one quintillion guesses at solving the puzzle to add the next block to bitcoin’s blockchain. The total network hashrate is typically measured in exahashes per second (EH/s), as is that of some large mining operations.

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2022. All rights reserved.